Markets were mulling familiar themes last week. Will a wider U.S. twin deficit change the rules for the dollar and treasuries and is elevated volatility here to stay in equities? Judging by last week, the answer would be: probably and yes. The contemplation over these stories, though, were interrupted by politics. Mr. Trump announced his intention to apply tariffs on steel and aluminium—25% and 10% respectively—and Mrs. May attempted to give clarity on the U.K. government’s Brexit position.* I was unimpressed with both.

Before I have a dig at Mr. Trump, I ought to provide an example of some-one who supports it. I have great respect for Stephen Jen, but his argument here is like endorsing the idea of a diet by advising someone to eat nothing but kale and carrots for a decade.

The analysis of Mr. Trump’s tariffs requires a distinction between the principle and the concrete measures. I concede that China is bending the rules of global trade, but Mr. Trump is stretching the fabrics of macro-economic policy if he starts imposing tariffs on industrial goods. He is presiding over an economy close to full employment, a low domestic savings rate, and a medium-sized twin deficit. To boot, he is about to let fly with unprecedented fiscal stimulus.

Adding policies to close the economy from the outside world—which presumably is the idea—is a recipe for soaring inflation and a sharp increase in interest rates. The dollar is a wildcard, though. Immediately after the election, markets also were considering the impact of tariffs. But they did so in the context of the assumption of a dollar bull market. The idea was that if the White House imposed tariffs of 10%, the dollar would rally 10% to cancel out the impact. Now, however, markets have been spooked by the prospect of fiscal stimulus, sending the dollar lower and bond yields higher.

Assuming that that U.S. savings rate remain unchanged, a steel and aluminium tariff is the equivalent of shooting yourself in the foot. By far the biggest steel sector in the U.S. is downstream— firms that use steel as inputs—and they now have to pay more for their raw material imports. With fiscal stimulus in infrastructure and defence coming their way, it seems unlikely that they will be able to switch entirely into domestically sourced steel. In other words, a tariff can be analysed like a tax increase, and microeconomics show that those with low demand elasticity tend to pay the lion’s share of it. Given where the U.S. economy is in the business cycle, the risk is high that the burden will be carried mainly in the domestic market. If the dollar weakens, and U.S. steel and aluminium imports rise, due to the boost from fiscal stimulus, the external deficit will widen.

The concrete measures also look misplaced. The tariffs will be applied universally on all countries’ imports and have been implemented under the guise of national security. The direct hit to Chinese producers will be limited, but the effect the closest U.S. trading partners and allies will be anything but.

Either Mr. Trump and his advisers don’t understand balance of pay-ments or they are trying to show the world that they are willing and able to break shit. I suspect it is a bit of both. With Mr. Navarro back in the hot seat, we are dealing with an adviser who bafflingly believes that anyone who runs a surplus with the U.S. is cheating.

WILL EQUITIES CARE ABOUT IT?

Equities were initially hit on Friday by Mr. Trump’s comment that “trade wars are good and easy to win,” but settled at the close to finish a volatile week down about 2% across the board. A few metals tariff won’t change anything. But further escalation and the threat of trade wars won’t do markets any good. The EU has daftly hit back with the threat to tax Harleys, Bourbon and Levi’s jeans, prompting an immediate reply from Mr. Trump to sting EU cars with taxes. Expect a lot of talk about who puts tariffs on who—and at what rate—this week. In the end, that doesn’t matter for investors. The key thing at stake here is the central pillar of equity bulls’ thesis for further upside: the synchronised upturn in global growth.

