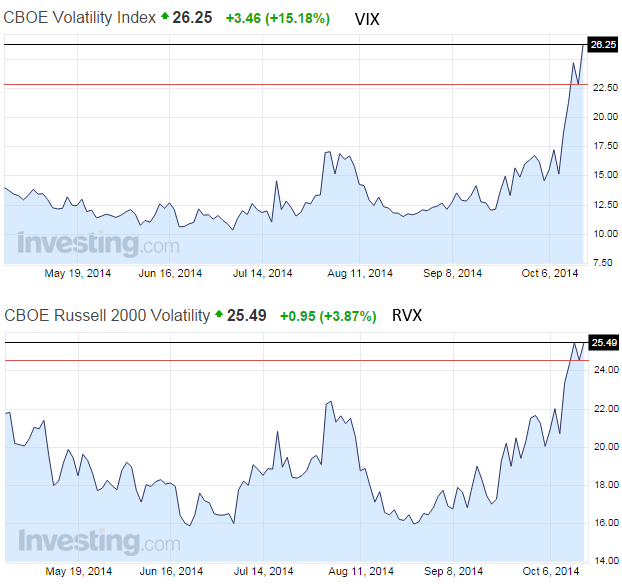

The recent spike in volatility has created a "dislocation" in US equity options markets. VIX, which is a measure of implied volatility for large cap shares is now higher than RVX - the small-cap equivalent. This is highly unusual, since small caps tend to be more volatile. Part of the issue is the outsized spike in the volatility of large energy shares due to the recent sell-off in crude oil.

Comments

Log in or sign up to join the conversation.