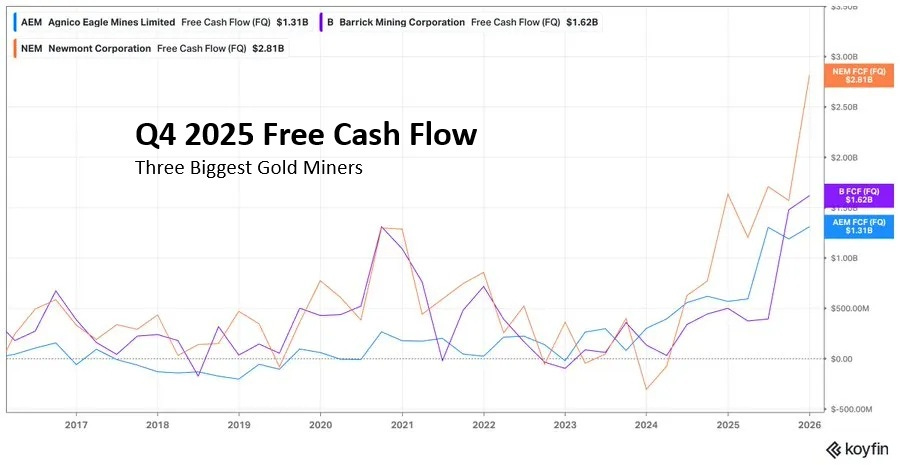

Precious metals are soaring, and well-run miners and royalty companies are generating massive amounts of cash. The following chart illustrates what it’s like for big, reasonably well-managed gold miners these days:

This is both validating (for them and us) and long overdue. But now investors are wondering what these suddenly flush miners will do with their burgeoning wealth.

The answer, of course, is that they’ll do lots of things, some of which will be spectacularly positive for their shareholders, and some of which that won’t. So let’s survey a few recent deals, starting with a huge one from the leading royalty company.

Wheaton Precious Metals Acquires Massive New Silver StreamFeb. 16, 2026 - Wheaton Precious Metals has entered into a definitive Precious Metals Purchase Agreement with a BHP Group Limited for their 33.75% portion of the silver produced at the Antamina Mine located in Peru. Upon closing, Wheaton will receive a combined 67.5% of all the silver produced from Antamina, up from the 33.75% currently delivered under the existing Glencore silver stream.

Highlights

Wheaton will fund the up-front $4.3 billion cost with $1.9 billion of cash on hand and new borrowing from credit lines.

Going forward, Antamina will contribute roughly 18% of WPM’s total gold equivalent production, making it the company’s second‑largest asset.

WPM’s net debt at closing of the acquisition will be approximately $2.4 billion, up from zero today.

$3.2 billion in projected 2026 cash flow should make the new debt manageable.

Instant Growth, More Risk, Less Flexibility

For perspective on the size of this deal, recall that royalty giant Franco-Nevada’s stake in the ill-fated Cobre Panama copper mine was about $1 billion. When that mine suddenly closed, the resulting loss was brutal.

Wheaton’s deal is four times that size, which makes it unprecedented for the royalty/streaming space, with Wheaton being just about the only player capable of even considering it.

The result: a big near-term cash flow bump, at the cost of more risk and less future flexibility. Going forward, expect impressive earnings reports from Wheaton, but relatively few new acquisitions.

OR Royalties Buys Additional Royalties in Nevada(February 24, 2026) - OR Royalties (OR: TSX & NYSE) has acquired Terraco Gold, a wholly-owned subsidiary of Sailfish Royalty Corp., which indirectly owns net smelter return (“NSR”) royalty assets on Solidus Resources LLC’s Spring Valley Gold Project located in Pershing County, Nevada. Total cash consideration is $168 million.

TRANSACTION HIGHLIGHTS

Tier-1 Mining Jurisdiction: All the NSR Royalties being acquired as part of the Transaction cover projects located in Nevada, which is ranked 4th globally as a mining jurisdiction.

Addition of Complementary Royalty Assets on a Familiar Project Now Entering Construction: The NSR Royalties being acquired complement those already owned by OR Royalties at Spring Valley. Following the closing of the Transaction, OR Royalties will own, on a combined basis: a 6.0% NSR royalty on the Schmidt Claims, a 4.0% NSR royalty on the Additional Royalty Areas, and a 1.0% NSR royalty on the Perimeter Royalty Area.

Adds to Peer-Leading 5-Year Gold Equivalent Ounce (“GEO3”) Growth Profile: The Transaction, is expected to add GEOs over-and-above OR Royalties’ recently released 2030 5-yr outlook range of 120,000-135,000 GEOs. Spring Valley is construction-ready and Solidus expects to achieve first gold production in the first half of 2028.

Instant Gratification

This deal is dwarfed by Wheaton’s, but is still big by mid-tier royalty standards. And it allows OR Royalties to immediately raise production guidance, which investors will like. View it as an accretive move with minimal financial downside.

Equinox Gold Eliminates Its Debt while Buying Back Shares

Equinox borrowed heavily to bring two mines online and complete a major acquisition. The resulting growth was impressive, but the added leverage was scary.

