Gold stocks have had a tough summer, pounded lower by their metal’s periodic sharp selloffs. Mired in its low-interest low-volume summer doldrums, gold has suffered big hits on flaring Fed-rate-hike fears and Trump’s war re-escalating. Resulting persistent weakness has left gold and gold-stock technicals deeply oversold, and herd sentiment quite bearish. But this is a great setup for a major mean-reversion autumn rally.

Seasonality is the tendency for prices to exhibit recurring patterns at certain times during the calendar year. While seasonality doesn’t drive price action, it quantifies annually-repeating behaviors driven by sentiment, technicals, and fundamentals. We humans are creatures of habit and herd, which naturally colors our trading decisions. The calendar year’s passage affects the timing and intensity of buying and selling.

Gold stocks display strong seasonality because their price action amplifies that of their dominant primary driver, gold. Gold’s seasonality generally isn’t driven by supply fluctuations like grown commodities see, as its mined supply remains relatively steady year-round. Instead gold’s major seasonality is demand-driven, with global investment demand varying considerably depending on the time in the calendar year.

This gold seasonality is fueled by well-known income-cycle and cultural drivers of outsized gold demand from around the world. Starting in late summers, Asian farmers begin to reap their harvests. As they figure out how much surplus income was generated from all their hard work during the growing season, they wisely plow some of their savings into gold. Asian harvest is followed by India’s famous wedding season.

Indians believe getting married during their autumn festivals is auspicious, increasing the likelihood of long, successful, happy, and even lucky marriages. And Indian parents outfit their brides with beautiful and intricate 22-karat gold jewelry, which they buy in vast quantities. That’s not only for adornment on their wedding days, but these dowries secure brides’ financial independence within their husbands’ families.

So during its bull-market years, gold has tended to enjoy sizable-to-strong autumn rallies driven by these sequential episodes of outsized demand. Naturally the gold stocks follow gold higher, amplifying its gains due to their profits leverage to the gold price. Today gold stocks are once again back at their most-bullish seasonal juncture, the transition between the typically-drifting summer doldrums and big autumn rallies.

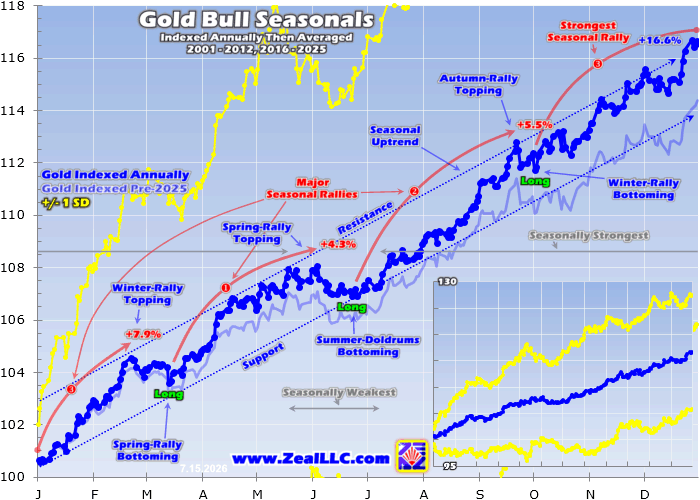

Since it is gold’s own demand-driven seasonality that fuels gold stocks’ seasonality, that’s logically the best place to start to understand what’s likely coming. This old research thread focuses on modern bull-market seasonality, as bull and bear price action are quite different. Over the past quarter-century or so, gold enjoyed bull years in 2001 to 2012 then again from 2016 to 2025. Intervening bear years ran 2013 to 2015.

In past gold-stock-seasonality essays I’ve analyzed all those many gold years, but their accumulation is making that space-prohibitive. Now fully 22 of these last 25 years qualify as gold-bull ones, and thus are included in this analysis. Naturally prevailing gold prices varied wildly across that long secular span, from just $257 in early April 2001 to a lofty $5,394 in late January 2026! So gold’s raw price data sure isn’t comparable.

The vast range of gold levels spread over all those many years has to first be rendered in like-percentage terms in order to make them perfectly comparable with each other. Then they can be averaged together to distill out gold’s bull-market seasonality. That’s accomplished by individually indexing each calendar year’s gold price action to its final close of the preceding year, which is recast at a common indexed baseline.

I’ve always used 100 which makes subsequent gains easy to parse. From that, all gold action of the following year is recalculated which normalizes all years to the same simple scale. For example gold trading at 110 simply means it has rallied 10% from the prior year’s close. Gold’s current seasonality from 2001 to 2012 and 2016 to 2025 is rendered in dark-blue, with its prior year’s pre-2025 data in light-blue.

