Gold (“Au“) and silver (“Ag“) prices are down from all-time highs in January. Will precious metal prices keep heading lower? They could, but I believe there’s good support around $4,000/oz Au and $60/oz Ag, currently ~$4,150/~$62.2.

Importantly, the factors that launched Au/Ag to all-time highs in January remain in place. Central bank buying — especially by China as it slowly but surely exits U.S. treasuries — paused briefly in some countries, but is picking up again.

Other key points include the related factors of extremely high debt levels (globally), currency debasement and rising inflation rates. We are in year six of a mined Ag supply deficit, with demand exceeding mined supply by ~160–200 million ounces.

If one is bullish on the medium-to-longer-term outlook for Au/Ag, junior miners with strong teams and solid projects in safe locations offer very significant upside potential, albeit with substantial investment risk. Undervalued, cashed-up juniors provide a degree of downside protection.

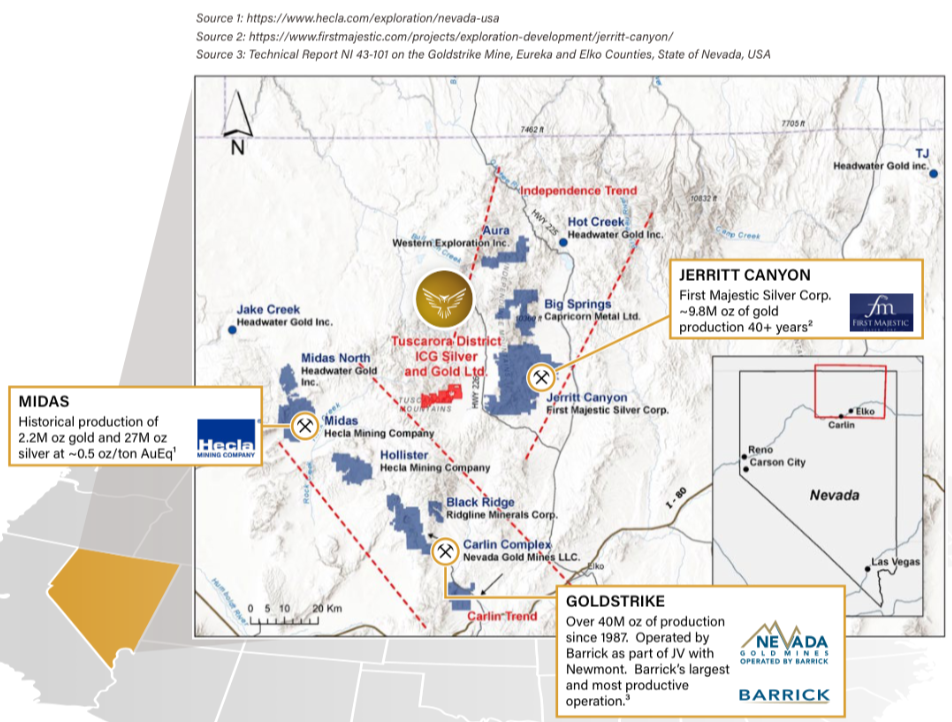

Surrounded by meaningful mines/projects, see Tuscarora in red…

Newly listed (March 2026) ICG Silver & Gold Ltd. (CSE:ICG) / (OTC: ICGSF) offers a compelling risk/reward proposition as typical junior miner risk is offset (somewhat) by a strong team, one of the world’s best jurisdictions (Nevada), a sizable land package, robust cash position, cheap valuation, and valuable historical database.

