Yes, the man is totally deranged, and so is the entire eurozone policy apparatus. Like much of officialdom elsewhere in the world, the ECB is attempting to fight low growth and low inflation with monetary nitroglycerin. It's only a matter of time before they blow the whole financial works sky high.

Low real GDP growth in the eurozone has absolutely nothing to do with the difference between –0.3% on the ECB deposit rate versus the new -0.4% dictate announced this morning; nor does QE bond purchases of EUR 80 billion per month compared to the prior EUR 60 billion rate have anything to do with it, either. The only purpose of such heavy handed financial intrusion is to make borrowing cheaper for households and businesses.

But here’s what the moronic Mario doesn’t get. The European private sector don’t want no more stinkin’ debt; they are up to their eyeballs in it already, and have been for the better part of a decade.

The growth problem in Europe is due to too much socialist welfare and too much statist taxation and regulation, not too little private borrowing. These are issues for fiscal policy and elected politicians, not central bank apparatchiks.

As shown in the chart below, the eurozone private sector had its final borrowing binge during the initial decade of the single currency regime through 2008; debts outstanding grew at the unsustainable rate of 7.5% annually. But since then the eurozone private sector has self-evidently been stranded on the shoals of Peak Debt.

Outstandings have flat-lined for the past eight years—-not withstanding increasingly heavy doses of ECB interest rate repression that have finally taken money market rates into the netherworld of subzero.

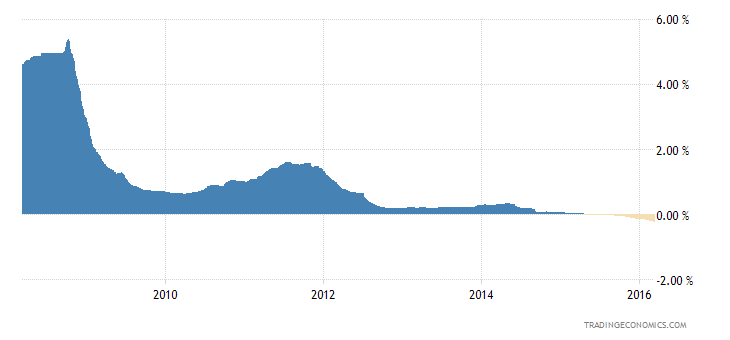

Nor has the approximate EUR $700 billion of bond purchases since QE’s inception last March made one wit of difference. Bank loans outstanding to the private sector were EUR 10.24 trillion at the end of January or exactly where they stood in March 2015 when Draghi and his merry band of money printers went all in.

By the same token, it is damn obvious that low inflation is not a problem, and that, in any event, it is not caused by lack of money printing and insufficient interest rate repression by the goofballs assembled at the ECB’s swell new headquarters in Frankfurt. The eurozone’s respite from its normal 1-2% annual dose of headline inflation is entirely imported via the global tide of plunging oil, commodities, steel and other industrial prices.

That welcome tide of imported deflation, in turn, is actually improving the eurozone’s terms of trade and raising consumer living standards; and it is not remotely connected to anything the ECB has done or not done in the last year or even four years.

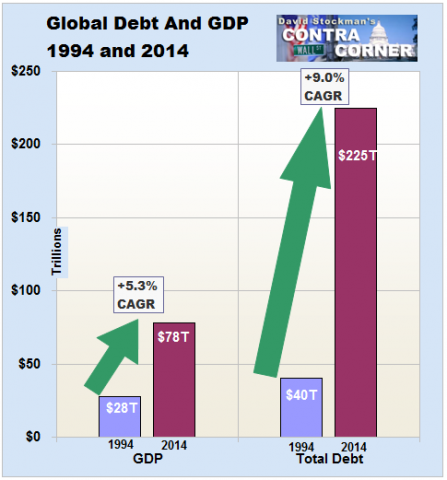

Instead, the global deflation is a consequence of the massive malinvestment in mining, energy, industry, transportation and distribution which has resulted from the 20-year global credit binge enabled by the world’s convoy of money printing central banks. Incremental debt of $185 trillion or nearly 4X GDP growth during that period has crushed the world’s capacity for investment and production led growth.

The overhang of excess capacity everywhere on the planet is also drastically compressing prices, margins and profits, but the major impact is in the Red Ponzi and its EM supply chain; and the secondary impact is on engineered machinery, high tech and luxury goods exporters, including Germany and other eurozone export strongholds.

It goes without saying, however, that today’s new round of monetary quackery by the ECB will have no impact whatsoever on eurozone export demand from China and the EM. Not only did Draghi fail to send the Euro careening lower, but it wouldn’t matter anyway. The barrier is not FX; the problem is investment saturation in foreign markets that have run out ofborrowing capacity.

In any event, the global deflation is actually a boon to eurozone workers and consumers because Europe is a giant energy and materials importer.

So what if that windfall to living standards in the old age colony now planted on the european continent causes the headline inflation indices to temporarily flat line?

Do the Keynesian madmen at the ECB really think that the hundred million or so eurozone households living essentially hand-to-mouth on stagnant wages and welfare will actually stop buying food, clothing, shelter, shoes, movie tickets, bedroom furniture and backyard garden tools because they are waiting for prices to go down?

In a world of peak debt and stagnant wages, the idea of a deflationary buyers strike is just self-serving bureaucratic jabberwocky.

The truth is, the whole central bank anti-deflation gambit is based on an egregious and self-created strawman. Namely, the utterly bogus notion that 2.00% headline CPI inflation is the magic elixir of economic performance. Yet there is not a shred of evidence to support it; it has come to prevail as a policy norm purely as a matter of assertion and ritual incantation.

In fact, the whole central bank inflation targeting regime has degenerated into the monetary equivalent of counting angels on the head of a pin in the manner of medieval theologians. If you even set aside just oil and energy——which absolutely is not produced within the borders of the eurozone——you get the picture shown below.

To wit, since the inception of the single currency in 1999, the harmonized consumer price index less energy (and seasonal food) has advanced at a1.57% rate per annum. During eight the years since the great financial crisis in 2008 it has gained by 1.21% per annum; and, assisted by the declining price of Europe’sraw materials and other non-energy imports, the index rose by 1.01% during the year ending in January.

So c’mon. Is there one iota of economic logic or common sense which suggests that a mere 36 basis point, or 56 basis point deviation, respectively, from a deeply embedded 17-year trend is enough to cause the $13 trillion eurozone economy to sink into some kind of macroeconic black hole? And one so devastating that it can only be remedied by what is essentially a criminal assault on savers and a windfall to speculators?

So, it can be well and truly said that the ECB and other central bankers are so far down the rabbit hole that they have lost contact with common sense.

Comments

Log in or sign up to join the conversation.