Across all these modern gold-bull years, gold has averaged fantastic 16.6% annual gains! With a stellar track record like that over 22 of these last 25 years, gold certainly deserves way more popularity with investors. Gold’s strong and persistent gains across this past quarter-century are concentrated in its autumn, winter, and spring seasonal rallies, which respectively averaged an impressive 5.5%, 7.9%, and 4.3%.

The autumn rally kicks off gold’s long strong season, launching out of the dreaded summer doldrums. That sentiment wasteland is gold’s weakest time of the year seasonally, mostly plaguing June. Doldrums’ lack of recurring gold demand surges usually leaves this metal drifting listlessly sideways to lower. But low volume as traders check out for summer vacations makes gold unusually vulnerable to outsized selloffs.

Normally there’s not much news in the summer doldrums as traders’ interest in markets fades to its lowest ebb. But this year proved anomalous with two unique major things traders are trying to understand. The first is how Trump’s new Fed chair will run the FOMC, and the second is how long Trump’s war with Iran will last and how broad its economic impact will be. All gold’s recent selloffs were fueled by these factors.

On Jobs Friday June 5th, gold plunged 3.7% shattering well-established multi-month high-consolidation support after a big nonfarm-payrolls beat ignited Fed-rate-hike fears. The leading GDX gold-stock ETF collapsed 8.8% on that! On June 10th gold dropped another 4.3% on Trump threatening to resume his war on Iran, as gold’s backward war trade reasserted itself. GDX fell another 4.9%, plumbing even-lower lows.

On June 17th Trump’s new Fed chair ran his first FOMC meeting, heavily emphasizing fighting inflation to achieve price stability. Despite Kevin Warsh’s refreshing new approach being way more likely to liberate gold from Fed tyranny, over the next five trading days it plunged another 7.8%! That hammered GDX yet another 14.5% lower. Then just this Monday, gold dropped 2.7% on Trump threatening to toll the Strait of Hormuz.

He said the US would demand an eye-popping 20% of the value of all cargo transiting that critical global chokepoint! GDX fell 2.9% on that madness, which Trump reneged on the very next day. Realize these are all one-off events. The Fed rarely gets new chairs, and never like this with a president trying to fire the former one to force rate cuts. And Trump’s endless flip-flopping on his war of choice is wildly unprecedented.

Having all this unique chaos unleashed in gold’s fragile summer doldrums was really bad luck. Had either development hit in any month other than June, normal gold trading would’ve much more readily absorbed any kneejerk selling. All this carnage has left gold down 5.9% year-to-date as of midweek, which is 94.1 in indexed terms. Yet over 22 of these last 25 years, gold has averaged a far-higher 108.4 at this same time!

That long secular mean equates to $4,676 today, which would require gold to surge a major 15.3% from midweek levels! And that would merely be a mean reversion, not the typical overshoot to the upside after prices are dragged down way out of kilter. So gold is really poised for a big autumn rally this year. Those typically run from late June to late September, with gold again averaging 5.5% gains over the last quarter-century.

Gold’s technicals argue for a far-larger autumn rally this year, while a bearish fundamental development could dampen it. On the price side, this Monday’s $3,999 gold close on Trump’s crazy threat of US 20% tolls on the Strait slammed gold back to just 89.4% of its baseline 200-day moving average. That was the most oversold gold has been in fully 3.8 years, since late September 2022! Such extremes fuel huge rebounds.

In early October 2023, gold’s last bull was born at a much-higher 94.6% of gold’s 200dma. Over the next 27.8 months, this metal soared 196.4% achieving a monster record cyclical bull! The more oversold gold gets, driving more herd bearishness among speculators and investors, the greater the odds for massive mean-reversion rallies to erupt. Those can ultimately attract enough capital to grow into major uplegs or bulls.

Given today’s deeply-oversold gold conditions after its anomalous summer-doldrums selloff, gold ought to at least double its modern autumn-rally average surging 11%ish by late September. And triple or even quadruple its secular +5.5% average wouldn’t be surprising at all. The main wildcard might not be this new Warsh Fed or even Trump’s endlessly-contradictory Truth Social posts, but Indian seasonal demand.

Few countries have been hit harder by Trump’s war than India. It relies on imports to satisfy a whopping 7/8ths of its oil demand, with half of that coming from the Persian Gulf before the war! The resulting way-higher oil prices exacerbated a currency crisis in India, its rupee plunging to record lows against the US dollar as rupees were sold to buy oil. Yet India can’t significantly slow its oil imports without crushing its economy.

So India’s government went after its second-largest import to try and shore up its currency, gold. In mid-May import duties on gold were more than doubled from 6% to 15%! While Indians love gold, they are shrewd price-conscious buyers. At the time, analysts estimated those higher taxes would slash big Indian gold demand by 1/4th or so. So Indian post-harvest and wedding-season gold buying this year could be muted.