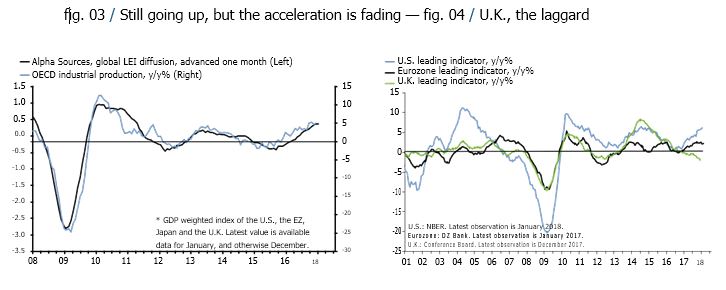

For now, it looks like smooth sailing. My first chart below shows that mar-kets continue to enjoy tailwinds from improving macroeconomic data. OECD industrial production growth is rising, and global leading indicators are on the up. But the second derivative of my LEI diffusion index is rolling over, as is momentum in real money growth in the largest global economies.

We don’t yet have evidence of any-thing sinister, but my spider sense tells me that an inflection point looms at the end of Q2. The simple pushback to this view is that U.S. fiscal stimulus comes online, prompting an acceleration of U.S. and global growth. That’s fine, but if the economy has to chase this down with a trade war, the consequences would be grim. In the U.S., inflation and interest rates would jump, and in the rest of the world, growth would slow.

The second chart below allows me to make a transition to Brexit. Prime Minister Theresa May delivered yet another speech on Friday, which as far as I can see provided little clarity on the U.K.’s position. Mrs. May did, however, acknowledge that Brexit has costs—for both the EU and the U.K.—and that things will not be as they were. That was a welcome dose of realism.

Ironically, the short-term evolution of this tragedy will probably be to make sure things remain the same via an extended transition period.

I have no clue where it all ends, but I am pretty sure that the U.K. economy is slowing. Leading indicators are send-ing a uniformly negative message, suggesting that the gentle decline in headline U.K. GDP growth will continue in the next few quarters. If this is true, it ought to provide tailwinds for remain-ers and soft brexiteers, Unless the U.K. economy crashes and burn, though, I doubt that it will turn the tide on public opinion. And I doubt that U.K. is staring down the barrel of a recession, at least not in the next 12 months.

TO SWIM NAKED IN BOND MARKETS?

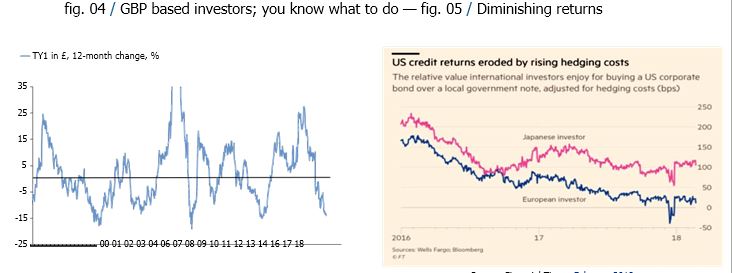

Speaking with traders over the years, my understanding has always been that hedges are something you buy in B&Q and in Home Depot. Apparently, this is not the case for global fixed income managers. Interest rate differentials be-tween the U.S. and the rest of the world are juicy as ever, but take into account hedging cost and the advantage all but disappears. There is a paradox of safety at work here. The faster the dollar declines against the euro and the yen, the safer it becomes to take currency risks. For investors who can’t, or won’t, take naked FX risk, however, the costs of hedging rises, eroding the net return of buying the rate differential between the U.S. and the rest of the world.

I accept the fact big fixed income managers—especially in sovereign bonds—can’t take currency risks, even if they wanted to. That’s great news for small-time punters, who can. I have been showing various models in my recent posts, indicating that U.S. treasuries—and 2y notes—are becoming attractive. Valuation scores are turning up, and bearish speculators are exposed due to a significant net-short position. The weaker dollar is a just an added benefit. To be clear, U.K. based inves-tors’ purchasing is not historically high with GBPUSD at about 1.40. But Cable has rallied in the past six months. The first chart below shows that the trailing year-over-year return of U.S. 10-year future in GBP. It’s rarely been lower. The decision should be easy; sell some of those expensive shares, buy some bonds, revisit in 12 months.

Comments

Log in or sign up to join the conversation.