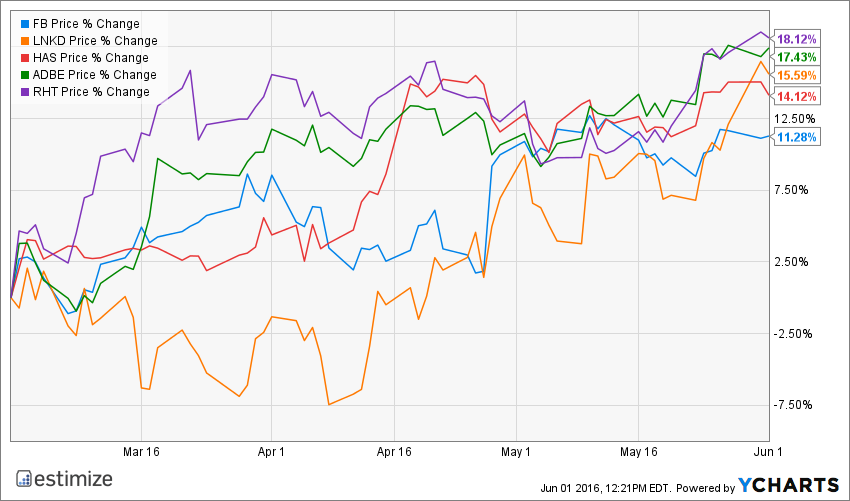

With over 90% of companies having reported earnings for Q1, this quarter can largely be deemed a disappointment. Despite a number of companies beating on both the top and bottom line, earnings growth from a year earlier still came in negative. This marked the first time the S&P 500 recorded four consecutive quarters of year over year declines in earnings since 2009. However, it hasn’t been so bad for everyone and ahead of Q2 earnings a number of companies are poised to impress investors. They include, Facebook (FB), LinkedIn (LNKD), Hasbro (HAS), Adobe (ADBE), and Red Hat (RHT). According to the Estimize data these names have been on the move, signified by consistent year over year growth, heavy upward revisions, and a history of beating expectations. The combination of these factors have typically led to substantial out performances and a pop in share prices.

Facebook (FB) Information Technology – Internet Software & Services

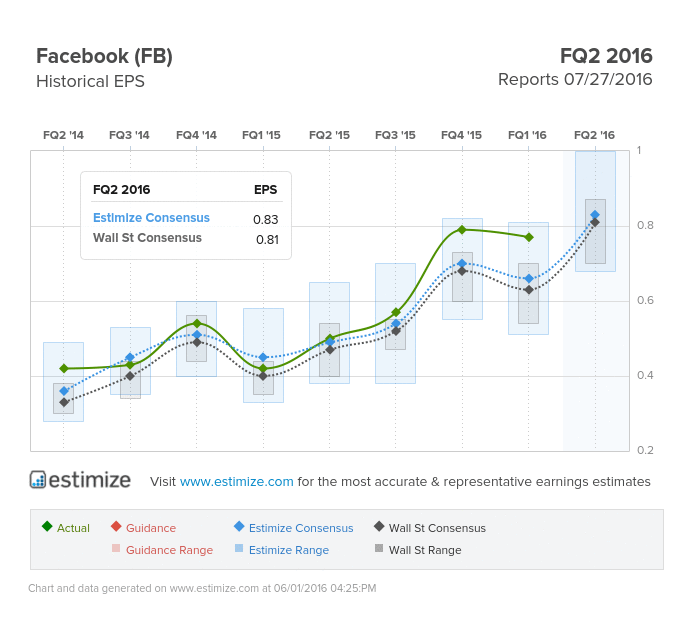

Lately, there are only a few names that can do no wrong in the eyes of Wall Street, and Facebook is one of them. The social media giant unsurprisingly bested its first quarter earnings with a user base that hasn’t stopped growing. The quarter featured double digit gains in monthly and active users with ad revenue growth skyrocketing over 50%. Active users should sustain their current growth levels but Facebook is more than just a social media company at this point. The company’s acquisitions of WhatsApp, Instagram and Oculus Rift have already exhibited robust growth. With Oculus prepared to hit the market in the next few months, Facebook have a new source of revenue.

Estimize is high on Facebook to maintain its success into the second quarter. The consensus data is looking for earnings per share of 83 cents on $6.01 billion in revenue, 2 cents higher than Wall Street on the bottom line and $20 million on the top. Compared to a year earlier this reflects a 64% increase in profitability and 49% revenue growth. In the last month, per share estimates have increased 16% and should continue to rise as we near its report date. For shareholders, strong earnings have contributed to the 50% gains in the stock.

