Introduction

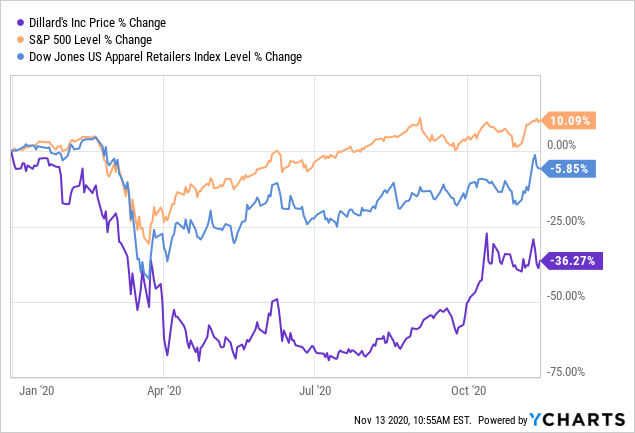

In our previous reports, we have explained the concerns around the retail sector as a whole, as evident with the general economic recovery sluggishness along with a flurry of retail bankruptcies. Dillard's (DDS) continue to be an underperformer for the year declining 36% YTD compared to US Apparel Retailer's index down 5^ and S&P's 10% uptick. The departmental stores continue to face competition from e-commerce and off-price retailers with renewed worries due to the second wave of COVID-19 that could potentially derail the recovery of the sector. That being said, the earnings season is upon us and we would have further data to validate the retail recovery, particularly the stronger ones like Dillard's poised to weather the COVID-storm and the company did manage to beat expectations handsomely.

Data by YCharts

Earnings Corner

The company reported sales of $1,025mn, a decline of 25% compared to the previous year, which fell slightly short of the expectations as the stores opened up fully during the quarter. Sales in comparable stores for the same period decreased approximately 24%. The home and Furniture segment continued to be the outperformers followed by ladies' accessories and lingerie and cosmetics while ladies' apparel remained a laggard. The biggest beat was in the gross margins which eclipsed even the year-ago period where the company reported 33.2% gross margin and posted a 35.7% gross margin, ahead of most estimates. The gross margin beat was primarily due to the decreased markdowns, which is encouraging as the company is able to sell through a sizeable chunk of its inventory without pushing down the prices highlighting the buoyancy of the recovery in retail and consumer confidence. Along with higher gross margins, cost control measures helped the company to post a surprise profit for the quarter excluding tax adjustments compared with our expectations of a minor loss. Inventory again declined 22% for the quarter which would aid the margins for the crucial holiday season quarter.

Summary

The stock got a huge boost last month when it was disclosed that Berkshire's Ted Weschler reported a 5%+ holding in the company, post which the stock skyrocketed almost 45%. However, although there are several positives, there are still structural challenges that remain unanswered with regards to its aging customer base and portfolio attractiveness. While the COVID-19 vaccine news was largely positive, the massive logistical hurdles remain still in place for delivery, refrigeration, and distribution on a large scale. With rising hospitalizations as we are in a crucial holiday season phase which contributes the highest proportion of revenue and EBITDA to the total year, soft footfall traffic could possibly derail the recovery path for the retailers. We remain cautious on Dillard's and highlight that most of the positives are already priced in and a hit during the crucial holiday season could prove much more challenging to the company. Reiterate Neutral.

Comments

Log in or sign up to join the conversation.