Investing in high-quality businesses trading at attractive valuation levels can lead to superior returns over the long term. However, finding these kinds of opportunities is much easier said than done.

More importantly, when a good business is trading at a discounted valuation, this is usually because there is some uncertainty hurting the stock in the short term, so capitalizing on these opportunities requires a long-term time horizon and a contrarian mindset.

In the case of Facebook (FB), regulatory risk, transitioning business dynamics, and general market conditions are weighing on the stock in recent months. On the other hand, the business fundamentals look as strong as ever and the stock is fairly attractively valued for such a high-quality business.

Strong Fundamentals

The data privacy scandals have produced some reputational damage to Facebook. Besides, many users are transitioning from the traditional Facebook platform towards Instagram and WhatsApp, and ads in stories generally carry lower prices than newsfeed ads. In addition to this, the company has significantly increased its spending in key areas related to security, data privacy, and product development in recent quarters.

These factors are making financial performance harder to predict in the short term, and they are hurting the stock price. However, the cold hard numbers show that Facebook keeps firing on all cylinders as of the most recent earnings report.

The company produced $16.9 billion in revenue during the second quarter of 2019, an increase of 28% versus the same quarter in the prior year. The figure surpassed market estimates, and the growth rate even accelerated versus a 26% year over year increase in revenue during the first quarter of 2019.

GAAP operating income was $4.6 billion during the quarter, representing a 27% operating profit margin. Excluding the impact of the FTC accrual, the operating margin would have been approximately 12 percentage points higher. The company ended the quarter with 39,700 full-time employees, up 31%. Even if Facebook keeps aggressively investing in areas such as security and product development, the business model keeps generating outstanding profitability.

More than 2.1 billion people used at least one of Facebook's apps on a daily basis in June of 2019 and more than 2.7 billion people were active on a monthly basis. This massive scale is a crucial source of competitive advantage for a market leader in social media.

The bigger the size of the platform, the more value it generates for its users. Platforms such as Facebook, Instagram, Messenger, and WhatsApp are increasingly more valuable when they provide more opportunities for interactions of all kinds. Users attract each other to the leading social networks, creating a virtuous cycle of growth and increased competitive strength for Facebook over the long term.

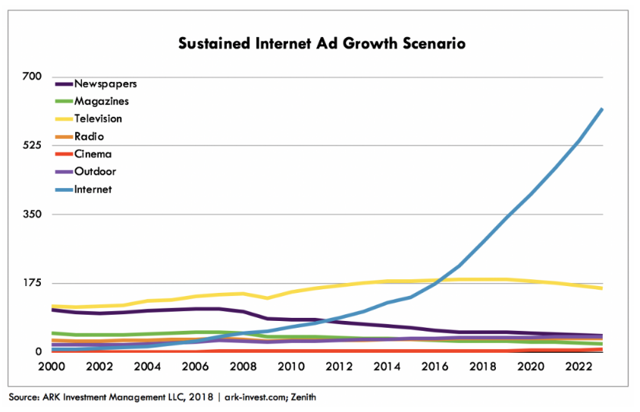

The online advertising industry is not only taking money away from traditional media but also enlarging the size of the cake by attracting new advertisers. Online advertising can be done with smaller budgets and in a more personalized way than traditional advertising, so many small businesses that cannot afford traditional advertising have a viable opportunity in the online advertising channels.

According to data from ARK Investment Management, five years from now, the advertising market as a whole could be worth as much as $900 billion, and two-thirds of that money could come from online advertising.

Source: ARK

Beyond advertising, the company is exploring opportunities in areas with big potential such as online shopping and payments. Instagram Checkout is in closed beta mode, and the company has recently launched a new feature that enables creators to tag products in their posts, providing an easy way to shop through Instagram without leaving the app.

According to management:

It's early days for shopping on Instagram, but we're excited about this over the long run.

The company is testing WhatsApp Payments in India, and it's planning to expand into new markets over the coming months. The Libra project is still giving the first steps, and it probably won't have much of an impact on the business in the coming quarters. Nevertheless, the project has intriguing potential over the years ahead.

Attractive Valuation

Facebook is currently expected to make $8.1 in earnings per share during 2019 and $9.27 during 2020. Based on these estimates, the stock is trading at a forward price to earnings ratio of 22 for 2019 and 19 for 2020.

This valuation is clearly attractive when considering that Facebook is producing revenue growth rates well above 20% year over year with recurrent operating margins in the neighborhood of 40% of sales.

It is important to keep in mind that valuation is always dynamic. Ratios such as forward price to earnings are calculated on the basis of earnings expectations in the year ahead. If the company can consistently deliver numbers above expectations, then the stock price needs to rise too in order for the valuation to remain stable.