Then the gold bull market combined with rising production to make a quick fix possible. From the company’s Q4 report:

(February 18, 2026) - Equinox Gold achieved record production in 2025, delivering 922,000 ounces of gold. Q4 revenue rose by 18% year-over-year, to $681.40 million. The company reduced net debt from $1.4 billion in mid-2025 to just $75 million by the end of January 2026.

Said the CEO Darren Hall: “We expect cash flow to eliminate the remaining debt in 2026. The strengthened balance sheet provides greater flexibility to self-fund 400,000 to 500,000 ounces of potential annual organic growth over the next five years.”

Dramatically Better Profile

Morphing from an over-indebted mid-tier to a debt-free near-million-ounce producer is an impressive year’s work. And $5,000/oz gold makes the promised internally financed growth plausible.

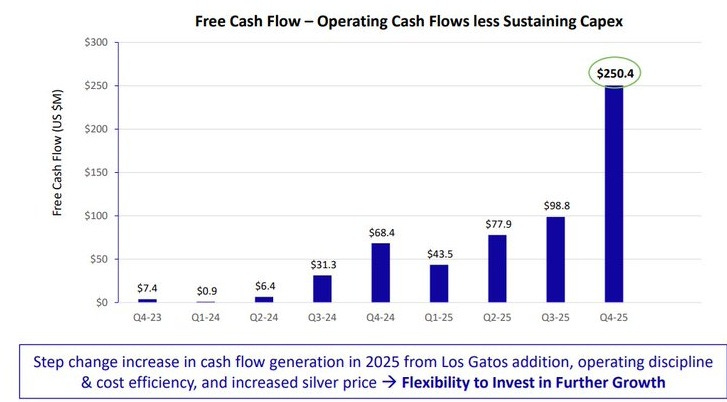

First Majestic Doubles Its Dividend

First Majestic timed a major acquisition perfectly, buying Mexican miner Gatos Silver just before the metal took off. The result: huge year-over-year gains in Q4 cash flow. From its annual report:

Record Free Cash Flow (+$182.0 million Y/Y): First Majestic generated a quarterly record of $250.4 million in free cash flow in Q4 2025 compared to $68.4 million in free cash flow in the fourth quarter of 2024.

Record Treasury Position: The Company ended the year with a record $937.7 million cash in treasury, representing a significant increase compared to $308.3 million at the end of 2024, and the highest treasury position in the Company’s history.

In January 2026, the Company announced that it is increasing its dividend per common share from 1% to 2% of net quarterly revenues earned, effective from January 1, 2026 onwards. The first payment at this increased dividend level is expected to be made in June 2026 when the Company pays its dividend for Q1 2026 in respect of revenue earned from January 1, 2026 onwards.

Nice Turnaround

First Majestic was an object lesson in questionable management as recently as 2023. But now it’s maybe the shiniest story in its sector. Increasing its dividend is a low-risk way for First Majestic to reward shareholders while retaining plenty of capital for exploration and organic growth.

With Mexico becoming an ever-riskier jurisdiction, some geographic diversification would be nice. But operationally, it’s hard to beat a multi-mine pure-play silver miner in this kind of bull market.

Elemental Royalty Offers Stablecoin Dividend

A while back, stablecoin giant Tether bought a stake in emerging royalty company Elemental. Now they’re exploring the resulting synergies:

Precious Metals Royalties Firm to Offer Dividends in Tether’s Tokenized GoldElemental Royalty signaled on Tuesday that investors will be able to receive dividends in the form of Tether’s XAUT, establishing a novel use case for tokenized gold on Wall Street.

The move is aimed at providing investors with direct ownership of physical gold, stemming from investments in gold royalties, the Colorado-based firm said in a press release. In total, investors are expected to receive a 12 cent dividend across several quarterly payments.

The company’s investors can still receive distributions in cash, as is traditional. But Elemental CEO David Cole described the company’s support of Tether’s product as innovative.

“The decision to offer investors a dividend in kind, in the form of Tether Gold, further differentiates Elemental as a forward-thinking, growth-oriented investment,” he said.

Interesting

This is unusual, but it might become more common in the future as stablecoins and other cryptocurrency variants enter the precious metals space. In the meantime, it’s risk-free for Elemental and might generate some buzz among cryptocurrency fans.

Which Brings Us To Newmont

Recall from the chart that opened this post that Newmont, the world’s biggest gold miner, also generated the most cash flow in Q4. By far.

That’s unalloyed great news, and Newmont shareholders should be ecstatic. Except for one little thing: Along with its $10 billion in annualized free cash flow, management announced 2026 production guidance that was down from 2025. Remember that the ideal miner profile is “rising production, falling costs, and higher metal prices.” Newmont has only achieved one of those.

It’s therefore likely that Newmont will face pressure to use its cash to boost production. So expect a hat trick: a big dividend increase, more share buybacks, and the acquisition of one or more tier-one properties. That means our portfolio’s mid-tier producers might attract some high-premium offers in the coming year.

Conclusion

Each of the deals profiled here looks reasonable in its own way. They’re either related to existing assets or easily reversed if they don’t work out. This is a sign of a healthy, well-balanced industry.

But it won’t always be thus, because cash flow of this magnitude is virtually guaranteed to trigger a feeding frenzy. That will be fun and maybe wildly profitable for those who stay the course in high-quality miners.

Comments

Log in or sign up to join the conversation.