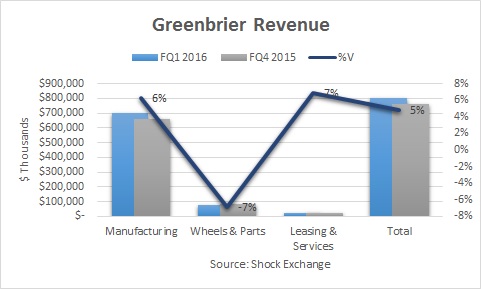

Greenbrier GBX delivered blowout FQ1 earnings this morning. The company reported revenue of $802 million and earnings per share of $2.15 on record earnings of $69 million. Revenue was up 5% sequentially and beat analysts' expectations of $759 million by a mile. However, the stock was down over 6% in mid-day trading. I had the following takeaways on the quarter.

Manufacturing Continues To Impress

Greenbrier's Manufacturing segment (nearly 90% of revenue) was impressive again this quarter. The heart of the business, Manufacturing, produces intermodal railcars, tank cars, conventional railcars, automotive railcars and marine vessels.

Revenue from the segment was up 6% sequentially. This following an 11% increase in FQ4. New railcar deliveries were 6,900 units for the quarter, up from 6,200 in FQ4. Greenbrier expects to deliver 20,000 - 22,000 units this year. Currently, it is ahead of schedule on full-year deliveries.

New Railcar Orders As Bad As Predicted

Heading into the quarter I felt new railcar orders was the most important metric to watch. Orders were 500 for the quarter -- off over 80% in comparison to FQ4 orders of 3,200. Through the first four months of the fiscal year Greenbrier garnered a total of 2,600 orders, of which 2,100 came in the month of December.

At 2,600 orders through four months Greenbrier has an annual run-rate of 10,400; this is down about 68% vis-a-vis FY15 orders of 32,400. I felt FY15 was potentially a high-water mark, and management confirmed it. Per Greenbrier's 10-Q, CEO Bill Furman had this to say:

"We anticipate and are prepared for market conditions in which order and backlog levels will likely come down from their elevated energy-driven peak."

For months I have been saying that new orders would fall in lockstep with the decline in the energy boom. With oil prices in the doldrums many shale plays find it difficult to keep drilling with prices below their break even costs. That means less tank cars are necessary to transport oil cross country. The company's prodigious backlog is also coming down. Greenbrier began the quarter with 41,300 units in backlog; after a reduction of 600 leased railcars held for syndication, 5,200 deliveries and new orders of 500, the backlog finished at 36,000 units.

Longs argue that heading into FQ1 Greenbrier had seven quarters' worth of revenue in backlog. The run-off in the backlog implies that revenue for FY17 will be less than this year's. Buying the stock now also implies that investors believe they can pick a bottom. I believe that is foolish. Until the fall off in new orders subsides or railroad traffic picks up for a few consecutive quarters I will continue to remain short. Greenbrier is well-run but there is much more pain ahead. Management now seems resigned to this fact.

Comments

Log in or sign up to join the conversation.