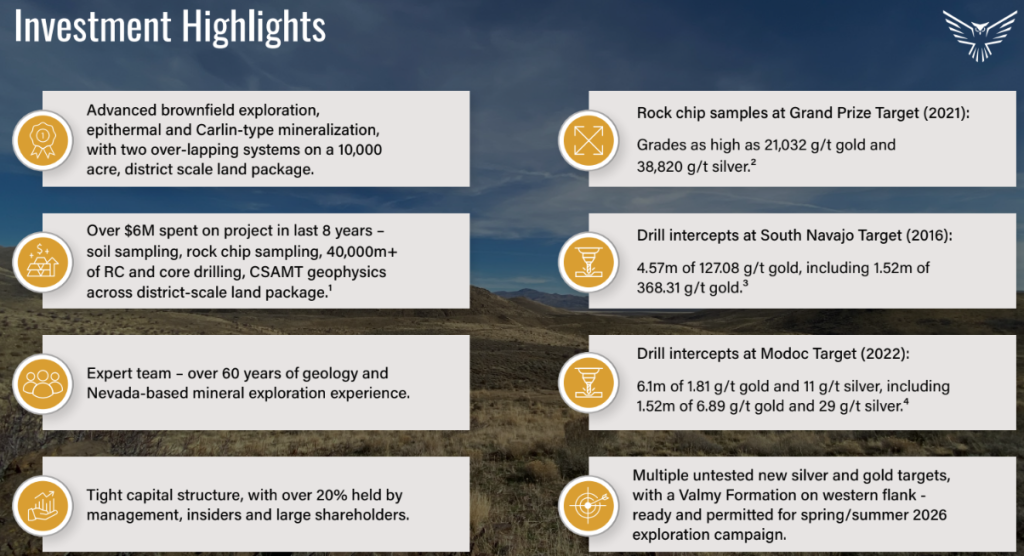

In today’s dollars, the value of the Company’s technical database, (5,000 samples, 130 line-kilometers of geophysics + other work) is estimated at C$15-$20M, exceeding the Company’s enterprise value. And, the replacement cost of 40,000+ meters of historical drilling in Nevada would be another C$20M+.

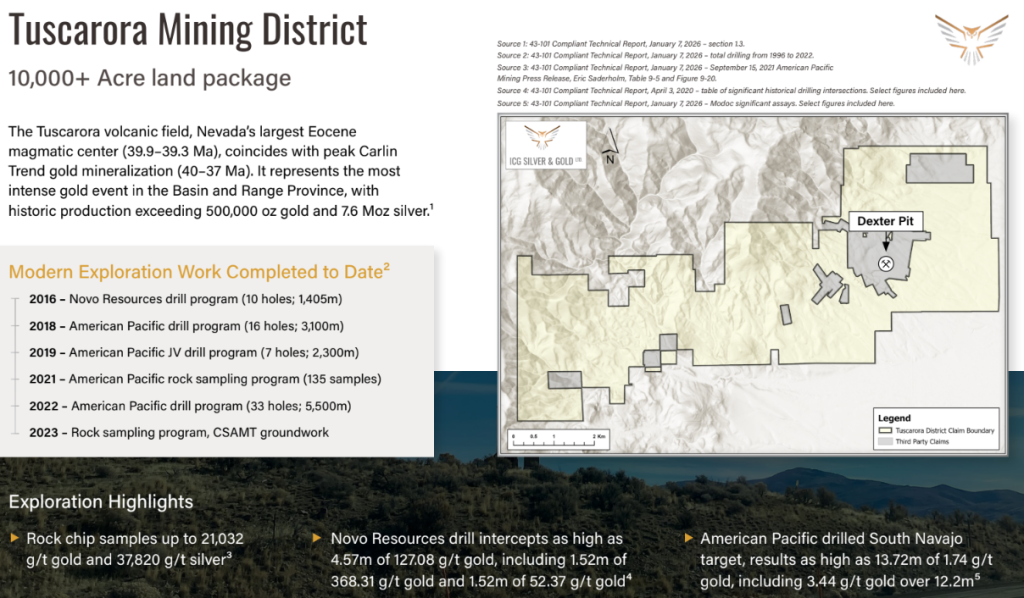

American Pacific Mining Corp., who ICG purchased the Tuscarora District Project (now 10,000 acres) from, invested over C$6M on soil/rock chip sampling, RC & core drilling, and CSAMT geophysics since 2018.

The district-scale Tuscarora District land package in NE Nevada sits at the intersection of the world-class Carlin and Independence Trends — two of Nevada’s most significant Au corridors.

Notably, the district is near substantial past-producing mines including; Jerritt Canyon (10 miles) and Midas (25 miles), and current producer Goldstrike (55 miles). Combined, Jerritt Canyon and Midas produced ~12M ounces Au + 27M ounces Ag.

