The Iran war has scrambled the old map of safety, leaving bond investors rethinking which havens still deserve the name. It’s debatable whether the period since the attacks began on Feb. 28 has forged a new normal, but a review of performance across major fixed‑income sectors certainly raises questions about how to manage expectations.

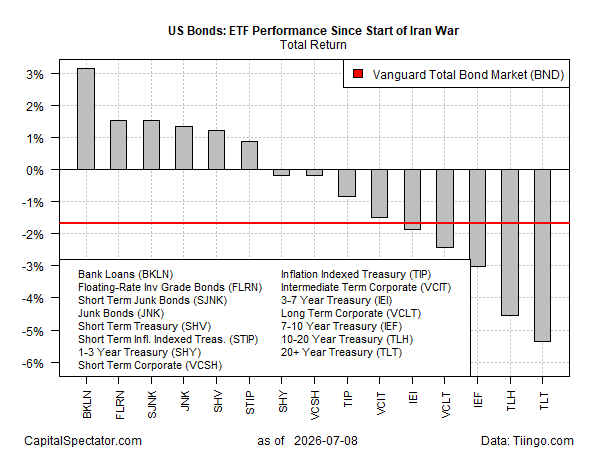

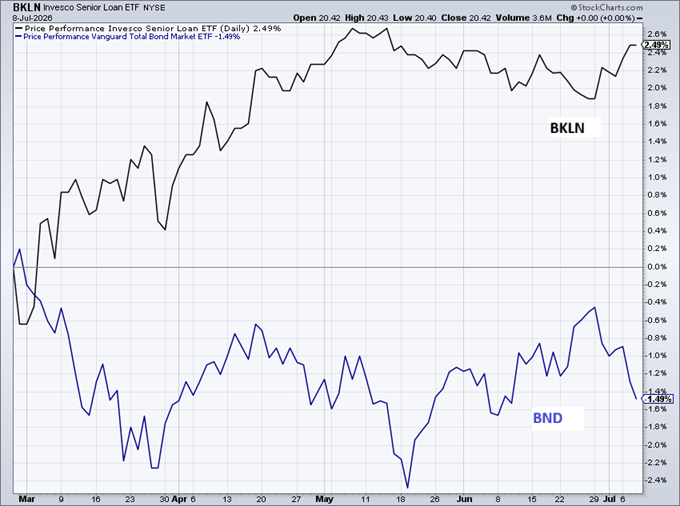

Perhaps the most surprising trend since the conflict began: bank loans have outperformed the rest of the field by a wide margin, based on a set of ETFs through yesterday’s close (July 8). The Invesco Senior Loan ETF (BKLN) continues to lead, rallying more than 3% since Feb. 28 — roughly double the gain of the next‑best performers.

Meanwhile, most Treasuries and the investment‑grade benchmark — Vanguard Total Bond Market (BND) — remain underwater since the war began. The biggest loss: long Treasuries (TLT), down more than 5%.

One explanation is that the war has lifted inflation and fueled expectations that the Federal Reserve will soon be forced to react by raising interest rates. Add in growing concerns about the still‑unaddressed rise in federal debt, and incentives are in place to think differently about safe havens.

Bank‑loan securities surged because the war in Iran flipped the usual risk playbook. Investors rushed to floating‑rate, senior‑secured credit, which suddenly looked safer than the long‑duration assets that typically anchor defensive portfolios.

BKLN holds floating‑rate, senior‑secured junk loans. The ETF’s strength in recent months suggests investors are eager to chase higher yields while sidestepping interest‑rate risk. They’re willing to take on a bit more credit risk to lock in coupon income and seek protection from future rate hikes.

On that basis, it’s no surprise that the second‑best performance during the war is essentially a tie between a dedicated floating‑rate note ETF (FLRN) and a short‑maturity junk‑bond fund (SJNK).

This isn’t a free lunch, however. Investors should be aware of three pressure points for BKLN and other funds favoring floating‑rate loans issued by relatively highly leveraged borrowers: shrinking income if the Fed cuts rates, leveraged borrowers vulnerable to tightening credit, and an underlying loan market prone to sudden liquidity freezes.

The crowd’s preferences remain clear, and BKLN’s strength is conspicuous relative to the investment‑grade benchmark (BND) since the war started.

To the extent that the Middle East conflict has persuaded investors to favor BKLN and similar portfolios, this week’s news flow suggests geopolitical risk will remain elevated. Renewed military strikes in the Middle East have jolted markets by reviving fears that the region’s fragile calm is slipping back into open conflict.

If war and geopolitical uncertainty have been bullish factors for BKLN and its counterparts in recent months, the near‑term outlook still looks supportive for this slice of the fixed-income market.

Comments

Log in or sign up to join the conversation.