Photo Credit: Mike Mozart

Dave & Buster’s Entertainment (PLAY) Consumer Discretionary - Hotels, Restaurants & Leisure | Reports June 7, After Market Closes

Dave & Buster’s is scheduled to report first quarter earnings tomorrow after the market closes. The company operates in a niche retail-restaurant market with an arcade in a bar & grill style setting. Dave & Buster’s is expected to deliver a 7th consecutive report of better than expected earnings and revenue. The company IPO’d in late 2014 and since then has exceeded expectations in every quarter. As a result the stock has increased 137.1% and is likely to jump on tomorrow’s report.

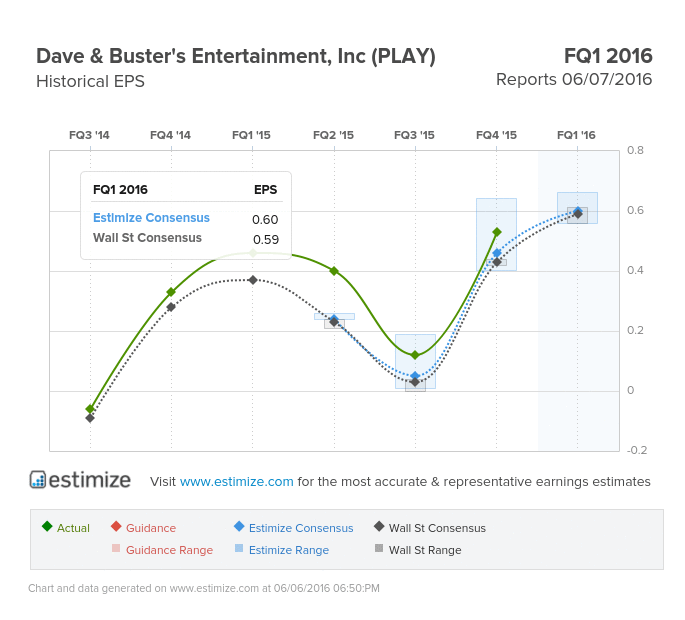

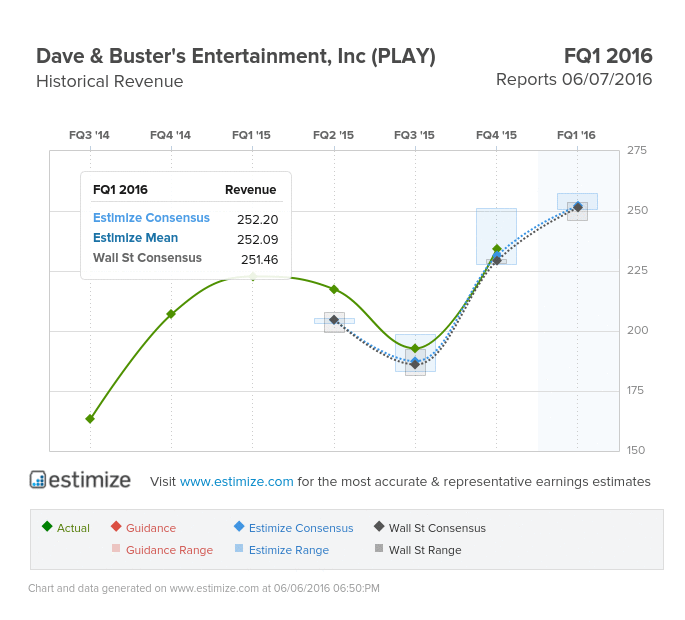

The Estimize consensus is calling for earnings per share of 60 cents on $252.20 million in revenue, 1 cent higher than Wall Street on the bottom line and right in line on the top. Compared to a year earlier earnings are projected to increase 30% on 13% sales growth. Not that investors needed another reason to buy in, but the stock typically posts big gains during earnings season. On average, shares increase 4% through earnings, rising to 7% in the month following a report.

Dave & Buster’s has been one of the few recent IPO’s whose rapid growth has translated to market gains. The full year 2015 featured a 16% increase in revenue coupled with 9% gains in comparable store sales. Driving growth was 10 new stores in the United States. In 2016 the company intends to open 9 to 10 new stores spanning from small to large store formats. The financial outlook for fiscal 2016 appears in line with its current growth rates. Total revenues are expected in the range of $967 to $987 million with comparable stores increasing in the range of 2-4%.

Not too many bad things can be said about Dave & Buster’s at the moment. With a rapid expansion plan in place, the company could see increasing operating expenses and pressure on margins. Meanwhile, the weaker spending environment might deter consumers from frequenting Dave & Buster’s stores. That said, all indications point to a strong first quarter.

Comments

Log in or sign up to join the conversation.