But the gold-demand impact could very well prove much less dire. In mid-May when those import duties were hiked, gold was running near $4,650. Midweek it was about 13% lower, more than offsetting that 9% jump in tariffs. Gold’s serious 26.0% reckoning in US-dollar terms from late January to late June may be more than enough selling to motivate Indian buyers. And 15% import duties on gold are nothing new there.

Before being slashed to 6% in July 2024 to promote India’s domestic gold-jewelry industry, they had been at this same 15%. And Indian gold demand had been strong for years despite such high import duties. And political pressure along with lower oil prices could lead India’s government to loosen some of its new gold import restrictions. Oil was running around $108 per barrel in mid-May, but has fallen over 25% by midweek!

I did a deeper analysis on Indian gold demand in a recent essay on gold’s seasonal launchpad nearing if you want more. The key takeaway today is while India’s higher import tariffs could retard gold’s autumn-rally demand this year, it likely won’t be anywhere near as much as analysts feared. India’s weak currency and resulting surging domestic inflation could actually encourage big investment in gold, tariffs be damned.

The major gold miners of GDX tend to amplify material gold moves by 2x to 3x, so a conservative 10% autumn rally in gold could easily catapult gold stocks 20% to 30% higher by late September. I wouldn’t be surprised to see a 15%-to-20% gold rebound given this year’s summer-doldrums extremes, which should fuel proportionally-larger gold-stock autumn rallies. That’s how gold-stock seasonals have played out.

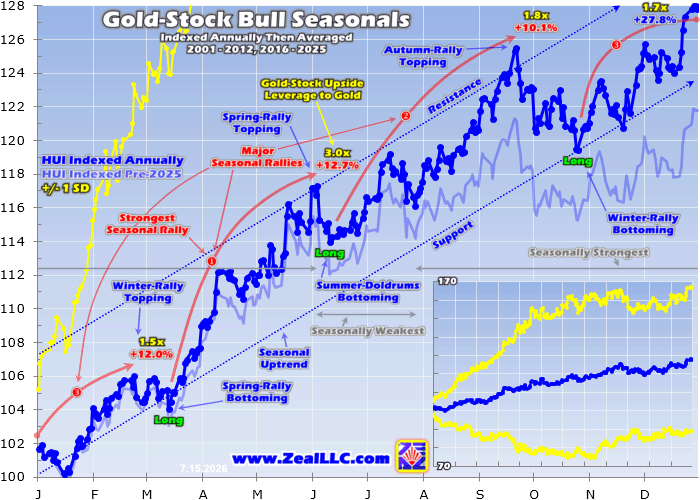

Since GDX was only born in May 2006, it is too young to encompass this secular-seasonality-research thread. So the older HUI NYSE Arca Gold BUGS Index is used instead, which was GDX’s predecessor. It still includes most of the same major gold miners at similar weightings, which makes the HUI and GDX functionally-interchangeable. If charted without numeric scales, they’d be indistinguishable from each other.

This chart applies this same annual-indexing-averaged-together methodology to the HUI during all these same modern gold-bull years. If GDX was substituted instead starting in 2007, the results would be all but identical. Despite long being ignored by the great majority of speculators and investors, gold stocks have proven one of the best-performing sectors in this past quarter-century. They deserve way more respect.

In these same modern gold-bull years of 2001 to 2012 and 2016 to 2025, the major gold stocks averaged phenomenal 27.8% annual gains! That’s epic across 22 of these last 25 years, and Wall Street should be crowing about this. Instead this contrarian sector still remains largely ignored. Because of their metal, gold stocks also enjoy distinct autumn, winter, and spring seasonal rallies over the same timeframes as gold.

These have averaged 10.1%, 12.0%, and 12.7% gains respectively, so the autumn rally kicking off gold’s strong season is the weakest for gold stocks. That 10.1% is only 1.8x gold’s 5.5% average, weak leverage under GDX’s usual 2x-to-3x range. After a quarter-century intensely studying and actively trading gold stocks with much success, I suspect lazy late-summer markets with traders still checked-out is the main reason.

Gold’s capital flows on outsized demand surges fueling its autumn rally are international, mainly Asian led by India. Yet the mostly-US-listed major gold stocks of GDX require American investors to buy them to fuel big rallies. The general vacation season for traders isn’t concentrated in June like gold’s summer doldrums, but extends through July and much of August into the long Labor Day weekend in early September.

Psychologically American market summers effectively run from Memorial Day weekend in late May to that Labor Day one. So along with general interest in the markets, gold-stock buying wanes in June, July, and much of August during vacation season. In addition to anticipating and taking family trips, traders who are still paying attention remain wary of gold and gold stocks after their summer doldrums damage sentiment.

