Real estate professionals recently asked me if we would get back to a “normal” housing market. Normal is a challenging concept, but we can think of it as fairly steady growth, roughly in pace with the overall economy’s growth rate. We’ve been there in past eras, and we will see some stability in the coming years—but stability is punctuated by periodic surprises, often of an extremely large magnitude.

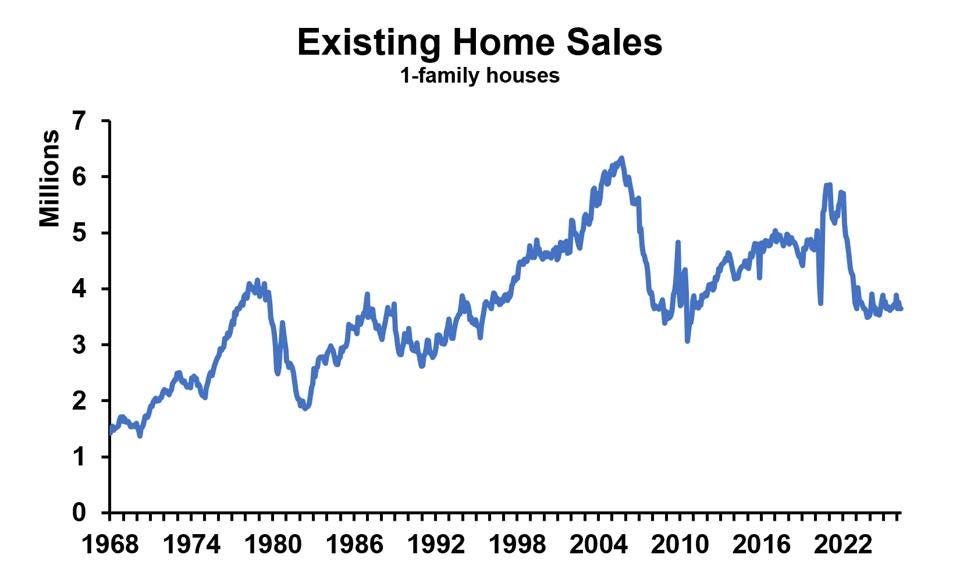

Steady gains punctuated by huge surprises./ Dr. Bill Conerly using data courtesy of the National Association of Realtors

Looking at historical data on home sales, there were time periods when the number of transactions rose fairly steadily. The data on the nearby chart are provided by the National Association of Realtors and do not contain every sale, but the data do show the underlying trends. (This article focuses on the volume of transactions more than prices.)

The late 1960s and most of the 1970s saw gains in transactions. Homes were generally considered good investments, beating the inflation that was rising in fits and starts. But this era ended in the early 1980s, when anti-inflation policy pushed mortgage rates up over 16%.

After interest rates retreated from their highs and the economy recovered from the back-to-back recessions of the early 1980s, home sales began another fairly steady rise. Although some years were better, and others leveled off, this era probably defined normal for a generation of Realtors, mortgage brokers, title insurance agents and escrow officers.

Normal ended, though, and well before many people realized it. Home sales surged, along with new construction, from the turn of the century through 2005. But that year the U.S. built over two million new housing units, for only 1.3 million additional households. Investors bought houses not to occupy but to flip. The overbuilding combined with an unstable financial system to cause the Great Recession of 2008-09, which was anything but normal.

Home sales began to rebound in 2011, then stabilized at just under five million sales per year—until the Covid-19 pandemic hit.

People stayed home in March 2020, and closings stalled with the typical two-month lag. But then the Federal Reserve moved aggressively to cut interest rates. Buyers and refinancers enjoyed seven months of mortgage rates below three percent. Even after mortgage rates increased a little, they were still incredibly low by historical standards. This was good for the real estate industry but definitely not normal.

Sales dropped as mortgage rates began rising due to the Fed’s 2022 policy reversal to fight inflation. Home sales finally settled around 3.7 million single family house transactions a year, 4.1 million with condos included. This is probably normal for the current environment.

