It’s all about data. The decentralized web is underway – or so we would like to believe Sir Tim Berners-Lee as he sets forth on his new adventure Solid as he builds a new open-source platform that aims to let users take control of their data. He gets serious as he takes a sabbatical from MIT for Solid. This announcement last week was fortuitous as it coincided with the sordid details of Facebook’s hacking. There were three bugs identified that allowed access to tokens in Facebook and then to other accounts. They reset access to nearly 50 million users and then another 40 million as a precaution. This is what Forbes called an Internet catastrophe: What’s most worrying of all, though, is what the hack has proven: that a company with the resources and power of Facebook can be robbed of keys that allow access to millions of accounts across the web. Given the keys allowed the hacker to take over any account using a Facebook login, the real number of affected individuals is likely far higher than 50 million. A vast number of people have trusted Facebook would be able to keep their login information safe, just as they do with Google and other tech providers.

What does this all have to do with digital assets or crypto currencies or the blockchain? Plenty. This last week’s data focus goes back to the basics principles of a distributed ledger – decentralization – and its ability to help ferret out fraud and hacks. If everyone has a copy, changing the original isn’t enough. There is also the constant tug and pull of regulations as many want more than DLT to stop hacking and malfeasance. The principles clash, anarchists of the web battle with the centrists for credibility and control.

What Happened Last Week?

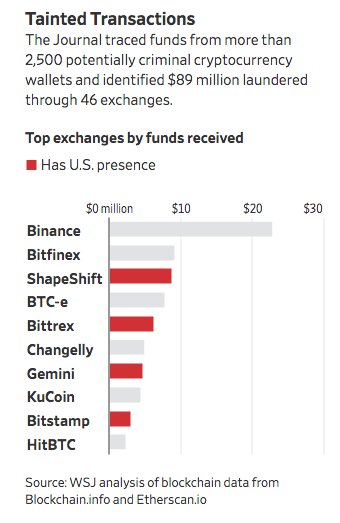

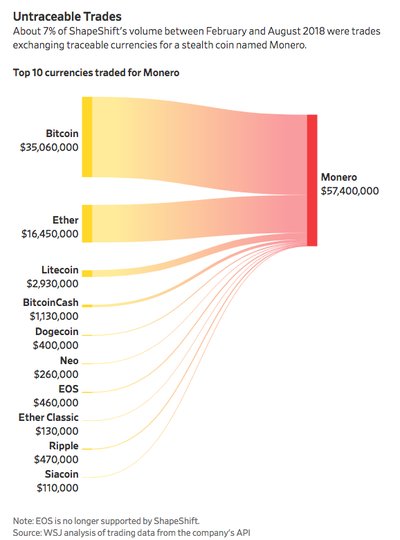

The WSJ investigation into dirty money highlights risks to crypto exchanges. The WSJ report highlighted the ShapeShift AG online exchange particularly but the investigation included 46 exchanges. It also linked money laundering with the Monero coin and highlighted its links to North Korea and washing the Wanna Cry ransom.

The article raises a number of questions – 1) are crypto currency exchanges misnamed? They act as custodian, platform, proprietary trader and clearer. This matters as the battle over regulation and restricting blockchain activities rests on such definition. ShapeShift argues its not in custody of customer funds so it’s not subject to KYC or AML rules. The U.S. Department of Treasury appears to disagree. Asked at a recent event about ShapeShift, Kevin O’Connor, an enforcement officer at Treasury’s Financial Crimes Enforcement Network, said that any crypto-to-crypto exchange that has U.S. customers must comply with rules governing money transmitters. A FinCEN spokesman said Mr. O’Connor was speaking broadly and not just in relation to ShapeShift. 2) are certain coins more prone to money laundering? The feeder stream of other coins into Monero as listed by the WSJ report are consistent with the overall market capitalization and so don’t have much meaning in the debate. This means it’s not a unique to crypto problem but rather just a tool for such behavior. 3) Are exchanges about to get regulated more aggressively? After the New York Attorney General Report and this WSJ report, the press would have you believe that all exchanges are looking for legal loopholes. A survey from Mistertango reported that 88% of exchanges want some industry regulation. About 40% of crypto exchanges in the study think “reducing barriers to funding crypto activity by banks will improve acceptance.” This is one of the factors driving adoption in South Korea, known as one of the largest markets for crypto currency trading.

Themes:

- Can crypto markets self-regulate? The biggest block to larger acceptance of digital assets for institutional money is the lack of clear regulation. The ability to have legal recourse over a crypto wallet and its custody seems to be the biggest necessary condition. This flies in the face of a decentralized, global effort. Investors wait on for the G20’s unified rules and regulations and updates from the SEC on the recent applications for Bitcoin ETFs.

- Is the data on trading coins too dark? The WSJ report last week raises the obvious issue on the data surrounding an exchange – there is a need for a token of tokens to record the transactions and keep them secure and measured. The clash is about of the provenance of transactions against the need for regulation to prevent such a cloak from hiding illegal activity.

- Should there be a central tape (like equities) or grouping of platforms (like FX) to monitor data? The simple measure of volume in crypto currencies is non-trivial to measure. There is double counting, proprietary trading from the exchange, HFT and algo trading that contort the numbers. For regulators, the ability to track money flows is a must, but for many the goal of crypto currencies is more about investments than trading. The hope of owning a coin as discussed last week, is in the call option for a disruptive technology to change economies on a super-scale.