But sometime around mid-August, a few things converge to rekindle gold-stock interest and traders start rushing to add positions. Kids return to school, formally ending the summer vacation season for a huge chunk of speculators and investors. Gold’s autumn rally powering higher from mid-July to mid-August starts getting noticed, fueling increasing bullishness. And gold miners report Q2 results during that same month.

In years where average gold prices are relatively high in Q2s by recent standards which is normal during bulls, gold miners’ earnings tend to be good. They report how they fared operationally and financially in Q2 mostly from late July to the mid-August deadline. If sufficiently strong, those Q2 numbers fuel plenty of interest among professional investors who follow quarterlies including funds motivating them to buy.

And these upcoming Q2’26 GDX results are going to prove amazing, gold miners’ second-strongest ever achieved! I wrote a whole essay last week explaining that forecast in depth. The gold miners are about to report near-record profits last quarter, while their stocks remain quite undervalued relative to underlying corporate earnings. And in sympathy with its metal, GDX also just collapsed to deep-secular-low oversoldness.

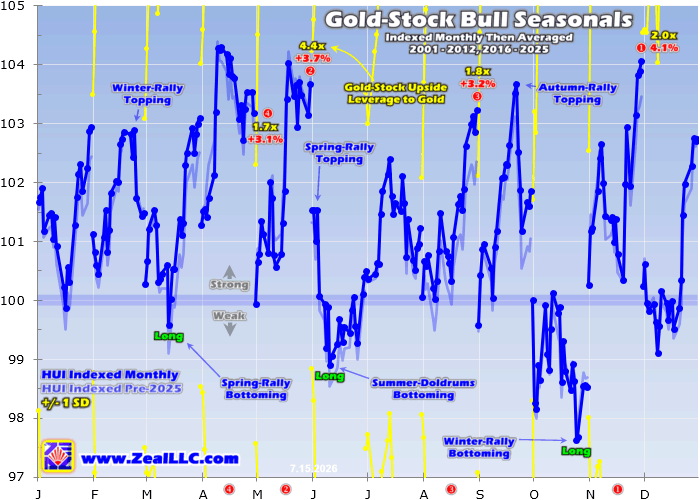

This Monday GDX plunged to just 83.8% of its 200dma, the most oversold gold stocks have been in fully 3.7 years since early November 2022! So they too are a coiled spring ready to explode higher with gold in a powerful mean-reversion bounce. Seasonally gold stocks tend to surge in early July, retreat most of the rest of this month, then really start powering higher by mid-August. This last chart emphasizes that action.

Instead of years, it carves gold-stock seasonality into more-granular calendar months using this same indexing-then-averaging methodology. In these same modern-gold-bull years, August has proven major gold stocks’ third-best month of the year seasonally with hefty 3.2% average gains! That makes late June into late July good times to add gold stocks relatively-low ahead of their major autumn, winter, and spring rallies.

During the heart of the summer doldrums in June, the HUI has just averaged little 0.4% gains. That drifting drives apathy in this small contrarian sector, which needs fast rallying to catch traders’ attention. Things improve in July despite that secondary selloff in its second half, with better average gains of 1.2%. Then capital inflows really start rocking in August late in or soon after Q2’s earnings season, driving that big 3.2%.

That momentum carries into September until gold’s autumn rally peaks late that month. The major gold stocks average strong 3.7% month-to-date gains into that, before correcting ahead of their subsequent winter rally. Again all that adds up to a 10.1% autumn-rally average, but can grow way larger when gold rebounds out of oversold conditions entering this seasonal strength. That’s sure as heck the case today.

So despite summer 2026’s anomalous gold selling spawned by new-Fed-chair-hawkishness fears and Trump’s loose-cannon Truth posts on his war, we’ve been rebuilding our newsletter trading books. It has been challenging with stoppings on kneejerk gold plunges, but we’re still loading up on fantastic smaller mid-tier and junior gold miners with superior fundamentals that really outperform majors during gold uplegs.

The bottom line is gold and its miners’ stocks are heading into their strong season. That’s kicked off by their robust autumn rally, which tends to run from late June to late September. And this year’s is likely to prove much larger than usual on big mean-reversion buying. Both gold and GDX were just hammered to their most-oversold levels in nearly four years, on Fed-rate-hike fears and Trump’s capricious war rants.

With gold’s reckoning slicing off over a quarter of its value since late January, the autumn rally’s usual Indian gold demand shouldn’t suffer too much from higher import duties there. And gold miners are about to report their second-best quarter ever, driving their already-low valuations even lower and attracting in fund investors. All this makes for a very-bullish autumn-rally setup this year, with outsized gains likely nearing.

Comments

Log in or sign up to join the conversation.