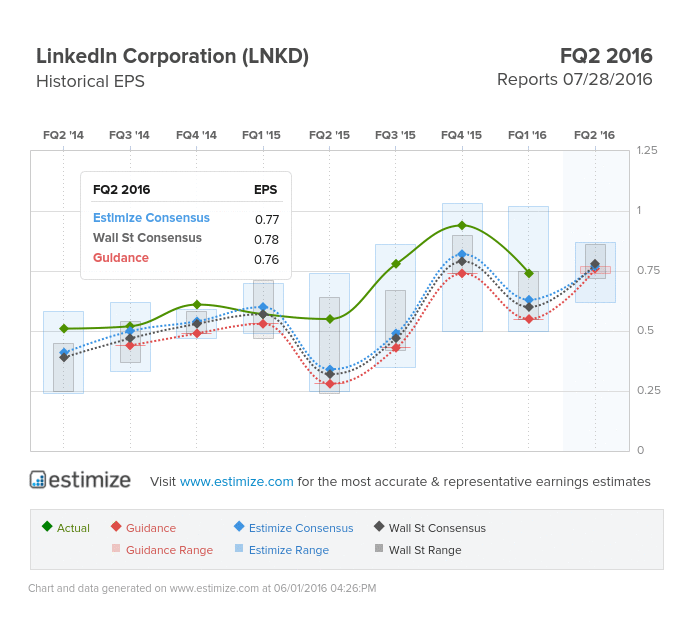

LinkedIn (LNKD) Information Technology – Internet Software & Services

Staying in the social media space, LinkedIn is another name bringing positive momentum into Q2 earnings season. The professional network kicked off fiscal 2016 and rebounded impressively from its Q4 analyst call that cut the stock in half. Earnings have never been the issue for LinkedIn, rather it’s forward looking guidance that tends to influence the stock. However, this quarter the company eliminated those concerns with both robust earnings and raised guidance. LinkedIn continues to see double digit gains in revenue from premium subscriptions, and talent and marketing solutions. After a good start, management indicated that Q2 revenue would come in between $885 and $890 million. The Estimize consensus is more bullish, forecasting revenue of $895.47 million on 77 cents per share. Compared to a year earlier this represents a 41% increase on the bottom line and 26% on the top. Earnings estimates have been revised up 15% in the last 3 months and should continue to into the report in July.

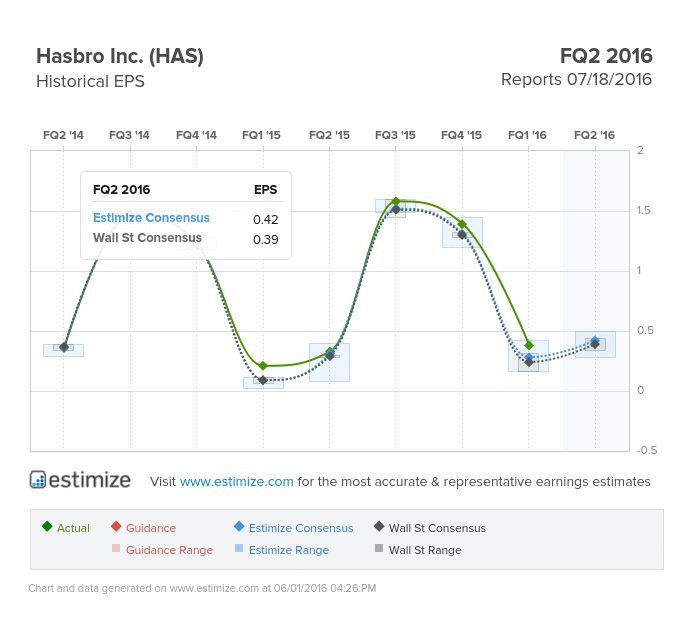

Hasbro (HAS) Consumer Discretionary– Leisure Equipment & Products

Star Wars: The Force Awakens has come and gone but Hasbro continues to benefit from its success. The toy maker yet again reported better than expected earnings thanks to its deep pipeline of movie based products. While Star Wars related toys should start to wane this should be more than offset by Captain America toys and the highly anticipated Disney princess line. With the second Frozen movie scheduled to hit theatres later this year, Hasbro girl’s sector should start to carry its own weight. This quarter, the Estimize community is looking for earnings of 42 cents per share on $881.90 million in revenue, 3 cents higher than Wall Street on the bottom and $4 million on the top. Compared to a year prior, profits are projected to rise 21% with a 10% increase in revenue. In the last month alone, earnings have been revised up 6%, reflecting analyst positive sentiment towards the toymaker.

