The U.S.–Iran ceasefire was looking strained before it appeared to break after both sides traded military strikes yesterday. President Trump said on Wednesday that he believes the ceasefire and interim agreement to end the war are “over.” He added that while U.S. negotiators can continue talking with Iran, he personally considers the effort “a waste of time.”

The path ahead for the Middle East crisis remains uncertain, and monitoring key indicators that serve as proxies for market sentiment has returned to the fore. Hanging in the balance as the conflict twists and turns anew: inflation risk, economic activity, monetary policy, and the risk appetite across financial markets.

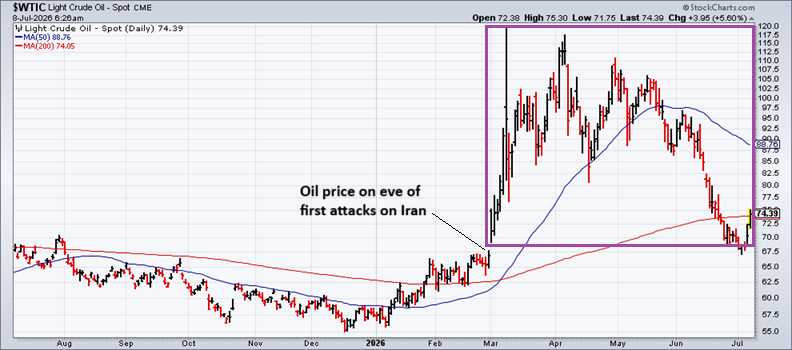

The price of crude oil remains on the front line of real‑time reaction, and so it’s not surprising that the weeks‑long slide sharply reversed this week. As the trading week began, the war premium had fully unwound, and WTI (the U.S. benchmark) briefly traded under $70 a barrel. The rebound to above $74 on Tuesday keeps prices at the low end of the range that has prevailed since the first attacks on Feb. 28. If oil continues to climb, many of the recent assumptions about a disinflationary pivot will come under renewed scrutiny.

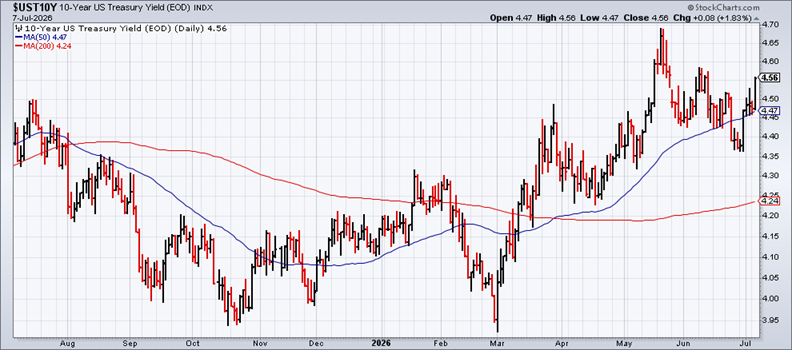

A similar reversal has unfolded in the U.S. 10‑year Treasury yield, which jumped to 4.56% on Tuesday. That’s a sign of renewed anxiety tied to the latest round of conflict in the Gulf and the potential for a renewed inflation pulse.

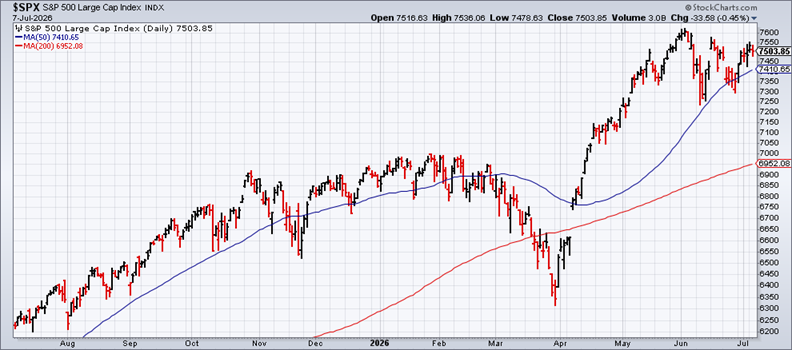

The stock market remains relatively calm as the S&P 500 Index continues to trade in a range, but the stoic sentiment will be tested as the murky conditions of the Middle East play out in the days and weeks ahead.

The moderate rebound in confidence that the Federal Reserve might be able to delay or sidestep rate hikes is under renewed pressure. Although markets are still pricing in moderately high odds for no change in monetary policy at the next FOMC meeting on July 29, the probability of a rate hike in September is estimated at roughly 66%, based on Fed funds futures.

The danger here is what appears to be Iran’s emerging game plan: holding out for increased leverage ahead of the November U.S. midterm elections rather than pursuing a deal with the Trump administration. By driving up oil prices and Treasury yields, the regional conflict threatens to force a more hawkish Federal Reserve stance, leaving the U.S. economy exposed to the long‑term consequences of Mideast instability.

Given the mercurial decision‑making on both sides, the outlook remains highly fluid. Once again, watching how oil prices and Treasury yields reprice the latest spike in geopolitical risk is essential for monitoring the crisis.

As Yogi Berra famously said, “It ain’t over till it’s over,” and it definitely ain’t over.

Comments

Log in or sign up to join the conversation.