Jerritt Canyon is an important factor as First Majestic Silver is bringing it back online next year. This is great news. It will attract regional infrastructure, workers, services and even more investor interest to NE Nevada.

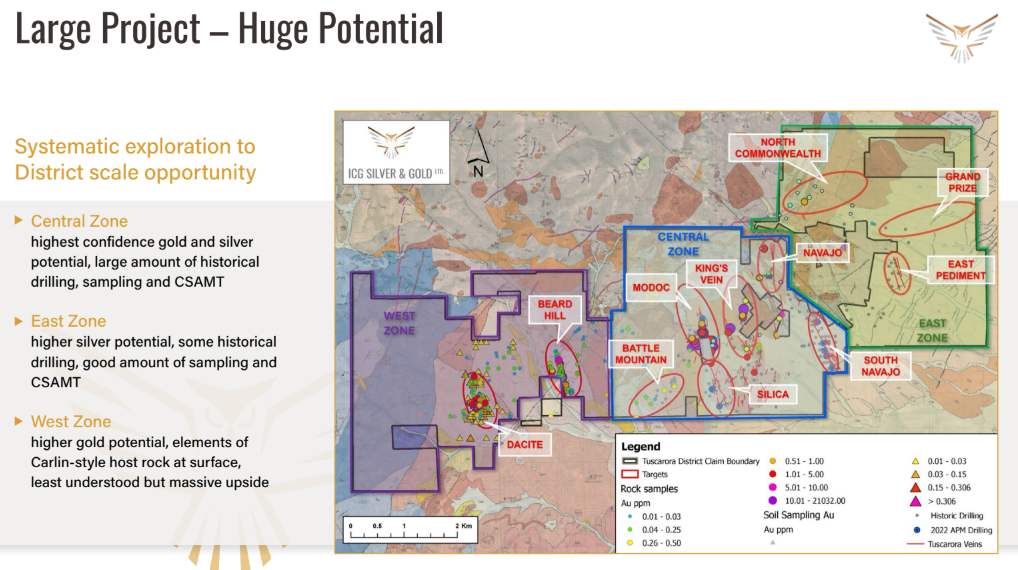

ICG’s thesis proposes two overlapping epithermal systems — one Au-dominant, the other Ag-dominant — converging in a layered configuration that previous operators left mostly untested.

A Phase 1 3,000 meter RC drill program kicked off in July. It will consist of ~15 holes. The cost is ~C$1.5M vs. the Company’s cash balance of ~C$4M. Drill results should start by August, leading to a maiden resource estimate in 1Q/27. Management has identified six high priority targets. Five have never seen modern drilling.

Pres./CEO/Dir. Steven Sirbovan commented,

“Commencing our first drill program at the Tuscarora District is a major milestone for ICG, marking the transition from district-scale compilation/target generation –> to active exploration.”

Korbon McCall, VP Exploration added, “Phase 1 drilling will allow us to test multiple shallow silver-gold targets and collect geological data to refine our district-scale model. Our objective is to assess geological controls and prioritize the strongest targets for subsequent drilling.”

The Central Zone is the backbone of the project. It will see ~80% of Phase 1 drilling, mainly on the Silica, Battle Mountain, Modoc, and King’s Vein targets. Management wants to see how those targets interact with South Navajo, where there’s a good understanding of the mineralization as it’s on trend with the historical Dexter Pit.

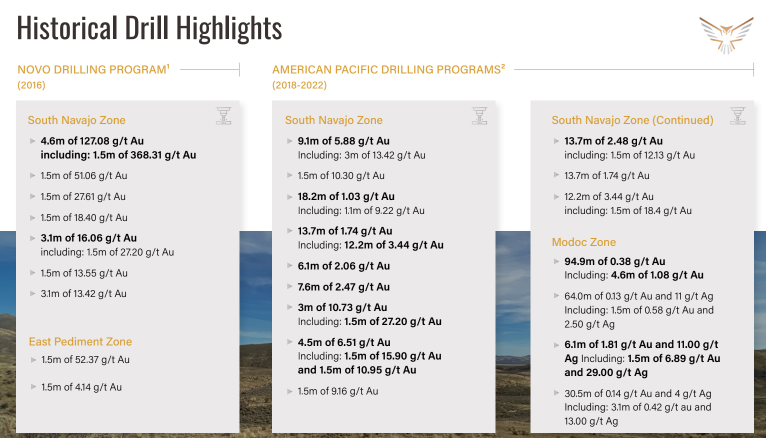

South Navajo hosts high-to-very-grade gold. As a reminder, Novo Resources drilled it in 2016, returning a remarkable 4.6 m of 127 g/t gold.