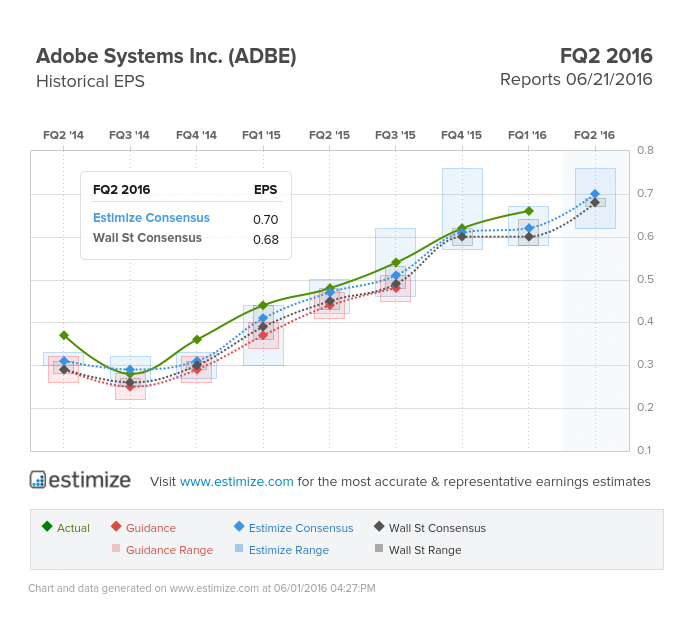

Adobe Systems (ADBE) Information Technology – Software

In the past 2 years, Adobe has seen both earnings and revenue steadily increase. In 2014, Adobe was plagued with low single digit growth, yet last quarter earnings growth topped 50% with revenue exceeding 20%. The new age of cloud computing has been key to Adobe’s success. Currently its two biggest drivers Creative Cloud and Marketing Cloud products continue to see record adoption rates. Early indications look as if increasing booking growth will bring strong Q2 earnings. The Estimize consensus is looking for earnings of 70 cents per share on $1.4 billion in revenue, 2 cents higher than Wall Street on the bottom and $10 million on the top. This reflects a 44% increase in EPS from a year earlier with revenue expected to grow 21%. Estimates should continue to rise in the run up to its report and are already up nearly 10% in the last 3 months.

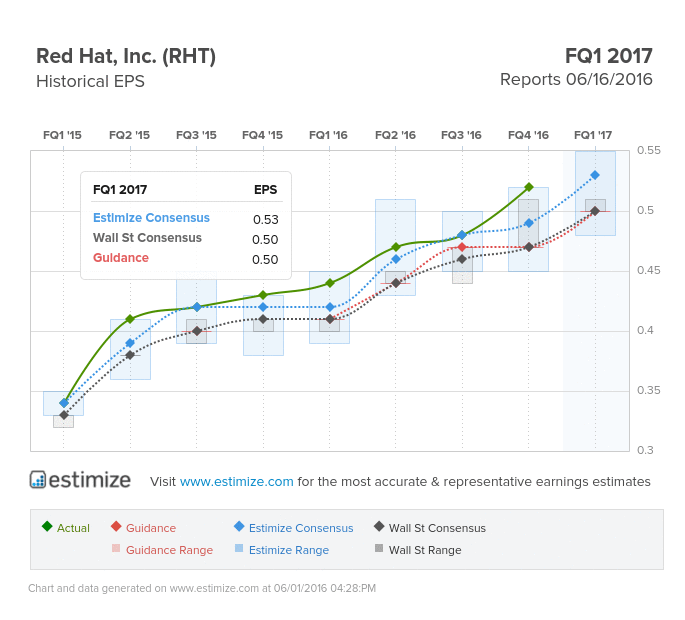

Red Hat Inc. (RHT) Information Technology – Software

Cloud computing is without a doubt one of the hottest industries at the moment, with companies like Amazon, Microsoft and Google all taking part in the action. And while the space is heavily concentrated at the top, smaller names have also been successful at stealing market share, Red Hat being one of them. Red Hat has been on the rise the past 2 years, seeing double digit gains in both earnings and revenue. While Red Hat Enterprise Linux remains a mainstay for the company, its beginning to shift towards new growth areas. Last week its continued those efforts with the release of Red Hat Open Stack and Cloud Suite platforms. The fully open solutions for enterprises allows IT organizations to manage and control their infrastructure from 1 place. For these reasons the Estimize community is bullish that Red Hat will beat once again. The consensus data is calling for earnings per share of 53 cents on $568.12 million, higher than both Wall Street and corporate guidance issued in March. From a year earlier, earnings and revenue are projected to grow 17%. However, given Red Hat’s track record and upward revisions activity, it won’t be surprising if growth rates trump 20% at the time of its report.

Comments

Log in or sign up to join the conversation.