The Iran war, now in its 103rd day, has reignited with bombs and missiles flying in all directions. Trump is threatening massive retaliation up to and including Iranian power plants and bridges.

Iran has said it will respond in kind to any bombings up to and including striking the remaining functional GCC energy infrastructure targets and the Bab al-Mandab strait (the entrance/exit to the Red Sea).

Wednesday night (6/10/26) saw Iran strike US airbases in several countries, and reports of massive explosions in Iran.

Despite all that, oil fell on the news … again. This morning (6/11) WTI oil in the US had fallen all night long, losing $4/bbl by morning.

Whether this is market complacency or evidence of active market rigging by US authorities, the result will be the same. Eventually, US oil stockpiles will reach some sort of terminal bottom. Then it will be game over.

Oil prices will spike, slamming the US economy into a brick wall with the least amount of time to prepare or adjust.

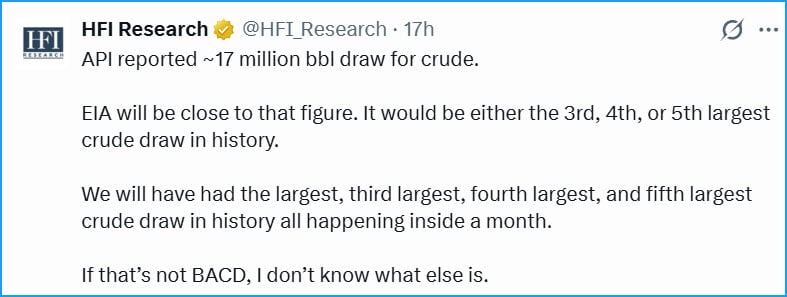

Believe it or not, the US has experienced 4 out of the 5 largest crude draws in history during a month when oil prices actually retreated significantly. FYI, “BACD” stands for Big A** Crude Draw.

The economic damage that is on the way is incalculable.

Gold Capitulation?

Equally mysterious would be the price behavior of gold, having steadily fallen ever since the start of the Iran war.

Shouldn’t gold be a crisis hedge? Or at least an inflation hedge (which is currently spiking rapidly)? Yes, but then again, we live in bizzarro world now.

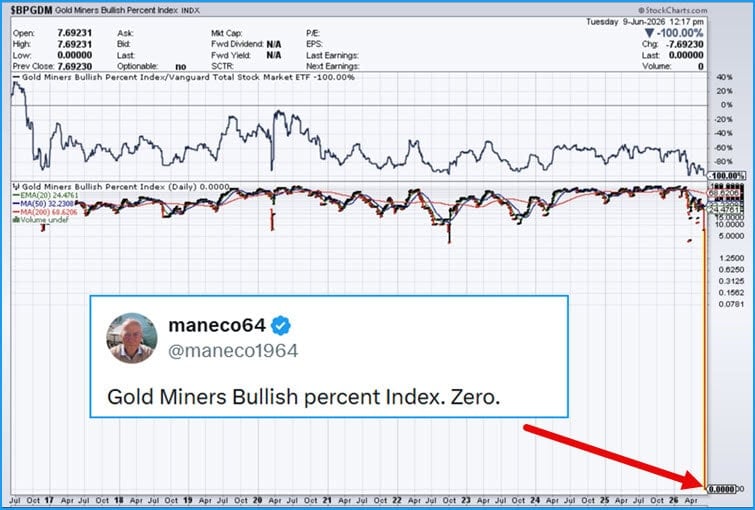

To really put a fine point on it, the gold mining stocks just recorded a “Bullish Percent” reading of…zero:

That means no stocks went up. None. Complete capitulation within the space. Nobody wants these money-printing machines.

Larry Lepard gives us the proper grounding on this historic event:

Inflation!

Inflation has reared its head, as Paul and I have long been discussing, in the form of higher PPI and CPI readings. The most recent reading for the CCI was 4.2%.

Once again, wages are now trailing inflation – a condition that is certain to worsen over the coming months (and years?).

It’s a global phenomenon with Japan’s PPI reading recently having come in at a scorching 6.3% (yr/yr).

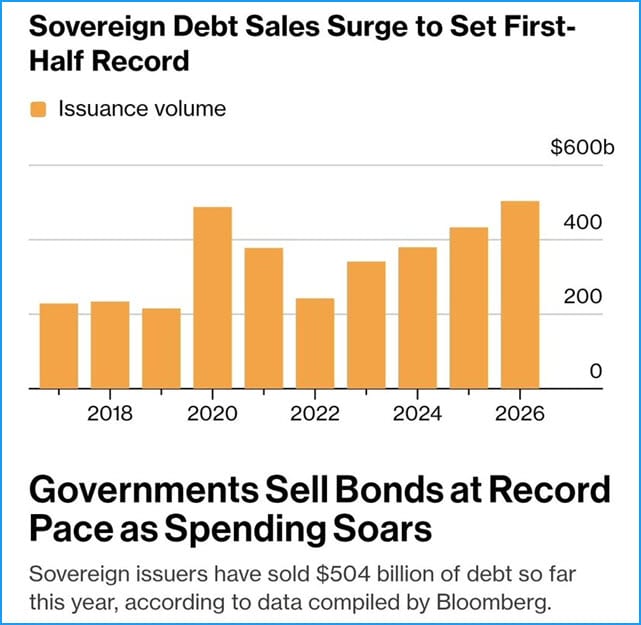

A huge driver of inflation, of course, is government deficit spending, which is also something of a global phenomenon. Currently sovereign bond sales are exceeding even the COVID scramble.

You all know what happened to inflation after that, right?

The AI Super Bubble

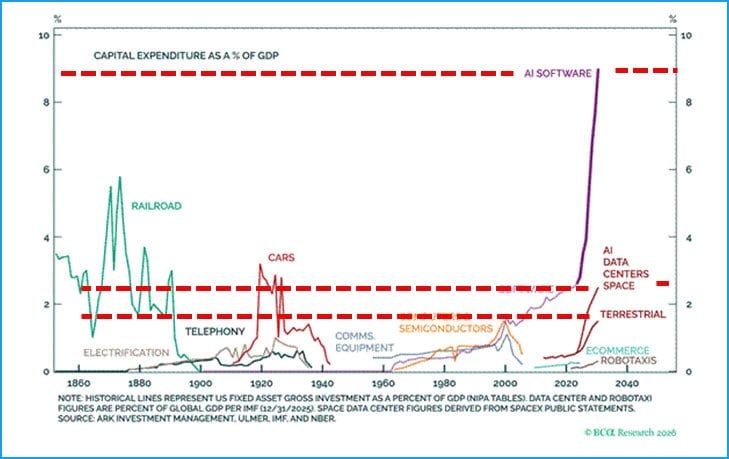

Keeping everything afloat in the US, presently, is AI CAPEX spending and circular financing.

When put on an apples-to-apples footing, the current AI CAPEX boom is without equal across every prior bubble since 1850:

Every single prior CAPEX boom was followed by huge losses. This time will not be different.

Given the extreme concentration of equity valuation in just ten major AI-related stocks, the risk to the overall stock market is enormous.

Either this AI play works out or it doesn’t. As of today, the revenues simply aren’t there to support the valuation extremes.

They might show up, but I doubt they will. Tick tock. However, oil continues to fall, as does gold, while US equities mysteriously climb.

It would seem that nothing matters, and anything goes.

Which is always a warning sign and why Paul continues to caution that people should be steering away from passive investing strategies and toward active tactical risk-managed strategies.

Comments

Log in or sign up to join the conversation.