Children and stocks are similar. You’re not supposed to have favorites.

But we all know that we do.

(I’m talking about stocks, of course – not the other thing.)

For years, I’ve said that despite my advice that you shouldn’t grow attached to individual stocks, Enterprise Products Partners (EPD) is one of my favorites.

It’s been in my Oxford Income Letter‘s portfolio for more than six years. Investors who bought it when I first recommended it have quadrupled their money.

Even better, though the stock has a yield of about 6% now, investors who bought back then are earning a whopping 14.7% yield on their original investment thanks to strong growth in the quarterly payout.

Can investors expect continued higher payouts?

Enterprise Products Partners is a master limited partnership, or MLP, that owns oil and gas pipelines.

It’s a pretty simple business. Other than maintaining the pipelines, there’s not a lot of capital, equipment, or staff required.

As a partnership, the company does not pay dividends. It pays distributions, which are taxed differently than regular dividends.

Dividends are taxed at the long-term capital gains rate, which is 15% for most people and as high as 23.8% if you’re in the highest tax bracket.

Distributions are typically considered a “return of capital.” As a result, they are not taxed in the year they are received. Instead, your cost basis is reduced by the amount of the distribution. Then, when you sell the stock, your capital gain – and the tax you pay on it – will be larger.

Here’s what I mean. If you buy a stock at $20 and receive a $1 distribution that is all return of capital, your new cost basis is $19.

If you sell the stock at $22, you’ll pay taxes on $3 worth of capital gains rather than $2.

However, the benefit is that you can collect tax-deferred income for years.

If you held the stock for 10 years and earned a $1 distribution per share each year, that would be 10 years’ worth of income that you did not pay taxes on.

Enterprise Products Partners’ distributable cash flow, or DCF, in 2025 was $8 billion, a 2.1% increase from the previous year. It paid out $4.7 billion in distributions for a payout ratio of 59%.

That’s a nice, low payout ratio. For an MLP, I’m fine with anything below 100% since MLPs exist for the purpose of distributing cash back to partners. They are not “earnings stories” like regular companies.

This year, DCF is forecast to inch higher to $8.04 billion. Distributions are also expected to increase to $4.8 billion, which would come out to a payout ratio of 60%.

If the company’s DCF slips instead of growing, that could result in a downgrade, but for now, it looks good.

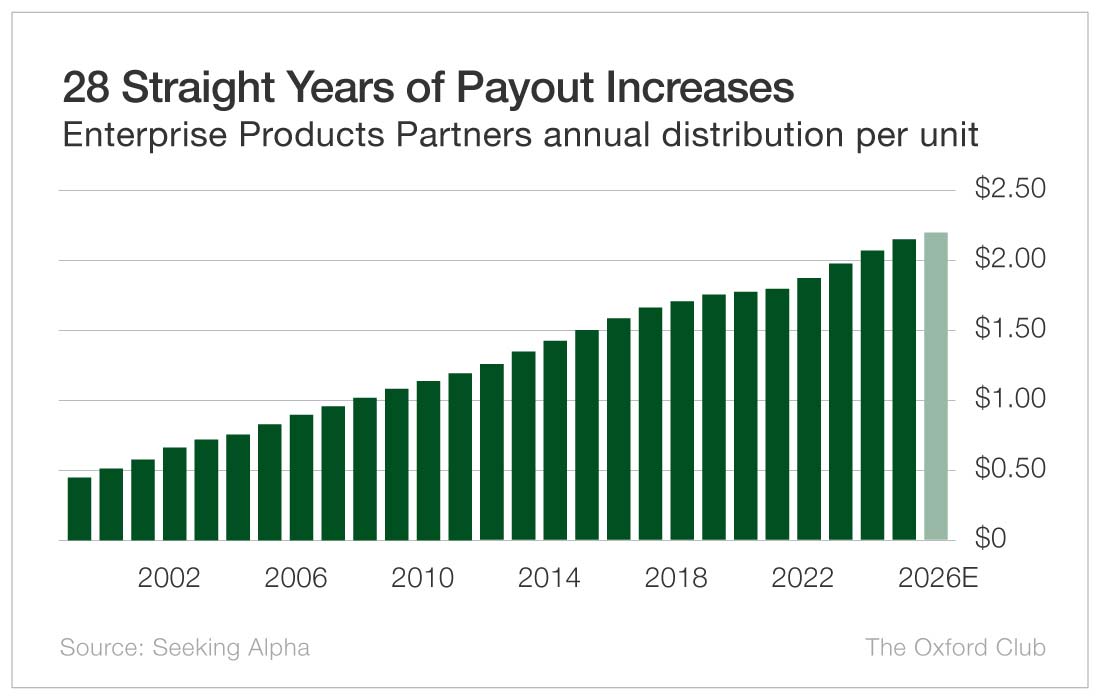

Lastly, Enterprise Products Partners is a Perpetual Dividend Raiser. It has boosted its distribution every year since 1999.

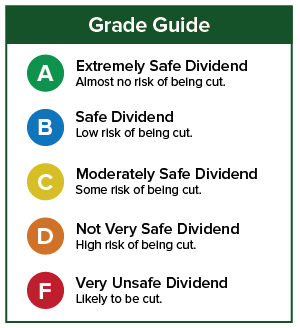

Given its growing cash flow, comfortable payout ratio, and 28-year history of annual distribution increases, it’s no surprise that my “favorite” stock has a very low risk of its payout being cut.

Dividend Safety Rating: A

Comments

Log in or sign up to join the conversation.