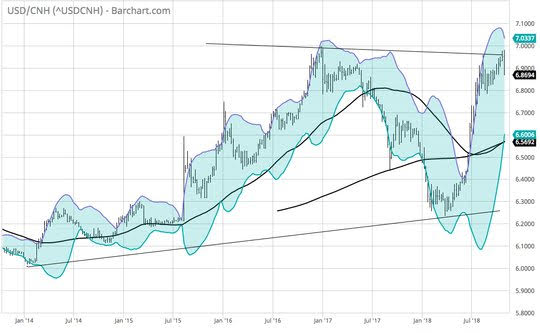

Being present emotionally, intellectually and spiritually requires effort. Meditation, exercise, diet, and communion – these all are part of the fullness of human experience and time but all require work. The natural state is entropy and markets are no different. Only work can keep a trend intact. The problem with living only in the moment, living without expectations, is that now is the best it can be and the risks for tomorrow remain. Markets are living this with this the best of times and the steady creep of peak earnings, peak growth thrives – witness the Apple earnings beat and outlook fail overnight. The bounce off the October lows (now reaching 5%) is evidence. The work behind this move rests today on Trump trade deal hopes with Xi in China. Bloomberg reported that President Trump has asked his cabinet to draft a possible China trade deal. For the cynics, this is a forced effort ahead of the mid-term elections to lift the stock market as that has become the President’s barometer for almost everything. Regardless of the future, the momentum for more money flows back to risk, away from safe-havens – particularly the USD – drives the headlines today, even with a cacophony of weaker economics from Australian retail sales to Swiss retail sales to Eurozone PMIs where Italy falls to contraction and the EU outlook dips with export orders. The mood maybe for buying value more than growth at least until the US jobs report. There are plenty of anomalies to consider today as well – Iron ore futures fell in China, EUR/CHF is lower, Oil hasn’t bounced. The tension for traders also returns with rates over risk with US 10-year yields back to 3.16% watching 3.20% for another run to 3.25% and a stop fest. On the other hand, the moment that seems to matter most is the drop in USD with the CNH revealing a larger play back to 3.80 again implying better EM and commodity markets. The move today in CNH and CNY is the most in 2-months and many see it as evidence of Chinese 7.00 defense working with stimulus plans and Xi’s determination to win back business confidence.

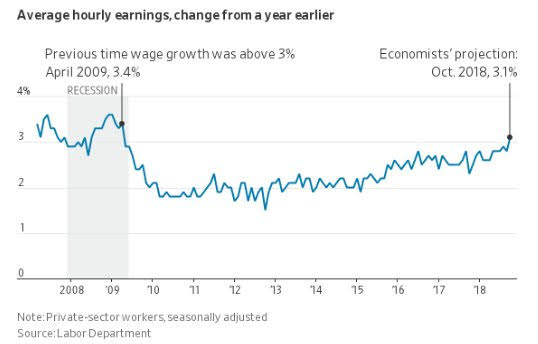

Question for the Day: Is it all about wages? The US jobs report today seems a side-show to the US/China trade deal hopes. But there is a key issue still about wages and inflation and the FOMC reaction. Higher US rates today matter and they could derail the hope-a-thon ongoing. The wage growth seems to be more important than the job creation but the whispers on jobs at 220,000 are to be respected. The ADP and other indicators point to a good report. If the unemployment rate dips below 3.7% or NFP is over 220,000 then wages not going up to 3.1% maybe less of an issue. Faith remains in a US Phillips Curve.

What Happened?

- Australia September retail sales up 0.2% m/m after 0.3% m/m – weaker than +0.3% m/m expected. The 3Q retail trade volume rose 0.2% q/q after 1.2% in 2Q. "Food retailing (0.4 per cent) led the rises," said Ben James, Director of Quarterly Economy Wide Surveys. "There was also a rise in cafés, restaurants and takeaways, which rose 0.5 per cent." The rises were offset by a fall in clothing, footwear and personal accessories (-1.2 per cent), while three industries were relatively unchanged: Other retailing (0.0 per cent), household goods (0.0 per cent), and department stores (0.0 per cent).

- Australian 3Q PPI up 0.8% q/q, 2.1% y/y. Domestic PPI rose 0.7% q/q, 1.9% while imports rose 1.6% q/q, 4.3% reflecting in part the weaker A$. Intermediate demand rose 1.2% q/q, 4.7% y/y while preliminary rose 1.3% q/q, 5.2% y/y.

