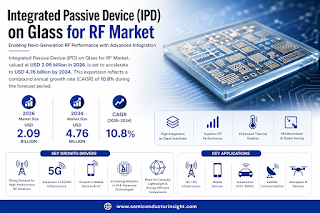

Integrated Passive Device (IPD) on Glass for RF Market, valued at USD 2.09 billion in 2026, is set to accelerate to USD 4.76 billion by 2034. This expansion reflects a compound annual growth rate (CAGR) of 9.6% and is detailed in a newly released research report from Semiconductor Insight. The study underscores the pivotal role of glass‑based IPD solutions in meeting the ever‑tighter performance, size and power‑efficiency constraints of next‑generation radio‑frequency (RF) systems across telecommunications, automotive, Internet of Things (IoT) and aerospace sectors.

IPD on glass combines the superior dielectric characteristics of high‑purity glass substrates with advanced thin‑film passive component integration, delivering ultra‑low signal loss, enhanced dimensional stability and a dramatically reduced footprint compared with traditional silicon or organic packages. These attributes make glass‑based IPDs a strategic enabler for high‑frequency 5G mmWave front‑ends, multi‑band smartphones, V2X automotive modules and compact IoT radios, where every millimeter of board space and every decibel of insertion loss matters.

Download FREE Sample Report:

Integrated Passive Device (IPD) on Glass for RF Market - View in Detailed Research Report

5G & mmWave Proliferation: The Primary Growth Engine

The relentless rollout of 5G networks, especially the migration to sub‑6 GHz and mmWave bands, is reshaping RF architecture. Operators are demanding passive components that sustain high‑frequency performance while occupying minimal board area. Glass‑substrate IPDs meet these demands by offering a dielectric loss tangent that is substantially lower than that of conventional polymer or silicon platforms, directly translating into higher link budgets and longer range for base‑station and handset designs.

Simultaneously, the mobile handset market is moving toward multi‑band, multi‑mode radios capable of supporting 5G, LTE, Wi‑Fi, Bluetooth and NFC within a single front‑end module. The integration of filters, diplexers, couplers and baluns on a single glass wafer eliminates the need for discrete component placement, reduces interconnect parasitics and shortens the overall RF signal path. This integration advantage is a decisive factor for OEMs seeking to keep device thickness below 7 mm while still delivering best‑in‑class connectivity.

Automotive Connectivity and Advanced Driver‑Assistance Systems (ADAS)

Modern vehicles are evolving into connected platforms that rely on high‑frequency radar, V2X (vehicle‑to‑everything) communication and over‑the‑air software updates. These functions demand RF front‑ends that can operate reliably across a wide temperature envelope and withstand harsh vibrations. Glass‑based IPDs provide excellent thermal stability and mechanical robustness, ensuring consistent filter characteristics from –40 °C to 125 °C-critical for automotive safety‑critical applications.

Major automotive OEMs and Tier‑1 suppliers are therefore accelerating their adoption of glass‑substrate passive components to consolidate RF front‑ends, reduce bill‑of‑materials costs and simplify supply‑chain logistics. The growing prevalence of autonomous driving prototypes further amplifies the need for compact, high‑performance RF solutions, positioning IPD on glass as a cornerstone technology for the next generation of smart vehicles.

IoT Expansion and Edge Computing

IoT devices-from wearable health monitors to industrial sensors-are proliferating at an unprecedented pace. Many of these devices operate in crowded ISM bands and require precise filtering to avoid interference while maintaining ultra‑low power consumption. Glass‑based IPDs, with their minimal insertion loss and high Q‑factor, enable designers to meet stringent energy budgets and extend battery life.

Edge‑computing gateways, which aggregate data from thousands of sensors, are also integrating higher‑frequency radios for private 5G and Wi‑Gig deployments. The modular nature of IPD on glass allows for rapid customization of passive networks, shortening time‑to‑market for new IoT use cases and supporting the scalability demanded by massive device deployments.

Supply‑Chain Consolidation and Technological Innovation

The IPD on glass market is seeing a consolidation of supply chains as leading semiconductor manufacturers acquire or partner with specialized glass‑substrate foundries. This trend accelerates technology transfer, reduces lead times and fosters co‑development of next‑generation packaging processes such as through‑glass vias (TGV) and wafer‑level packaging (WLP). The resulting economies of scale are essential for meeting the projected demand from high‑volume consumer electronics and telecom equipment manufacturers.

