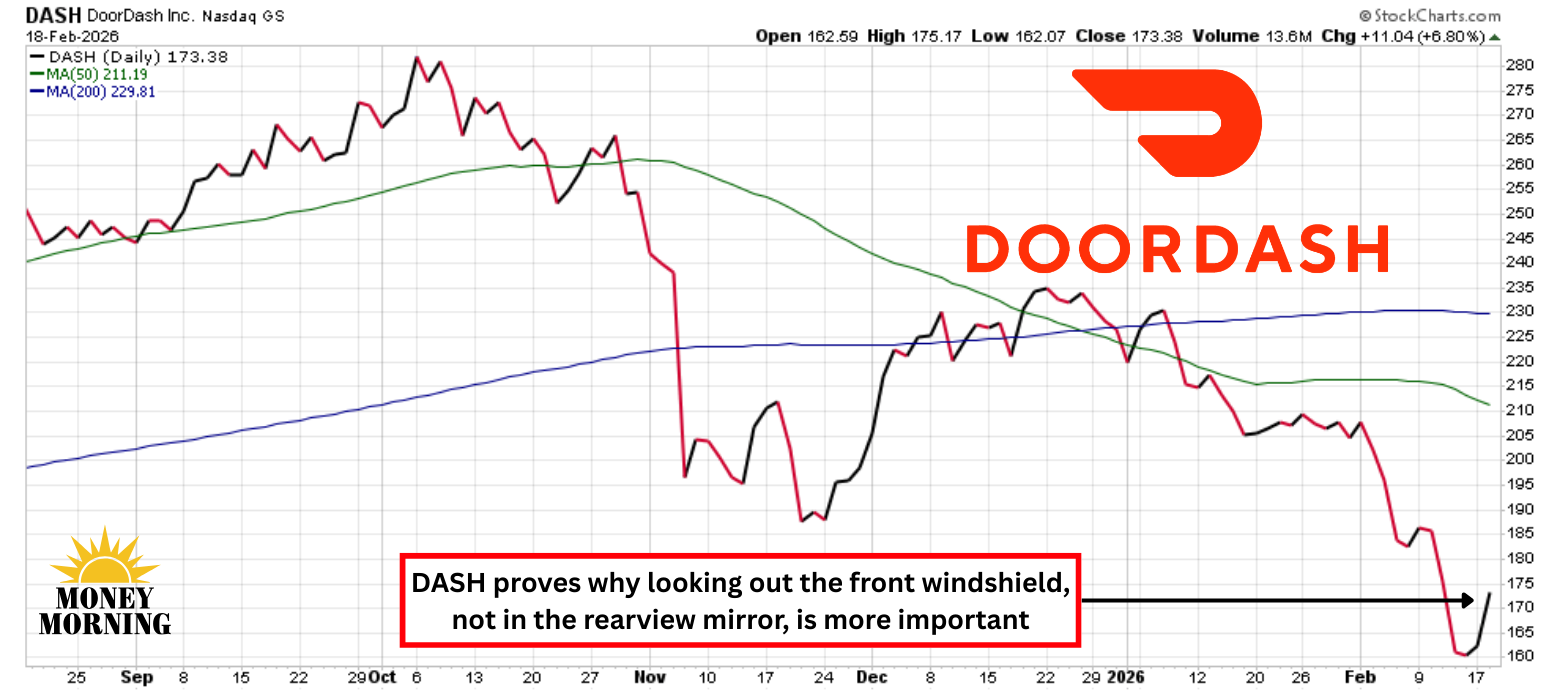

It's not very uncommon for a company to miss both revenue and earnings estimates yet see its shares surge afterward. DoorDash (Nasdaq: DASH), though, achieved just that following its fourth-quarter 2025 results. The food delivery giant reported revenue of $3.96 billion, falling short of the $3.99 billion Wall Street expected, while adjusted earnings came in at $0.48 against forecasts of $0.59 per share.

Despite the misses, the stock – which initially plunged on the headline numbers – reversed course and rallied higher as investors digested the bigger picture. This reaction underscores a key investing principle: a company's future trajectory often matters more than its current snapshot. DoorDash's emphasis on long-term growth, international expansion, and operational efficiencies convinced the market that brighter days lie ahead.

Misses Mask Underlying Strength

DoorDash's Q4 performance showed robust year-over-year growth, but it couldn't quite meet lofty analyst expectations. Total orders jumped 32% to 903 million, and Marketplace Gross Order Value (GOV) rose 39% to $29.7 billion. Revenue grew 38% to approximately $4 billion, yet this slight shortfall – coupled with the EPS miss – triggered an immediate sell-off in extended trading.

However, full-year 2025 revenue reached $13.7 billion, with GAAP net income soaring to $935 million, demonstrating a shift toward consistent profitability. Adjusted EBITDA also increased 38% to $780 million, reflecting solid profitability gains amid scale. The initial market jitters gave way as details emerged, revealing a company not just surviving but strategically advancing.

Dashing Forward With Momentum

What turned the tide for investors was DoorDash's optimistic outlook and key operational wins. Management guided for a slightly higher full-year 2026 adjusted EBITDA margin as a percentage of Marketplace GOV compared to 2025, excluding the recent Deliveroo acquisition, even as the company ramps up investments in technology and autonomous delivery.

Deliveroo – acquired last October – outperformed expectations with over $45 million in Q4 EBITDA contribution, and is projected to add about $200 million in 2026. Wolt, DoorDash's earlier international acquisition, continues to integrate smoothly, bolstering global operations. International segments (excluding Deliveroo) saw accelerating GOV growth and improving unit economics quarter-over-quarter, outpacing U.S. expansion.

New verticals like grocery and retail also attracted record new consumers, with U.S. Marketplace GOV in these areas holding steady and unit economics on track to turn gross-profit positive in the second half of 2026. DashPass had a banner year, adding record subscribers to reach over 35 million members across programs, driving higher order frequency and profit dollars,though it compresses margins in the short term.

These elements paint a picture of sustained momentum, with DoorDash leveraging a unified global tech platform for efficiency and innovation.

Bottom Line

DoorDash's business is clearly gaining traction, with strong order growth, international acceleration, and profitability improvements signaling a maturing model. However, the stock trades at lofty valuations, currently around 81x trailing earnings and 36x estimates, although Wall Street anticipates a robust 49% EPS compound annual growth rate over the next five years, fueled by scale and new verticals.

Still, prudent investors might want to wait for a pullback in the stock before jumping in, as the premium pricing leaves little room for error.

Comments

Log in or sign up to join the conversation.