Etsy (ETSY) delivered spectacular numbers for the second quarter of 2020, with the business gaining traction across the board and making significant progress both financially and operationally. The stock is on fire lately, but Etsy still offers plenty of upside potential from current valuation levels.

Etsy Is Firing On All Cylinders

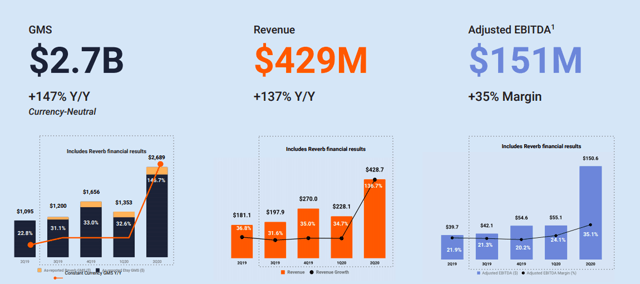

Etsy delivered a year over year increase of 137% in revenue during the second quarter of 2020, to $428.7 million. Marketplace revenue grew 146% and services revenue increased by 110.7%. GMS grew 147% versus the same quarter in the prior year.

(Click on image to enlarge)

Source: Etsy

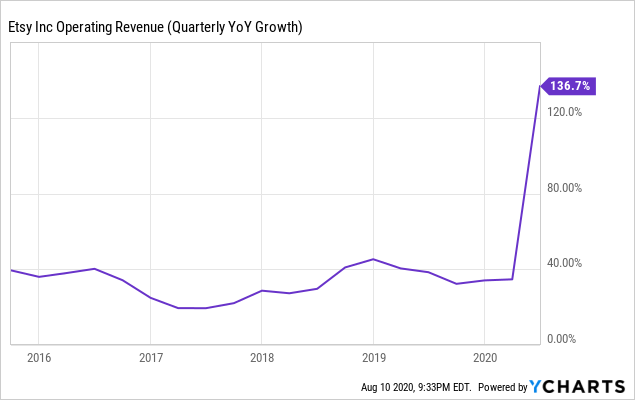

Growth has significantly accelerated lately, but even before the pandemic, the company was producing consistently strong revenue growth rates. Much of the acceleration in growth is obviously temporary, but there are also some permanent drivers to consider.

All the new buyers and sellers, as well as the existing members who get more engaged with the platform during the pandemic are making the company stronger over the long term, even if growth rates can be expected to decelerate when the economy normalizes.

(Click on image to enlarge)

Data by YCharts

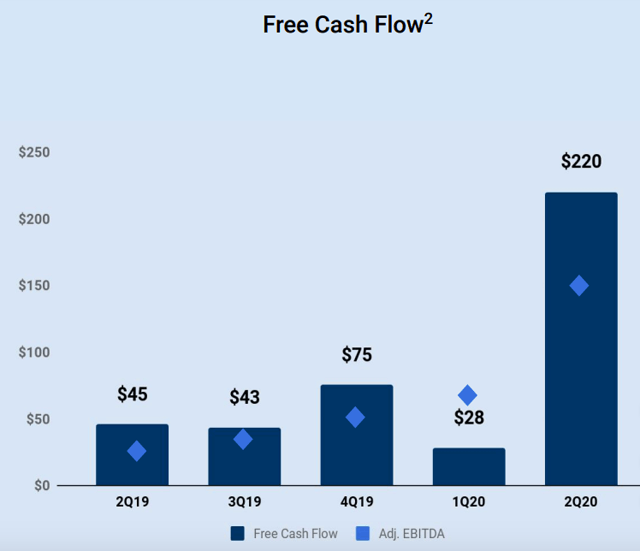

Consolidated active buyers grew 41.0% year-over-year in the second quarter, and active sellers grew 34.6%. Etsy marketplace's GMS per active buyer on a trailing 12-month basis grew 5% year-over-year and 6% excluding masks, so engagement trends are clearly moving in the right direction.

Profitability is also trending higher, gross margin increased from 67.6% in the second quarter of 2019 to 74% of revenue in the second quarter of 2020, and operating expenses as a percentage of revenue declined from 57.8% to 46.2%. Vigorous revenue growth in combination with expanding profitability produced a huge jump in both EBITDA and free cash flow last quarter.

