old and precious metal juniors have been under pressure. If one thinks the multi-year bull market has ended, there’s little reason to keep reading. I think prices will recover in the coming months. Having said that, Majors & mid-tier producers are killing it at current pricing.

A massive tsunami of M&A is incoming, highlighted by the takeouts of G2 Goldfields (PEA), and Rupert Resources (PFS), each at over C$550/oz in the ground. Another clear and growing trend is Majors & mid-tiers making multiple strategic investments in promising projects/companies, even early stage situations.

Companies like Agnico Eagle, Newmont, AngloGold Ashanti, Gold Fields, Centerra Gold, Alamos Gold, Kinross & B2Gold have been actively securing stakes in juniors.

Gold (“Au“) is up a substantial +165% from its 4-yr low, but investors seem more focused on it being down -22% from nearly $5,600 in late January. Despite the doom & gloom, one thing that never fails to impress is blockbuster drill results. That’s why I’m writing about Graycliff Exploration (CSE: GRAY) / (OTC Pink: GRYCF).

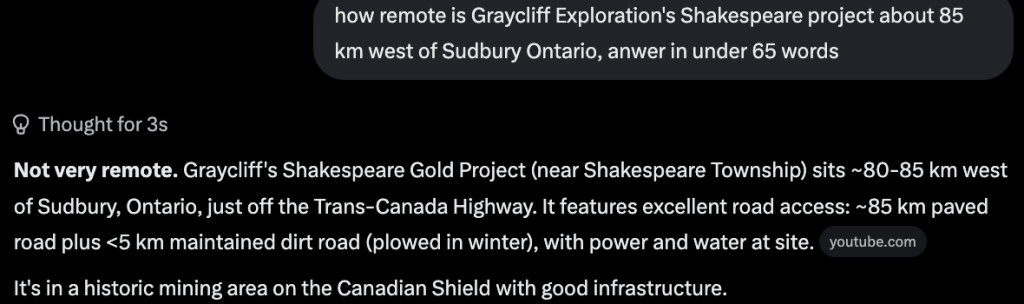

Graycliff is focused on 1,360 hectares of prospective ground, roughly 85 km west of Sudbury, Ontario, on the prolific Canadian Shield. The Company has drilled 12,500+ meters, with visible Au mineralization and significant Au assays in numerous holes.

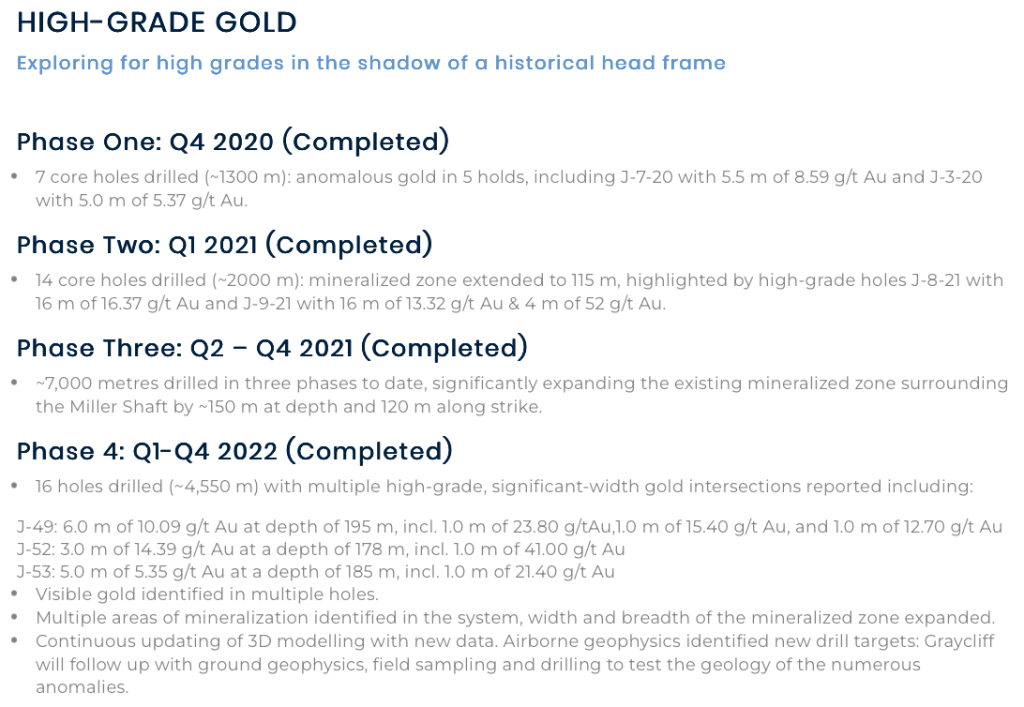

The flagship Shakespeare Gold Project hosts historic production, namely the Shakespeare Gold Mine, which operated from 1903-1907, producing ~2,959 ounces from ~8,599 tonnes (10.7 g/t Au), mined from six underground levels. The Project is just off the Trans-Canada Highway with power & water at site.