- Riksbank October 23 Minutes: December or February hike still on table, September vote was 4-2 unchanged. Both Ohlsson and Floden voted for 25bps hike in October. "I do not perceive further clarification to what, in my opinion, is already a clear monetary policy plan to be particularly sensible. It would only make it even more difficult to change the plan and postpone the first increase if this were to prove necessary," Deputy Governor Jansson said. The tiebreaker for any hike remains the Governor. “It likely matters little whether the rate is raised in December or February. But on the financial markets there is, of course, great interest in exactly when a rate rise may arrive," Governor Ingves said, adding that they would "have to follow developments until December."

- Swiss retail sales -1.6% m/m, -2.7% y/y after +0.5% y/y – weaker than -0.1% y/y expected. Sales of food/beveraged fell 2.4% after +1% y/y while non-food fell -3.9% after -0.4% y/y.

- German September import prices up 0.4% m/m, +4.4% y/y while exports 0% m/m, +1.9% y/y.Import prices for energy up 4.5% m/m, 32.5% y/y while ex oil/products up 0.1% m/m, 2.3% y/y.

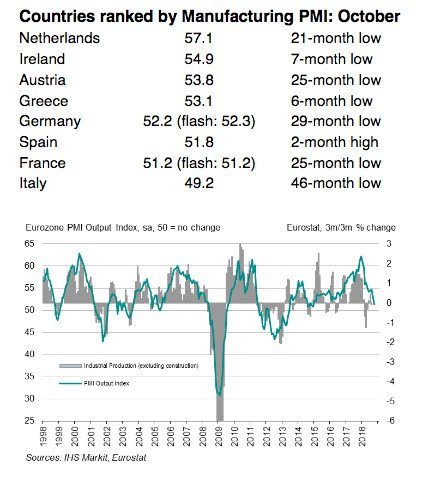

- Eurozone October final Manufacturing PMI 52 from 53.2 – weaker than 52.1 flash–26-month lows. The order books drop as exports fall for the first time in 5 ½ years. Trade concerns also pushed down confidence.

- Spanish Manufacturing PMI 51.8 from 51.4 – better than 50.8 expected. Faster gains in output and new orders but confidence down to summer 2013 lows.

- Italian Manufacturing PMI 49.2 from 50 – weaker than 49.5 expected – worst in 46 months. New orders sharpest drop since May 2013, Exports first drop in 6-years.

- French final Manufacturing PMI 51.2 from 52.5 – same as flash. Output fell into contraction for the first time in 27-months. Business confidence at 28-month lows.

- German final Manufacturing PMI 52.2 from 53.7 – weaker than 52.3 flash. New orders drop for first time since Nov 2014, first negative outlook for output in 4-years.

- UK October Construction PMI 53.2 from 52.1 – better than the 51.9 expected – second best in 16-months. Civil engineering bounced back to best levels since July 2017. House building and commercial construction also both increased at good rates but the slowest gains in 5 and 7 months respectively. New business volumes slowed sharply to 5 month lows and expectations fell to near 6-year lows. "Although total UK construction activity rose at a stronger pace in October, the underlying survey data paint a less rosy picture for the sector towards the end of the year... Construction companies again linked uncertainty to Brexit negotiations, which influenced delays to final decisions at clients," said Trevor Balchin, Economics Director at IHS Markit.

Market Recap:

Equities: The US S&P500 futures are up 0.8% after 1.06% gains yesterday. The Stoxx Europe 600 is up 1% - best in 3 weeks. The MSCI Asia Pacific rallied sharply led by Hong Kong and Korea on US/China trade hopes up over 2.75%.

- Japan Nikkei up 2.56% to 22,243.66

- Korea Kospi up 3.53% to 2,096

- Hong Kong Hang Seng up 4.21% to 26.486.35

- China Shanghai Composite up 2.70% to 2,676.48

- Australia ASX up 0.17% to 5,935.80

- India NSE50 up 1.66% to 10,553

- UK FTSE so far up 0.65% to 7,162

- German DAX so far up 1.45% to 11,634

- French CAC40 so far up 1.30% to 5,153,

- Italian FTSE so far up 1.6% to 19,493

Fixed Income: Risk-on, bonds lower. Selling of core safe-havens continues with focus on equities, earnings, US jobs. German 10-year Bund yields up 3.5bps to 0.43%, French OATs up 2.5bps to 0.78%, UK Gilts yields up 3.5bps to 1.485% while periphery gains with Italy off 8bps to 3.30%, Spain flat at 1.56%, Portugal off 1bps to 1.865% and Greece up 2bps to 4.205% - facing DBRS ratings review at close.