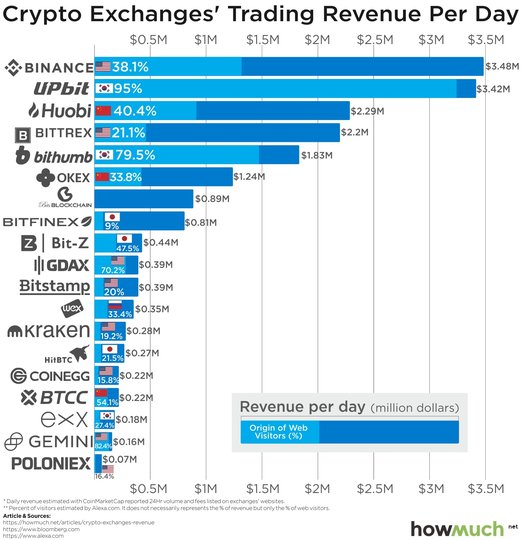

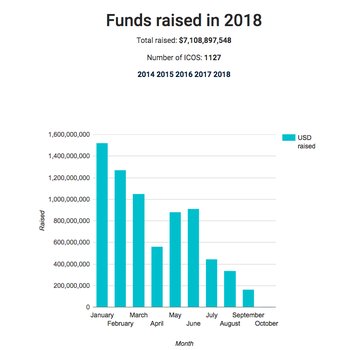

Question for the Week: If crypto exchanges are more profitable than new coins, is blockchain innovation dying? Estimates for profits at exchanges are $2-3bn over the last year. Estimates for total market cap in crypto is $300-$500bn. The charge of many about crypto exchanges is that they are taking in big margins and not delivering on the broader development of the market. To be specific, the exchanges are seen as trading with all the information – holding new coins ransom by demanding a 10-20% holding to list on the exchange and allow for market making, demanding 4% fees on trades, keeping the order book opaque if not dark and bifurcating information flows (preferring high frequency users over retail ones). The effect has been that many see the ICO (initial coin offering) dwindling in 2018.

If the amount of money being raised for new enterprises in blockchain is stalling, then the innovation is going to slowdown. This is the central tenant for many in all development. The post 2008 world saw the number of tech startups jump because of QE and zero rates, so the ICO money is much the same. Of course, there are two key factors beyond the control of exchanges in the flow of capital to blockchain development – 1) The value of bitcoin and other tokens, obviously this is self-reflective – the more leverage in a closed system the more prices rise. 2) The actual global interest rate of fiat money. The cost of capital remains the key factor more than the role of exchanges in setting the course for blockchain development. If there isn’t money in the new blockchain enterprises, they won’t make it regardless of the behaviors of the exchanges. The ability for ICOs to hold value rests on the forward curve of the market.

One block to developers of new enterprises using blockchain is the lack of one standard. Announced Oct 1, the Hyperledger Project and the Enterprise Ethereum Alliance (EEA) have agreed to collaborate on bringing common standards to the blockchain space and cross-pollinate a wider open-source community. This joining of forces is notable as EEA and Hyperledger represent two of the three largest and arguably most influential enterprise blockchain communities, the third being the R3 Corda ecosystem. The feeder stream of open source code for blockchain business ideas remains healthy. The future of innovation in this space seems to continue without much concern, despite the ICO slowing. This maybe the simple answer but it’s the best we have right now.

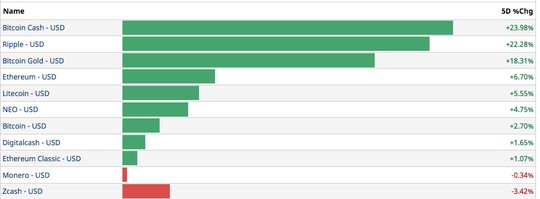

Market Recap: The rally back in Bitcoin and the continued gains in Ripple were the most notable stories in trading last week. However, markets were relatively quiet. The amount of realized volatility is less than in other weeks and suggests a larger risk for movement in October.

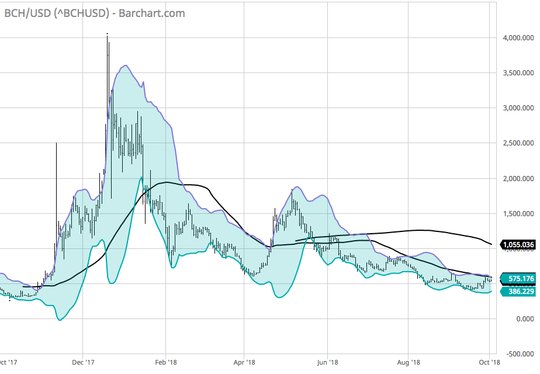

The gains in BCH were the headline but the larger 1-year chart suggests we remain below a breakout. The BTC breakout level of note is $6700 and the BCH Is $575.

The relationship of crypto trading to macro policy is something to consider given the FOMC rate hike and the focus on the NAFTA 2.0 (now USMCA) in the last week. The role of alternative money like gold matters to the value metrics of crytpo currencies. The Bitcoin Gold chart highlights this point and makes clear that the battle for alternatives to fiat money are reflexive to the price of the USD overall. The 1% gain in the US dollar index last week, the 0.5% drop in Gold, all that matters in the big picture for the path of crypto currencies.

BTG is telling us that a bottom is being put in place for the alternative space and that even with the move up in the USD last week, gold and other alternative money has a longer-term play building with $16.50 base for $45 test.

Comments

Log in or sign up to join the conversation.