To the extent that some of the historical workings can be utilized, like the mine shaft, (to be determined), that could present savings in cap-ex. If the team can safely access underground levels, it might be able to drill more efficiently & cheaply (being studied).

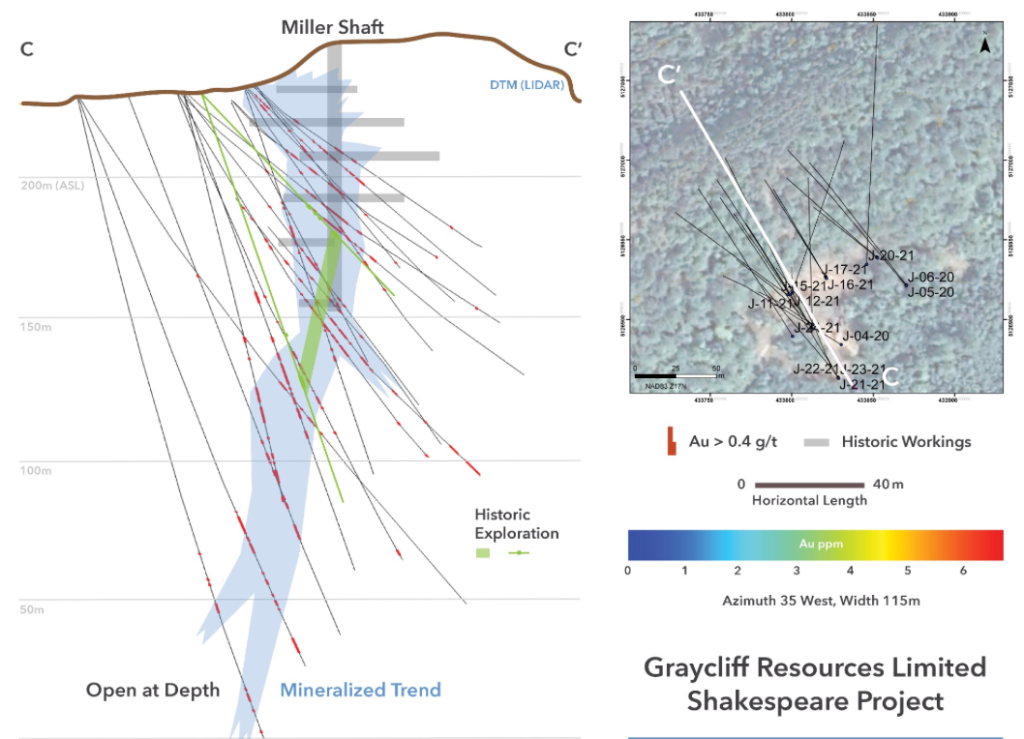

Historic exploration was completed intermittently between 1938 and 2014, including trenching, sampling & drilling. Subsequently, there were notable drilling successes like: 5.5 m of 8.59 g/t Au in Q4/20, [16 m of 16.37 g/t Au, 6 m of 13.32 g/t & 4 m of 52 g/t] in Q1/21. Additional medium-to-high-grade results through 2022, incl. 4.8 m of 46.0 g/t Au.

The following charts of Canadian-listed Au producers, developers, and explorers shows the Top gram-meter readings for 2025, 2024 & 2023. Most of the companies are valued at C$1B+, Alamos at > C$15B. By contrast, Graycliff is valued at C$6M (C$0.36/shr).

On June 2nd, Graycliff entered the extremely rare, ultra-high grade Au club. I’m not talking about Top 10% or Top 5%, but Top 1%… Top 1% for a project that’s not that remote, (see above image) or in a scary jurisdiction. Ontario is ranked #2 globally in the latest annual Fraser Institute Mining Survey.

If Graycliff’s 7.0 meters of 454 g/t Au was a 2025 event, it would have been comfortably in the #3 spot. Looking at the 2024 Canadian-listed leaderboard, Graycliff, at 3,180 gram-meters, would have been #2 behind DPM Metals, (market cap C$9.8B). For 2023, Graycliff’s blockbuster result would have been #1.

Top gram-meter hits from Canadian-listed Au companies 2023-2025

Yes, Graycliff reported a really great hole, but the key is that the Company has under 17M shares outstanding and a tiny market cap. Management will report on two additional holes in the coming weeks. Should we expect another bonanza intercept?