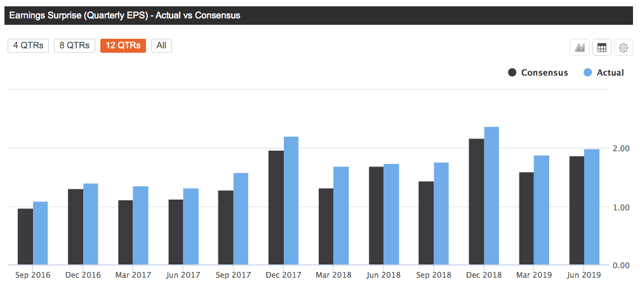

Facebook has an impressive track record in that area, the company has delivered earnings numbers above Wall Street estimates over the past 12 quarters, which is not easy to do in such a dynamic industry.

Source: Seeking Alpha Essential

The fact that Facebook has outperformed earnings expectations in the past does not guarantee that the company will keep doing so in the future. However, it's good to know that management tends to under-promise and over-deliver when it comes to earnings. As long as this trend remains in place, it could be a considerable tailwind for Facebook stock.

Valuation needs to be analyzed in the context of other return drivers. A company producing strong growth and consistently delivering earnings above expectations deserves a higher valuation than a business producing mediocre financial performance and underperforming expectations.

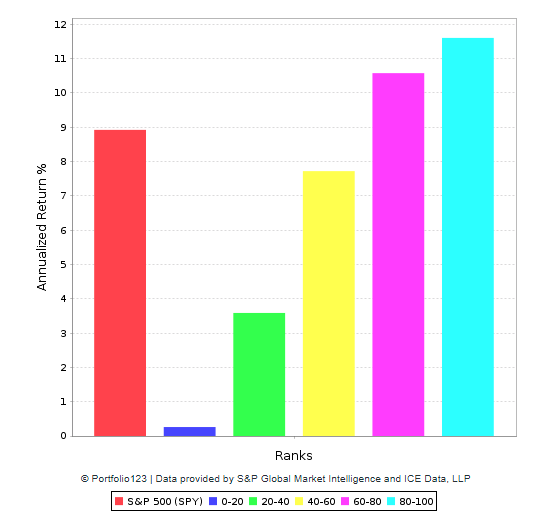

But sometimes it can be challenging to incorporate multiple factors into the analysis in order to see the complete picture from a quantitative perspective. The PowerFactors system is a quantitative system that ranks companies in a particular universe according to a combination of factors, such as financial quality, valuation, fundamental momentum, and relative strength.

Here is a quick explanation of the factors considered in the algorithm:

- Financial quality includes profitability metrics such as return on investment, operating profit margin, and free cash flow margin. The more profitable the business, the higher its ability to create profits for shareholders over the long term.

- Valuation covers typical valuation ratios such as price to earnings, price to earnings growth, and price to free cash flow.

- Fundamental Momentum: This factor looks for companies that are performing better than expected and producing rising expectations, so it measures the change in earnings and sales forecasts.

- Relative Strength: Winners tend to keep on winning. When a stock is outperforming the market, it tends to continue doing so more often than not. For this reason, the PowerFactors system looks for stocks delivering above-average returns over different time frames.

The backtested performance numbers show that companies with high PowerFactors rankings tend to deliver superior returns in the long term. The higher the PowerFactors ranking, the higher the expected returns, indicating that the system is consistent and robust.

Data from S&P Global via Portfolio123

Facebook has a PowerFactors ranking of 98 as of the time of this writing, meaning that the stock is in the top 2% of companies in the US stock market when considering financial quality, valuation, fundamental momentum, and relative strength combined.

Risk And Reward Going Forward

Regulatory risk is one of the most important uncertainty drivers currently weighting on Facebook stock. This factor cannot be overlooked, but it seems like the market could be exaggerating the potential impact of regulatory pressure on the company's business.

Facebook is a top player in social media, but the company is clearly not in a monopolistic position since most social media users actually use multiple social networks from different companies. Users in the social media sector are literally one click away from one platform to the other, and several new platforms have gained ground in recent years.

The company needs to guarantee to both regulators and consumers that it can protect user data and stay away from anti-competitive behavior. This could take some time and money, but Facebook has the financial and human resources to provide such guarantees.

Transitions always carry some risks. Users are increasingly moving away from the traditional Facebook platform towards Instagram, and new features such as stories could be harder to monetize than the newsfeed monetization strategies. In spite of this, management has proven its ability to continue delivering solid results through this transition.

Market risk is an important consideration, Facebook is a high growth stock with above average volatility. Even if the business fundamentals remain solid, the stock is vulnerable to the downside in times of trade war and declining risk appetite among global investors.

Nevertheless, Facebook is a widely profitable business with abundant growth opportunities and trading at attractive valuation levels. For investors who can handle the short-term uncertainty, Facebook looks like a compelling investment over the long term.

Comments

Log in or sign up to join the conversation.