- US Bonds sold off across curve with jobs next key– 2Y up 2.6bps to 2.871%, 5Y up 3.6bps to 2.992%, 10Y up 3.2bps to 3.163%, 30Y up 2.1bps to 3.397%.

- Japan JGBs hit on risk-on, curves steeper with focus on BOJ tweaking. 2Y off 0.3bps to -0.136%, 5Y up 0.3bps to -0.093%, 10Y up 0.5bps to 0.114%, 30Y up 1.7bps to 0.87%. The BOJ raised the 1-3Y and 3-5Y Rinban amounts by Y50bn each. Cover ratios were the curve story – +Y350bn of 1-3Y with cover 2.87 from 2.99, +400bn of 3-5Y cover 2.61 from 2.62 while +450bn of 5-10Y with cover 2.44 from 2.60.

- Australian bonds track risk mood, ignore weaker retail sales, good auction. 3Y up 3.3bps to 2.05%, 10Y up 5bps to 2.69%. AOFM sold A$1bn of 10Y 3.25% Apr 2029 TB138 bonds at 2.6631% with 2.995 cover – previously 4.97 cover – but cover higher when adjusted for size.

- China PBOC skips open market operations, leaves liquidity unchanged on the day. The 7-day rates were flat at 2.65%. 2Y flat at 3.003%, 5Y up 5bps to 3.35%, 10Y up 6bps to 3.54%.

Foreign Exchange: The US dollar index fell 0.25% to 96.05 continuing its reversal with range 96.04-96.40. Emerging Markets are USD offered – EMEA: ZAR up 0.6% to 14.317, TRY up 0.9% to 5.46, RUB up 0.05% to 65.64; ASIA: TWD up 0.75% to 30.66, KRW up 1.4% to 1122, INR up 1.3% to 72.485.

- EUR: 1.1445 up 0.35%.Range 1.1391-1.1448 with focus on USD weakness not EUR strength. 1.1380-1.1520 keys into US jobs.

- JPY: 112.85 up 0.15%. Range 112.56-113.10 with 112 base for 114 still – EUR/JPY 129.20 up 0.45% with 130 key.

- GBP: 1.3025 up 0.15%.Range 1.2986-1.3041 with focus on 1.30 pivot and 1.2950-1.3150 risks. EUR/GBP .8785 up 0.15% - Brexit beats data and BOE still

- AUD: .7250 up 0.65%.Range .7193-1.7255 with China rebound key but A$ caps shares, NZD up 0.45% to .6685 with breakout risk for .6750 again.

- CAD: 1.3055 off 0.2%.Range 1.3050-1.3098 with data today key, but crosses/China trade story driving with 1.30 pivot for 1.2880 again.

- CHF: .9975 off 0.45%.Range .9972-1.0029 with EUR/CHF off 0.1% to 1.1425 – flashing yellow despite equities – suggest 1.00 stops open .9880 $ again.

- CNY: 6.9371 fixed 0.43% stronger from 6.9670, trades stronger no up 0.75% to 6.8725 with range 6.9354-6.8720.

Commodities: Oil mixed, Gold up, Copper up 1.9% to $2.8550.

- Oil: $63.55 off 0.20%. Range $63.26-$63.95. WTI watching $63.50 as the pivot for $62.32 next June 16 lows with $60-$65 envelope and 200-day at $65.38 key. Brent $73.04 up 0.2%, watching 200-day at $72.40 as base with $75 and $78.45 200-day resistance.

- Gold: $1235.80 up 0.2%.Range $1233-$1236. Watching USD reversal and risk-on/rates battle for driving upside with $1236 and $1243.5 the Oct 26 highs back in play. Silver up 0.45% to $14.81 watching $14.80 trend line break for push to $15 next with $14.50 base building.

Economic Calendar:

- 0830 am US Oct jobs report – NFP 134kp 190ke / earnings 0.3%p 0.3%e / rate 3.7%p 3.7%e

- 0830 am US trade deficit $53.2bn p $53.6bn e

- 0830 am Canada Sep trade surplus C$0.53bn p C$0.3bne

- 0830 am Canada Oct employment change 63.3k p 10k e / unemployment 5.9%p 5.9%e / participation rate 65.4%p 65.6%e

- 1000 am US Sep Factory Orders 2.3%p 0.4%e / ex trans 0.1%p 0.1%e

Comments

Log in or sign up to join the conversation.