(Photo Credit: Mike Mozart)

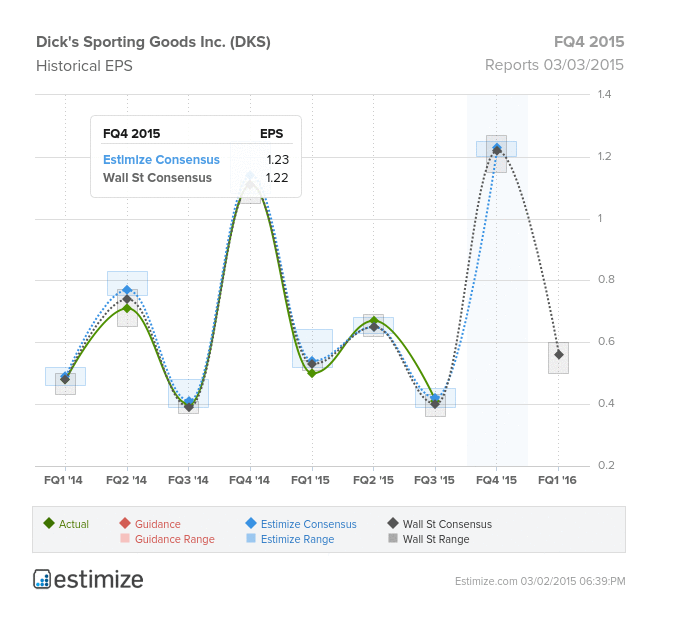

Before tomorrow’s markets open, Dick’s Sporting Goods will report results for the fourth quarter. The Estimize community is calling for EPS of $1.23, a penny higher than the Wall Street consensus, suggesting YoY growth of 11%. Revenues estimates of $2.1B are in-line with Wall Street, expected to grow 9% from the year-ago quarter.

The weaknesses and bright spots in Dick’s business segments are well known. It’s no secret that the company has struggled with their hunting and golfing businesses in the last several quarters. Dick’s owns Field & Stream stores which have felt the pain of lower firearm and ammunition sales in 2014. During 2012 - 2013 changing political winds encouraged a rush to purchase guns which has since died down, a pain point for competitors like Cabela’s as well. Similarly, sales at Golf Galaxy, Dick’s golf apparel and equipment store, have been hurting the overall business. Since the recession, many have turned away from the expensive sport, or cut down on how often they play. Golf is also having a hard time attracting a new generation of players. In Q3, Dick’s reported same store sales of 1.7%, but that figure jumped to 4.6% ex-golf and hunting. We’re expecting similar commentary this quarter.

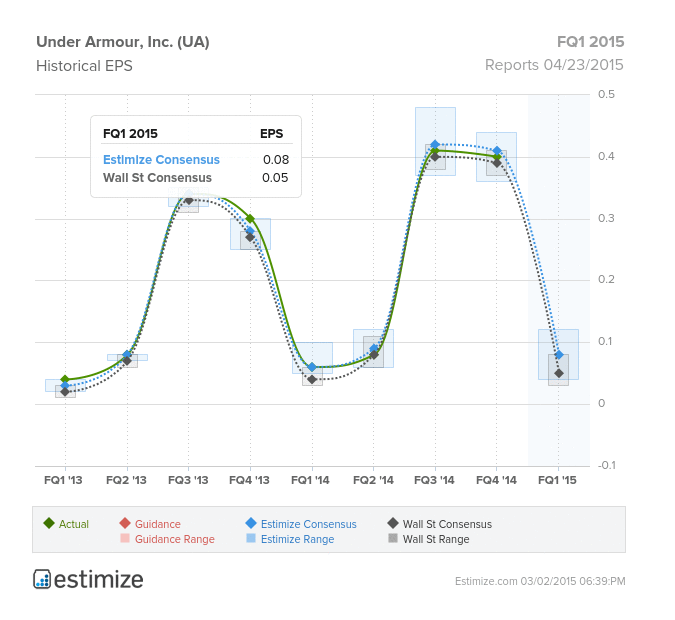

The bright spot for Q4 will most certainly be athletic apparel, specifically for women and youth. This is an area that has been consistently growing for Dick’s. Under Armour is one of the most important brands that the sporting goods retailer carries, and that company performed phenomenally in Q4, growing earnings and revenues by over 30%. They’ve made a conscious effort to carve out a space for Under Armour in their stores, by launching shop-in-shop facilities, and that is expected to pay off this quarter.

Comments

Log in or sign up to join the conversation.