Battle Mountain is a new target acquired as part of a new claims block a few months ago, which also came with a historical database. Acquiring land with data has been a focus for ICG, adding to mineralized inventory before the drill bit has even turned.

The other 20% will be spent on the East Zone, (East Pediment & Grand Prize) where there has been meaningful historical drilling, sampling, and geophysics, but no modern drilling.

The East Zone is considered more prominent for silver. In 1997 Newcrest Resources drilled a hole at East Pediment that delivered 1.5 m of 367 g/t silver + 52 g/t gold. If drilling goes well, the team will consider expanding the campaign.

The West Zone is a newer acquisition with significant blue-sky potential. It appears to be a different system, potentially Carlin-style with bulk-tonnage characteristics. It includes the Beard Hill & Dacite targets. The Company recently completed geophysics there that shows promising features feeding known targets.

Integration of the expanded database into VRIFY visualization software has been completed. CEO Steven Sirbovan makes a big deal about the new VRIFY model. I agree with his enthusiasm. It’s important as it allows management to visualize every drill hole on the Project, bringing the opportunity to life for investors & potential strategic investors.

For example, at South Navajo, one can see a strike length of ~1.2 km by 325 m, with high-grade intercepts including; 4.6 m of 12.7 g/t gold, 18 m of > 1 g/t, and ~14 m of ~2.5 g/t). I encourage readers to watch this very recent investor webinar that nicely describes BOTH the imminent drill program, and the VRIFY model.

Mineralization remains open along strike and at depth. At Modoc and Silica, surface geochemistry aligns well with drilling. King’s Vein is an un-drilled target that looks structurally fed from depth. The East Zone targets are shallow and ready for follow-up. The West Zone remains largely untested but shows strong potential.

ICG has 43.2M shares outstanding, zero debt and ~10M warrants/options struck at C$0.50, so 54M fully-diluted shares. At C$0.42, the fully-diluted enterprise value ~C$13M, quite low for an open pit + underground prospect in Nevada.

To reiterate, there are multiple promising, untested new & existing Ag/Au targets, and considerable cash in the bank. In my view, ICG Silver & Gold has a tremendous team for a sub-C$15M junior.

CEO Sirbovan is a capital markets professional with 13+ years’ experience in Investment Banking, Private Equity & Investor Relations, focused on sub-$100M companies. He has led public & private financings, M&A, and corp. advisory work on 100+ transactions.

Earlier, he worked as an analyst at Waterton Global Resource Management, evaluating metals and mining projects across Nevada & Arizona. Steven is surrounded by a strong team including Exec. Chair Jeff Swinoga.

Mr. Swinoga is a CPA & MBA with 25+ years’ experience in capital markets, project development and mine construction. He held senior roles at Barrick (7 years), First Mining, Torex Gold, and Hudbay Minerals. He was recently Pres./CEO/Dir. of Exploits Discovery Corp.

VP Exploration Korbon McCall, Founder of McCall Geosciences, LLC, is an experienced geologist, with a project development background, focused on the western U.S.

Gary Baschuk is Dir. & Senior Technical Advisor. He brings 40+ years’ experience as a geologist, mining analyst, & investment banker, including 13 years with Barrick at the Goldstrike complex in Nevada. His focus is on small to midsized precious metal juniors.