(Click on image to enlarge)

Source: Etsy

Reasonable Valuation

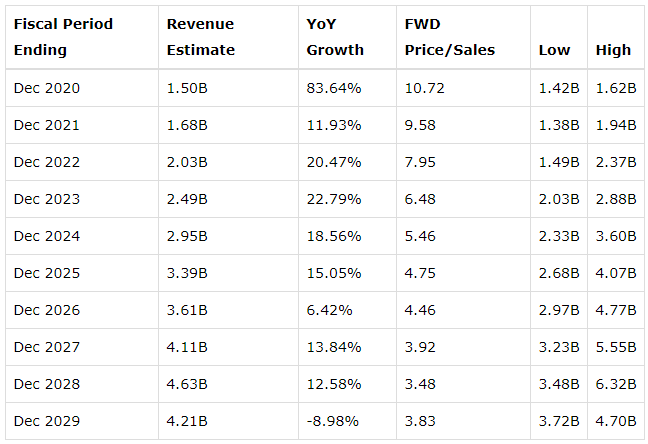

The table below shows the average revenue estimate, the implied revenue growth rate, and the forward price to sales ratio for Etsy in the years ahead. The data also shows the high and low revenue estimates to provide an idea about the degree of dispersion in those estimates.

The gap between the high and low revenue estimates for Etsy is unusually high. This shows that there is a large degree of discrepancy among the analysts following the stock, which can be a source of opportunity if the bullish thesis plays out well.

The high estimate for 2021 stands at $1.94 billion versus an average estimate of $1.68 and a low estimate of $1.38 billion. If revenue numbers ultimately come in closer to the high end of the estimate range, this could be a major tailwind for the stock price. The larger the uncertainty, the bigger the upside when things work out well.

In any case, even assuming that revenue will be in line with the average estimate, a price to sales ratio around 9.6 is hardly excessive for a company that is performing so well and has plenty of room for sustained growth in the years ahead.

(Click on image to enlarge)

Source: Seeking Alpha

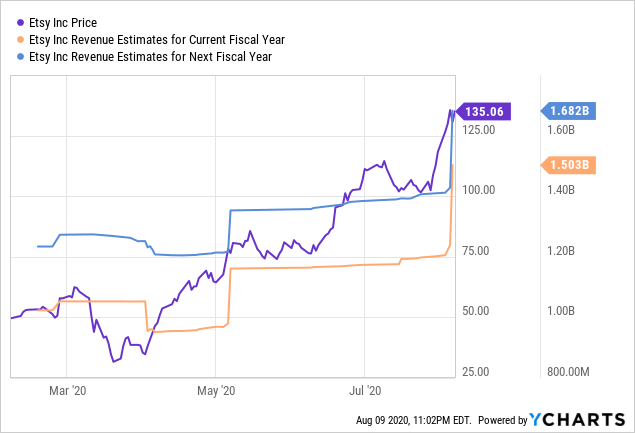

Stock prices reflect a particular set of expectations for the future of a business. When expectations change, the stock price generally moves in the same direction. In other words, if revenue estimates are increasing, the stock price needs to increase too for the price to sales ratio to remain constant.

Wall Street analysts have been running from behind and raising their revenue estimates for Etsy over time, which is pushing the stock price higher too. As long as this trend remains in place, fundamental momentum could be a powerful driver for Etsy stock over the near term.

(Click on image to enlarge)

Data by YCharts

Valuation should be interpreted in its proper context. A company that generates vigorous growth and performs above expectations deserves a higher price to sales ratio than a business with decelerating growth rates and failing to meet expectations.