Furthermore, research initiatives in Europe, Japan and the United States are exploring novel glass compositions that push dielectric loss even lower, while advanced thin‑film deposition techniques improve component tolerance and reliability. Such innovation is expected to unlock new RF topologies that were previously impractical on traditional substrates.

Regional Dynamics

Asia‑Pacific remains the dominant engine for market growth, leveraging a dense ecosystem of foundries, material suppliers and contract manufacturers. Government‑backed semiconductor initiatives in China, South Korea and Taiwan are channeling billions of dollars into advanced packaging, further cementing the region’s leadership through 2034.

North America, particularly the United States, continues to lead in RF‑chip design, defense electronics and private‑5G deployments, creating a highly attractive niche for high‑performance glass‑based IPDs. Europe’s strong automotive sector and EU‑funded semiconductor programs are fostering a steady increase in regional demand, while the Middle East and Africa present emerging opportunities tied to 5G‑enabled smart‑city projects and expanding mobile broadband penetration.

Get Full Report Here:

Integrated Passive Device (IPD) on Glass for RF Market, Trends, Business Strategies 2026-2034 - View in Detailed Research Report

COMPETITIVE LANDSCAPE

List of Key Integrated Passive Device (IPD) on Glass for RF Companies Profiled

Murata Manufacturing Co., Ltd.

TDK Corporation

STMicroelectronics

Qualcomm Technologies, Inc.

Broadcom Inc.

Skyworks Solutions, Inc.

Qorvo, Inc.

Taiyo Yuden Co., Ltd.

Vishay Intertechnology, Inc.

Würth Elektronik GmbH & Co. KG

AVX Corporation (Kyocera Group)

YAGEO Corporation

Johanson Technology, Inc.

Soshin Electric Co., Ltd.

Knowles Corporation

Segment Analysis:

Segment Category | Sub-Segments | Key Insights |

By Type |

| RF Filters represent the leading type segment within the Integrated Passive Device on Glass for RF market, driven by their indispensable role in managing signal integrity across an increasingly crowded wireless spectrum.

|

By Application |

| Wireless Communication (5G/LTE) dominates the application landscape for IPD on glass, underpinned by the accelerating global rollout of next‑generation network infrastructure and the evolving complexity of RF front‑end module design.

|

By End User |

| Consumer Electronics Manufacturers constitute the leading end‑user segment in the IPD on glass for RF market, reflecting the enormous scale and rapid product refresh cycles characteristic of the global consumer device industry.

|

By Substrate Technology |

| Borosilicate Glass leads the substrate technology segment, valued for its well‑established combination of electrical, thermal and mechanical properties that are particularly well‑aligned with demanding RF application requirements.

|

By Packaging Technology |

| Wafer‑Level Packaging (WLP) emerges as the dominant packaging technology for IPD on glass for RF applications, driven by its inherent compatibility with the high‑precision fabrication processes required to produce glass‑substrate passive components at commercial scale.

|

Read Full Report: https://semiconductorinsight.com/report/ipd-on-glass-rf-market/

Download Sample Report: https://semiconductorinsight.com/download-sample-report/?product_id=142826

Click Here to Explore More-

https://semiconductorinsight.com/blog/tag/wireless-bluetooth-speaker-chips-market/

https://semiconductorinsight.com/blog/tag/electrically-erasable-rom-market-growth-2/

https://semiconductorinsight.com/blog/tag/regenerative-battery-pack-test-systems-market-trends/

https://semiconductorinsight.com/blog/tag/two-way-tower-mounted-amplifiers-market-trends/

https://semiconductorinsight.com/blog/tag/dc-dc-converters-market/

About Semiconductor Insight

Semiconductor Insight is a leading provider of market intelligence and strategic consulting for the global semiconductor and high‑technology industries. Our in‑depth reports and analysis offer actionable insights to help businesses navigate complex market dynamics, identify growth opportunities, and make informed decisions. We are committed to delivering high‑quality, data‑driven research to our clients worldwide.

🌐 Website: https://semiconductorinsight.com/

📞 International: +91 8087 99 2013

🔗 LinkedIn: Follow Us

Comments

Log in or sign up to join the conversation.