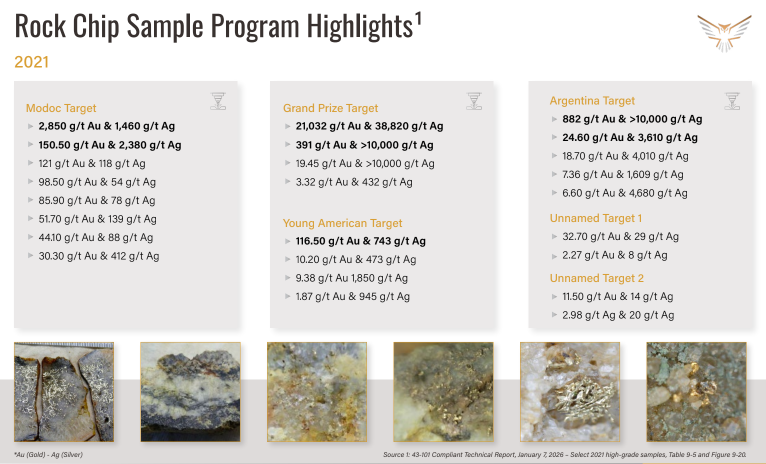

The Ag angle is an important opportunity for ICG. Despite weakness of late, Ag has nearly tripled since 3Q/2024. Historical sampling and drill results showed pockets of strong Ag, but the focus was always on Au. Note the rock chip sample grades above, up to 37,820 g/t Ag, and 11 samples > 1,000 g/t Ag.

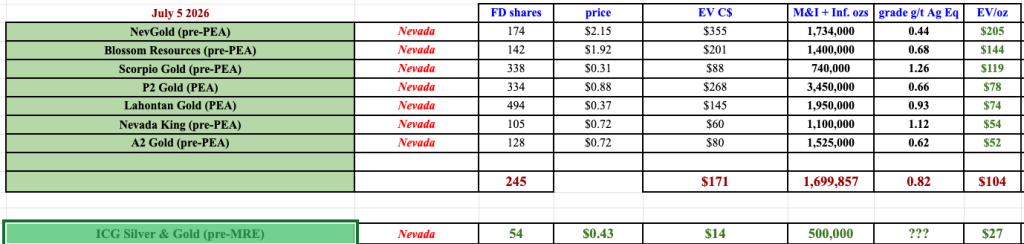

I believe ICG Silver & Gold Ltd. (CSE:ICG) is undervalued vs. the following Nevada-focused juniors. Assuming the Company can deliver 500,000 Au Eq. ounces in an MRE, (with a longer-term goal of 1M+ ounces), ICG trades at a prospective C$27/oz. vs. peers at C$103/oz.

Comparing a pre-MRE company to these more advanced, (but still early-stage), peers would be aggressive if not for ICG’s roughly C$4M in cash, enough to take it through delivery of a MRE in 1q/27.

Large players in Nevada include; Newmont, Barrick, AngloGold Ashanti, and Kinross, as well as royalty/streaming giants like Franco-Nevada, Wheaton Precious Metals and Royal Gold.

Mid-tiers include; Coeur Mining, Equinox Gold, Hecla Mining, SSR Mining, I-80 Gold, McEwen Inc., Orla Mining, and Torex Gold. Integra Resources. Hycroft Mining and First Majestic have meaningful precious metal assets in Nevada.

I believe a tsunami of global M&A — especially of U.S. projects — will lift valuations across the board. Recent acquisitions of G2 Goldfields (PEA-stage) by G Mining Ventures, and Rupert Resources (PFS) by Newmont, were done at eye-popping levels above C$500/oz.

Therefore, the timing is ideal for ICG Silver & Gold Ltd (CSE: ICG) / (OTC: ICGSF) to deliver a MRE in 1Q/27, when precious metal prices and junior miner valuations could be stronger. Today’s C$13M, fully-diluted enterprise value could be a distant memory if drilling goes well.

Disclosures/disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER] ) about ICG Silver & Gold, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market-making activities. [ER] is not directly employed by any company, group, organization, party, or person. The shares of ICG Silver & Gold are highly speculative, and not suitable for all investors. Readers understand and agree that investments in small-cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, ICG Silver & Gold was an advertiser on [ER] and Peter Epstein owned shares in the company, acquired in the open market.

Readers understand and agree that they must conduct due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reason whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector, or investment topic.

Comments

Log in or sign up to join the conversation.