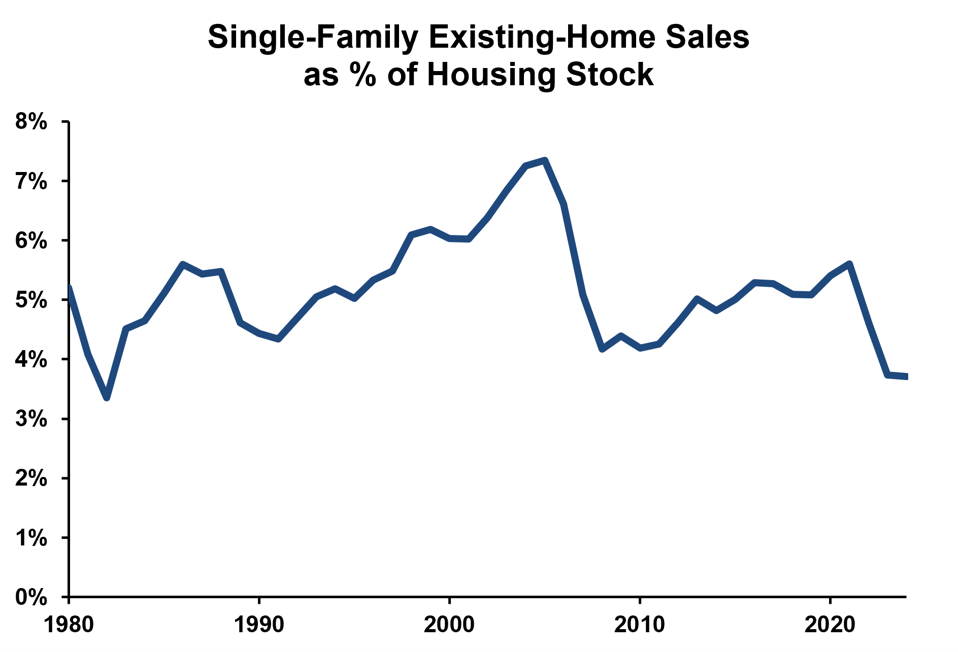

Very low sales rate now./ Dr. Bill Conerly's calculations based on data courtesy of the National Association of Realtors and the Census Bureau.

Relative to the number of housing units that exist, current volume is low. Sales have averaged about five percent of the housing stock since 1980, but recent activity is less than four percent. (The calculation requires some estimation of the housing stock, so the figures are not precise.)

Two factors drive this lower normal. The first is a long-run trend. Americans are not moving as much as they used to. Data show clearly that today people are not moving across state or county lines as frequently as they did decades ago. Lifestyle moves may not have slowed, but moves for better jobs are much less prevalent. Wage rates do not vary from state to state as much as they once did. And more families have two earners who are professionals and thus less mobile.

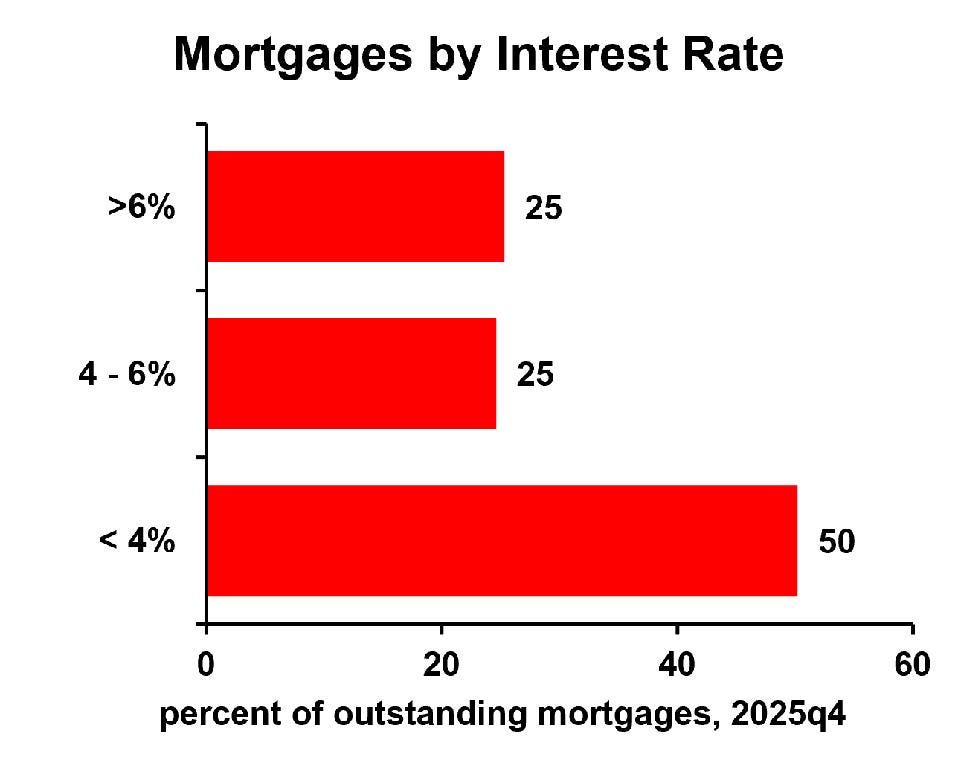

Half of mortgages are below 4%/ Dr. Bill Conerly based on data from the Federal Housing Finance Agency

The second factor depressing transactions is mortgage rate lock-in. People who bought or refinanced in the early 2020s hesitate to give up that cheap mortgage for one that will cost well over six percent. At the end of last year, about half of all mortgages were at interest rates below four percent. The lock-in effect will fade away, but gradually. A shift back to mortgage rates under four percent is very unlikely in the next few years.

Although it feels like this may be a new normal, the history shows several significant turning points that pop up unexpectedly. None of them are clearly predictable, so we should think of the occasional surprise as being normal. The surprise could be negative, such as the recessions that periodically disrupt real estate. But the pandemic ended up a very positive surprise for residential real estate professionals. So home sales will feel “normal” for a while and then change dramatically.

Business planning can optimize for the current environment, but should also include resiliency for unexpected changes. Over the long run, steady growth punctuated by an occasional huge surprise is precisely what normal looks like.

Comments

Log in or sign up to join the conversation.