A year ago, I looked at the dividend safety of natural gas shipper Flex LNG (FLNG) . At the time, it had a whopping 13% yield. However, falling free cash flow and a payout ratio that exceeded 100% meant the stock received an “F” rating.

Fortunately for shareholders, the quarterly dividend has remained intact at $0.75 per share, giving the stock a current yield of more than 11%.

But can that $0.75 dividend stay afloat?

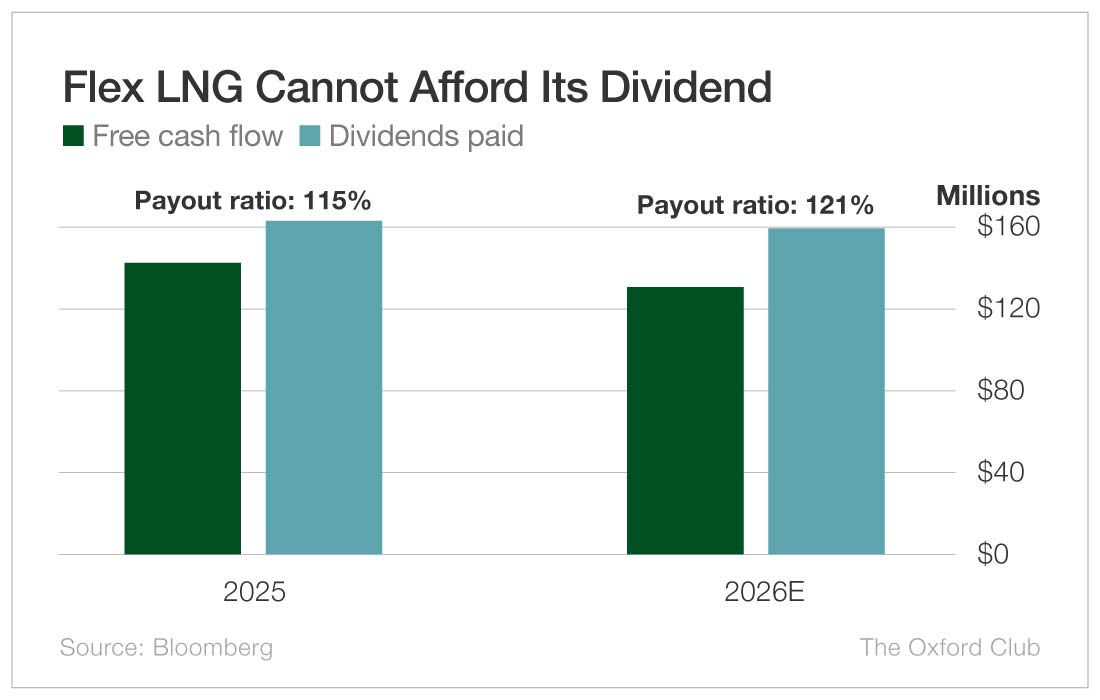

When I reviewed the stock last year, one problem was that free cash flow was projected to fall to $152 million in 2025 from $183 million the previous year. The actual numbers in 2025 were even worse than expected.

Flex LNG generated just $141 million in free cash flow in 2025 while paying out $162 million in dividends. That came out to a payout ratio of 115%. In other words, for every $1 of free cash flow it made, the company paid out $1.15.

Think of it like this: If you make $100,000 a year and spend $115,000, that extra $15,000 has to come from somewhere. You either have to take it out of savings or borrow it.

The same thing goes for companies. When a company’s amount paid in dividends exceeds its free cash flow by that much, it’s a big concern.

This year, free cash flow is forecast to drop further to $131 million. Flex LNG is projected to pay shareholders $159 million in dividends, increasing the payout ratio even more to 121%.

Falling free cash flow and a too-high payout ratio mean the dividend is even less safe than it was a year ago.

Flex LNG shareholders should not be surprised if the dividend is reduced in the next year.

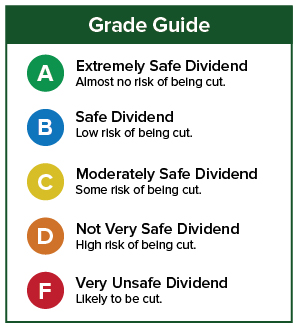

Dividend Safety Rating: F

Comments

Log in or sign up to join the conversation.