I have been a rabid Gilead GILD bull for some time now, but when the facts change so does my thesis. My previous article stated that the Wyden-Grassley report could punish Gilead; it apparently got longs' dander up. Seeking Alpha author Brad Kenagy also took issue with my sell thesis. Below is my response to Brad:

Point #1

"If the furor over Gilead's HCV pricing reaches the court of public opinion, the company will be hard-pressed to differentiate itself from other firms like Valeant (NYSE:VRX) or Turing."

The report from Senators Wyden (Oregon) and Grassley (Iowa) suggests that Medicare spent over $8B on Sovaldi and Harvoni prior to rebates. Given that Medicare and Medicaid are large buyers of HCV drugs, they wield a lot of power; the Veterans Administration and U.S. prisons could also add to that buying power. I envision a scenario where these entities and/or the government negotiate steeper discounts on HCV drugs from Gilead going forward. Gilead should be the government's primary focus because Harvoni is best-in-class in terms of cure rates and efficacy, vis-a-vis the competition.

Secondly, individuals infected with HCV tend to be highly sophisticated about the disease and its price; after all, they are the ones who use or need the drug. Assuming steeper discounts are garnered by the government, I also envision HCV infected patients demanding similar discounts. Otherwise, it would appear that the government is picking the winners - members of Medicare and Medicaid, veterans and the prison population - over other members of the public.

Once the debate over the price of Harvoni enters the public consciousness, what would be Gilead's rationale for not offering steep discounts to everyone? It would be difficult to use the "we need to recoup R&D" argument since there is no evidence that Harvoni's cost is tied to R&D spending. Moreover, prices for drugs offered by Turing and Valeant are also divorced from R&D costs. I envision this debate becoming a political football; something has to give and it could be the price of Harvoni.

Point #2

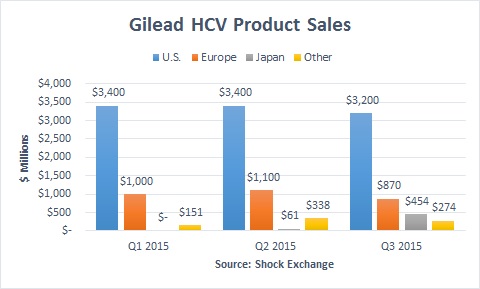

"At some point HCV sales in Japan could flatten out just like those in the U.S. and Europe."

Gilead's respective HCV product sale for Q1, Q2, and Q3 2015 were $4.6 billion, $4.9 billion and $4.8 billion, respectively.

Sales in the U.S. and Europe appear to have peaked; combined U.S./Europe product sales were $4.4 billion, $4.5 billion and $4.1 billion in Q1, Q2 and Q3, respectively. If not for the $454 million in sales from Japan, total HCV product sales would have declined.

For the next few quarters, the ramp up in Japan may be able to offset by further declines in the U.S. and Europe. However, if Japan's sales flatten out then total product sales will likely be flat to declining. As of now, the ramp up in Japan is masking a deterioration of product sales in the U.S. and Europe.

Point #3

As HCV Sales Go, So Goes Gilead

In Q3, non-HCV sales were up about 6% Q/Q, outpacing the growth in HCV sales. The company's TAF based HIV treatments have shown antiviral efficacy with less dosage and fewer side effects. However, at 58% of total revenue, HCV products will still drive revenue, earnings and sentiment around the stock. I believe HCV product sales will slow, either due to declines in volume, price or both. I recommend trading ahead of the thesis; if one waits until declines in HCV sales materialize, it may be too late.

Comments

Log in or sign up to join the conversation.