Agnico Eagle, one of the big three gold miners and arguably the best-managed, just reported quarterly earnings that were either great or hugely disappointing, depending on one’s point of view.

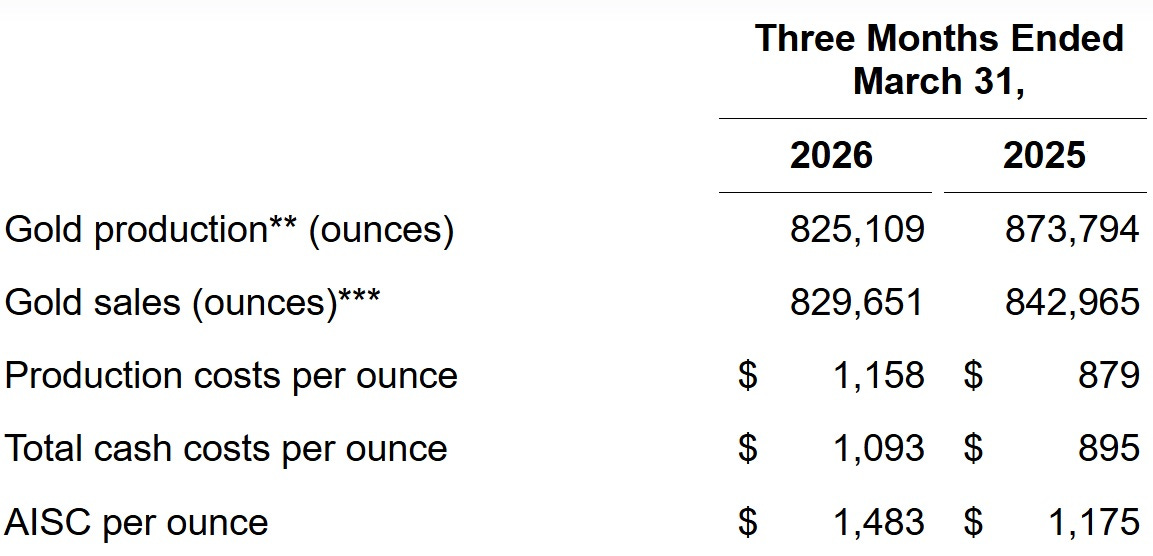

First, the ugly: lower production and higher costs.

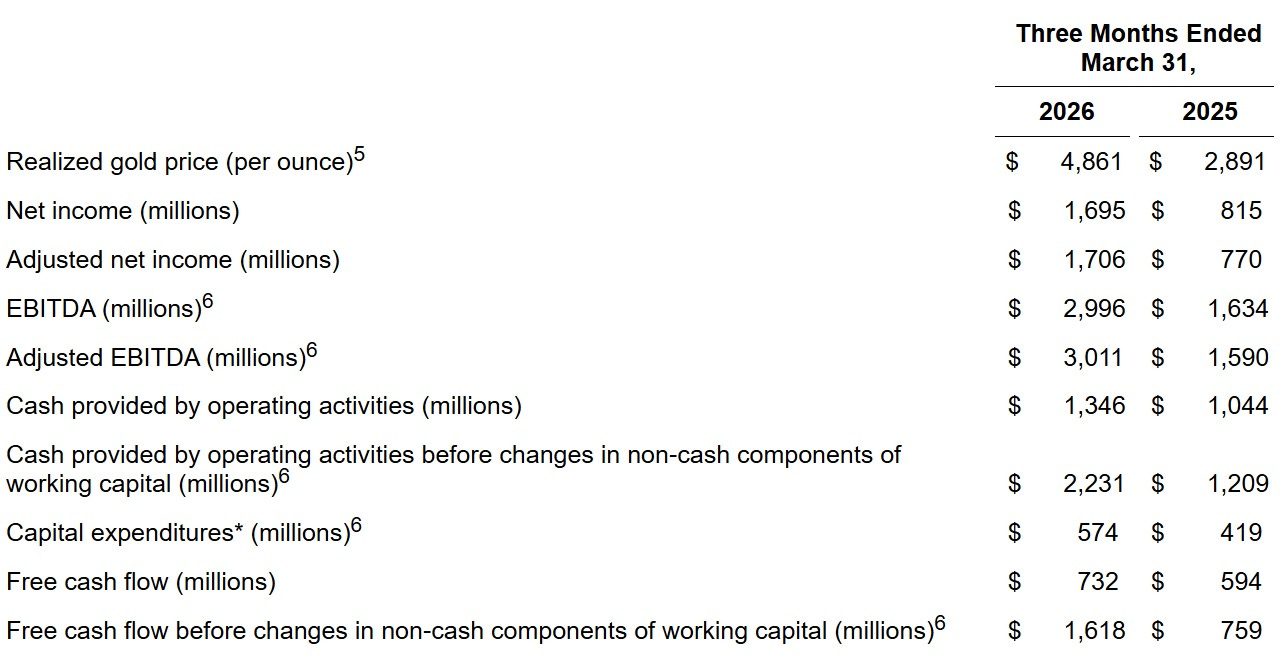

Now the gorgeous: Record high revenues, operating margins, and net income, with around $1 billion of free cash flow.

How did lower production and higher costs beget record earnings? Obviously, the price of gold was way up in Q1. When the price of what you’re selling jumps, your margins swell and cash pours in.

But It Only Works While Gold Is Rising

One month into this year’s second quarter, gold is down slightly from its Q1 average, which, other things being equal, means sequentially lower earnings and cash flow for Aginco. Investors will not be happy.

Solving the Problem

Agnico’s management saw this day coming and has decided to aggressively boost its future growth:

Agnico Eagle moves to consolidate Finland’s gold district in nearly C$4B deal

(Kitco News) - Agnico Eagle (AEM) Mines announced today that it will take control of the Central Lapland Greenstone Belt in Finland through three simultaneous transactions, cementing its position as the dominant gold producer in northern Europe.

The senior producer will acquire Rupert Resources for approximately C$2.9 billion, paying 0.0401 Agnico shares plus a contingent value right of up to C$3.00 per Rupert share — a 67% premium to Friday’s close. Separately, Agnico will buy Aurion Resources (AU) for C$2.60 per share in cash, valuing the junior at roughly C$481 million, and purchase B2Gold (BTG)’s 70% stake in the Fingold joint venture for US$325 million.

The prize is Rupert’s Ikkari deposit, a 3.5-million-ounce gold system sitting just down the road from Agnico’s flagship Kittilä mine, which still holds 3.3 million ounces in reserves and has been producing since 2009. Stitching the three land packages together hands Agnico a contiguous district in one of Europe’s most mining-friendly jurisdictions, with obvious synergies across permitting, infrastructure, and its existing Finnish workforce.

The deal is the latest sign that senior gold producers are willing to pay up for long-life ounces in stable jurisdictions, with bullion trading near record highs and greenfield discoveries increasingly scarce. For Agnico, it extends the same “district consolidation” playbook it ran in Quebec’s Abitibi belt — but this time in Lapland.

Closing is targeted for early Q3 2026, subject to shareholder and court approvals.

Note The Premium

There are two takeaways here:

A miner with Agnico’s buying power doesn’t have to accept declining production. It can buy pretty much whatever it wants, and should therefore be expected to grow by paying up for high-quality assets.

The other big gold miners are in the same boat, with stagnant production but soaring cash flow. So expect them to adopt the same growth-through-acquisition strategy. That means many of our Portfolio’s smaller gold miners will receive high-premium bids in the coming years. Which, in turn, means the commodity ride is just getting started. Keep buying the dips.

Comments

Log in or sign up to join the conversation.