No, not nearly as strong as the first hole, but that’s not required to keep this story in the headlines. Having said that, there could be strong intervals, we have to wait a few weeks. Why would anyone sell shares in this exciting junior at a C$6M market cap?!?

I believe investors could be underestimating the importance of this great discovery. Instead of today’s negligible market cap on 17M shares, what if this news came a year from now with 3x as many shares? The upside potential would have been far lower.

Imagine if a prominent investor like Eric Sprott, Frank Giustra, or Michael Gentile were to announce an investment? To be clear, this is very high risk, far from a sure thing. If the market cap were C$50M awaiting the results from two more holes, that would be entirely different.

In looking at four other big drill result situations from Sterling Metals, Prospector Metals, San Lorenzo Gold, and Tectonic Metals, they were up an average of +192% two weeks after news broke. In mid-May, Targa Exploration was up as much as +294% weeks after announcing visible gold — but, with no assays!

A week after Graycliff’s results, the stock is +64%. Shares would probably be higher if not for talk on ceo.ca of a capital raise. Yet, if 15M shares were issued at C$0.32 to raise C$4.8 (gross proceeds before fees), total shares would remain under 32M. I have no knowledge of the exact plans, but I imagine a raise is coming.

How much should a company with game-changing ultra-high-grade drill results be worth? A lot more than the pro forma market cap (perhaps ~32M shares x C$0.36 = C$11.5M). Importantly, C$4.8M would provide months of exploration runway to meaningfully unlock the true potential of the Shakespeare project.

Management is carefully looking into doing a bulk sample of thousands of tonnes. If that were to deliver high-grade material, it could potentially generate meaningful free cash flow for a company the size of Graycliff. More importantly, it would greatly de-risk the Shakespeare Project. A bulk sample would be next year’s business.

There are several ways the next two holes could contribute to de-risking and building the Graycliff opportunity. For example, the holes could provide evidence on whether visible/free gold (as seen in Hole A) is consistent.

More core provides samples for initial leach tests, gravity concentration, or flotation studies — critical for assessing if high-grade material is economically viable. The next two holes should show grade distribution and rock characteristics across slightly different positions, helping in resource modeling and planning for a bulk sample.

Even far more moderate grades in the same structural corridor could point to the system’s persistence and orientation (continuity). Broader lower-grade halos around high-grade zones would be positive for overall tonnage potential. The next two holes will shift focus from “discovery-wow factor” to engineering & development fundamentals.

Is it possible I’m talking up a single drill result too much? Yes, but only if the interval turns out to be a one-hit wonder, an outlier that leads nowhere. Certainly possible, but unlikely (in my view). The best defense against a poor outcome is the very cheap entry point. Readers should note, this need not become a multi-million ounce deposit.

Given the C$6M market cap, 500,000+ high grade ounces would be a home run. I’m not saying there’s evidence of 500k+, (if no continuity established, there may never be a resource) only that it’s a much more attainable outcome than the multi-million ounce goals of much larger juniors.

A few days after the June 2nd drill results, management entered into an agreement to acquire a 100% interest in 13 strategic mineral claims (208 ha) located in Shakespeare township, located within the same highly prospective geological corridor. According to the press release,

“Securing the claims will allow Graycliff to immediately expand upon the search area for the mineralized footprint defined by its recent drilling success. The expansion will ensure the company commands the strike extensions and areas that cover parallel structures that could be very important in future exploration as the company explores to determine the full scale of the Shakespeare gold system.”

Graycliff Exploration’s game-changing news is just a week old. A lot will happen in the next year. We could see good-to-great news, or future drill results could be mediocre (or worse), leading to diminished prospects for Shakespeare.

However, although early-stage, a Top 1% interval of 7 meters (not sub 1 meter), is extremely encouraging. And, the low share count / tiny market cap makes Graycliff an attractive risk/reward proposition.

Disclosures/Disclaimers

Peter Epstein & Epstein Research [ER] have no current or prior business relationship with Graycliff Exploration. However, [ER] is pursuing Graycliff as a potential paying client and is optimistic Graycliff will engage. Therefore, readers should consider [ER] biased in favor of the Company and take that fact into consideration upon reading the above article. The content herein contains only public information obtained from press releases, the Company’s website, sedar filings and conversations with management. As of June 9, 2026, Peter Epstein of [ER] owns no shares in the Company but might acquire shares in the near future.

The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Graycliff Exploration, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market-making activities. [ER] is not directly employed by any company, group, organization, party, or person. The shares of Graycliff Exploration are highly speculative, and not suitable for all investors. Readers understand and agree that investments in small-cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

Comments

Log in or sign up to join the conversation.