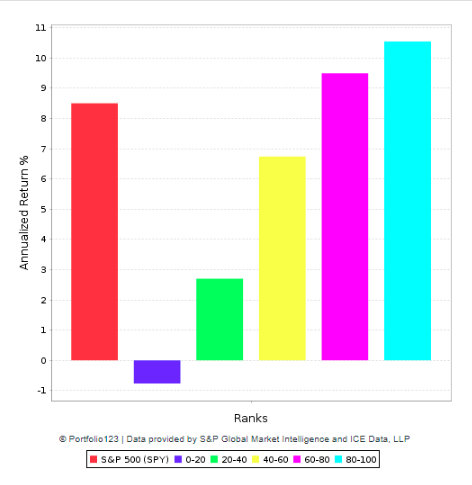

This is beyond discussion, but it can be difficult to incorporate multiple factors into the analysis and quantify them in order to see the complete picture. In that spirit, the PowerFactors system is a quantitative system that ranks companies in a particular universe according to a combination of factors: financial quality, valuation, fundamental momentum, and relative strength.

(Click on image to enlarge)

Data from S&P Global via Portfolio123

The backtested performance numbers show that companies with high PowerFactors rankings tend to deliver superior returns over the long term, and the higher the ranking the higher the subsequent returns.

Etsy has a PowerFactors ranking above 99 as of the time of this writing. This means that the stock is in the top 1% of companies in the US stock markets based on financial quality, valuation, fundamental momentum, and relative strength together.

None of this guarantees future returns. The backtested performance data simply tells us that a large number of companies with high PowerFactors rankings tend to deliver superior returns over the long term, but this does not tell us much about how a specific company such as Etsy will perform in a particular year.

The company certainly needs to continue meeting and ideally exceeding expectations in order to deliver solid returns going forward. However, it is good to know that Etsy stock is still offering attractive upside potential from current valuations if management keeps executing well.

Risk And Reward Going Forward

Competition is always a concern for investors, especially when it comes to a company operating in such a dynamic environment. However, Etsy has proven to be quite solid from a competitive perspective. In 2015 Amazon (AMZN) launched its Handmade at Amazon site, and it did not derail Etsy from its growth trajectory.

Most buyers and sellers on Etsy would hardly consider moving to such an enormous and "industrialized" platform as Amazon. Besides, the network effect is one of the strongest sources of competitive strength for online businesses, and Etsy is a textbook example of how this factor plays out.

Buyers and sellers attract each other to a platform such as Etsy in search of more opportunities to buy and sell different kinds of products. The bigger the platform the more value it provides to its users, which keeps attracting more users and creating a virtuous cycle over time. Winners tend to keep on winning in this market, and Etsy has already gained escape velocity.

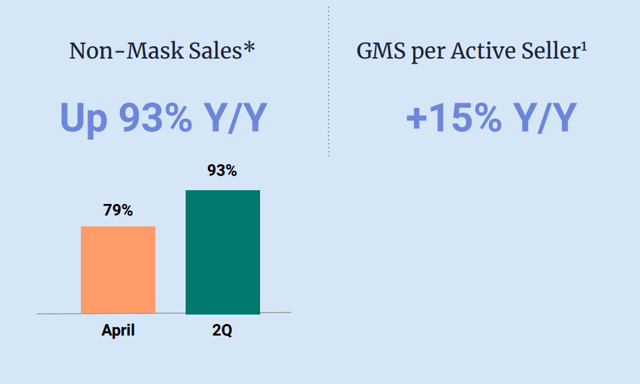

Another potential reason for concern is that a large share of revenue growth in recent months could be due to exceptional circumstances during the pandemic. The e-commerce industry as a whole is being benefited by the stay at home measures, and Etsy has benefited from a huge increase in masks sales recently.

The statistics for mask sales are truly mind-blowing. In the second quarter, Etsy sold $346 million worth of masks, and over 110,000 sellers sold at least one mask. To provide an idea, that's enough masks to stretch all the way from New York to London according to management.

But performance without masks has been outstanding too. Non-mask sales grew 93% in the second quarter, accelerating versus a 79% increase in April. Besides, masks are bringing buyers and sellers to Etsy, and chances are that these users will remain on the platform when the pandemic is over to a good degree.

(Click on image to enlarge)

Source. Etsy

Etsy is not a "buy and forget" company, it will be important to monitor the company's fundamentals and strategic direction in the years ahead. But the upside potential is clearly attractive.

Etsy is a relatively young company with an attractive business model in a high growth industry, and financial performance has been outstanding recently. For these reasons, the stock looks well-positioned for attractive returns in the years ahead.

Comments

Log in or sign up to join the conversation.