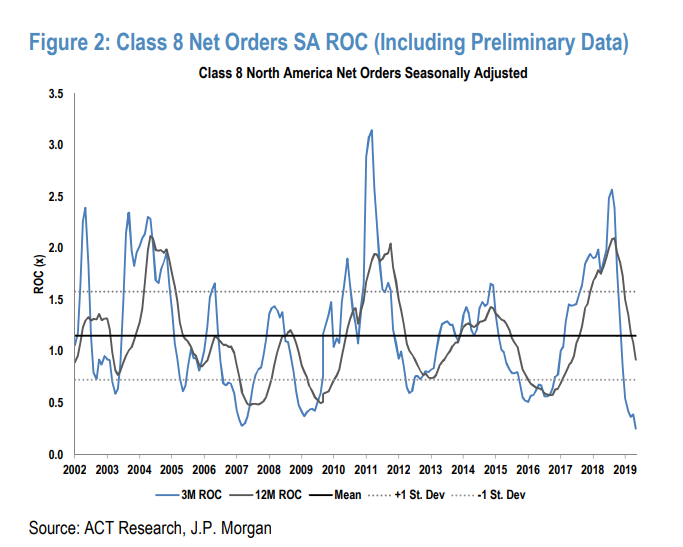

A bloated backlog of Class 8 orders as a result of a euphoric mid-2018 continues to weigh on heavy-duty truck orders in 2019.

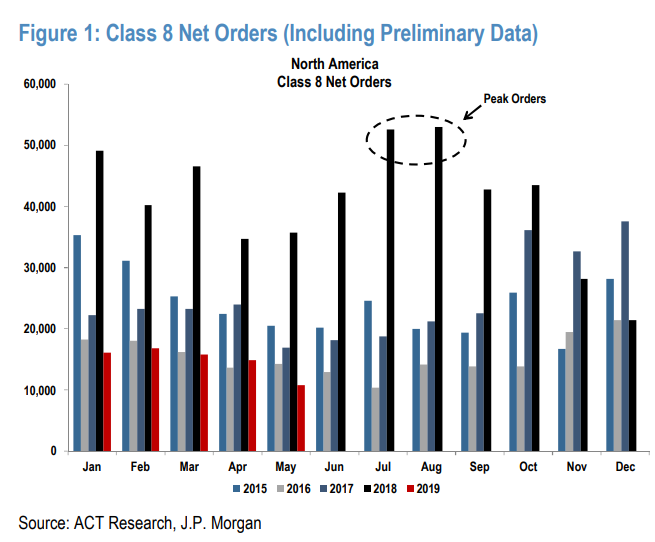

Preliminary North America Class 8 net order data from ACT Research shows that the industry booked just 10,800 units in May, down 27% sequentially, but also lower by an astonishing 70% year-over-year. YTD orders are down 64% compared to the first five months of 2018.

This chart shows the stunning difference between 2018 orders (black bars) and 2019 orders (red bars).

(Click on image to enlarge)

Class 8 trucks, which are made by Daimler (Freightliner, Western Star), Paccar (Peterbuilt, Kenworth), Navistar International, and Volvo Group (Mack Trucks, Volvo Trucks), are one of the more common heavy trucks on the road, used for transport, logistics and occasionally (some dump trucks) for industrial purposes. Typical 18 wheelers on the road are generally all Class 8 vehicles, and traditionally are seen as an accurate coincident indicator of trade and logistics trends in the economy.

In addition, a follow up note from JP Morgan noted that Class 5-7 (medium duty) net new orders were down 21% YoY and down 19% sequentially. For May, net orders were 19,300 units, down 21% YoY and down 19% MoM. Despite these trends, JP Morgan still expects 2019 production of ~278,000 units (up 2% YoY).

(Click on image to enlarge)

Kenny Vieth, ACT’s President and Senior Analyst said: “Fraying freight market and rate conditions along with a still-large Class 8 order backlog contributed to the worst NA Class 8 net order performance since July of 2016. May saw NA Class 8 orders fall below the 15,900 units averaged through the year’s first trimester, and year-to-date Class 8 net orders have contracted 64% compared to the first five months of 2018."

(Click on image to enlarge)

Speaking about the medium duty market, Vieth commented: “While the US manufacturing/freight economy has been droopy since late 2018, the medium-duty market continues to benefit from the underlying strength in the consumer economy. In May, NA Classes 5-7 net orders were 19,300 units, down 21% year-over-year and 19% from April. One has to look back 22 months to find a weaker medium-duty order month on an actual basis or just 2 months when looking at the data on a seasonally adjusted basis.”

In mid-May, we pointed out the dire picture for shipping for the rest of 2019.

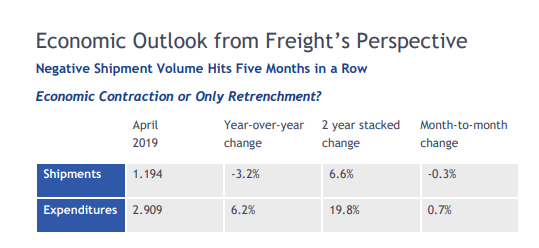

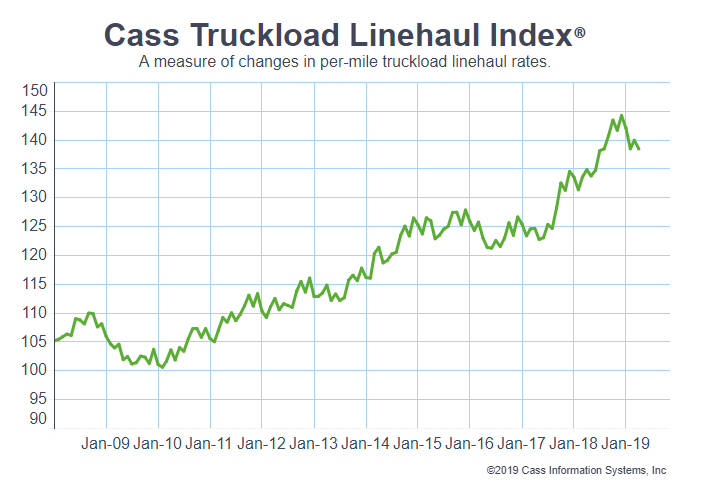

The Cass Freight Index report for the month ended April 2019 painted a dire picture for freight heading into the end of the second quarter. The report said that "continued decline" in the freight index remains a concern, pointing out that shipments have fallen 3.4% year over year while expenditures have risen 6.2%. Sequentially on a monthly basis, shipments are down 0.3% while expenditures ticked up 0.7%.

(Click on image to enlarge)

(Click on image to enlarge)

Days prior to that, we noted that used Class 8 truck sales were also crashing.

Preliminary data showed that used truck sales in the Class 8 segment fell 13% in April compared to last year, according to FreightWaves. Used truck sales as a whole fell 5% in April compared to a 25% uptick in March. The average price of a used truck rose 14%, while at the same time average miles contracted and average truck age was relatively flat, according to ACT research.

Finally, at the beginning of May we pointed out that orders for Class 8 trucks in April had also been decimated, down 57% year over year. North American Class 8 net order data showed the industry booked 14,800 units in April, down 57% from a year-ago. The decline in Aprile was also being blamed on companies filling orders from a bloated backlog of last year’s record purchases and buyers juggling remaining orders. The numbers from April were also the lowest since 2016.

Comments

Log in or sign up to join the conversation.