Market Analysis

This year’s June quarterly stocks and acreage reports prompted a dramatic initial response when the USDA released them on Friday. Despite the US Ag Department planting report showing higher than expected corn & spring wheat seedings, soybeans 134,000 less than expected acres prompted a relief rally across the major CBOT markets after the report. This year’s June 1 stocks didn’t provide much price guidance when this quarter’s inventories were only modestly different than trade averages.

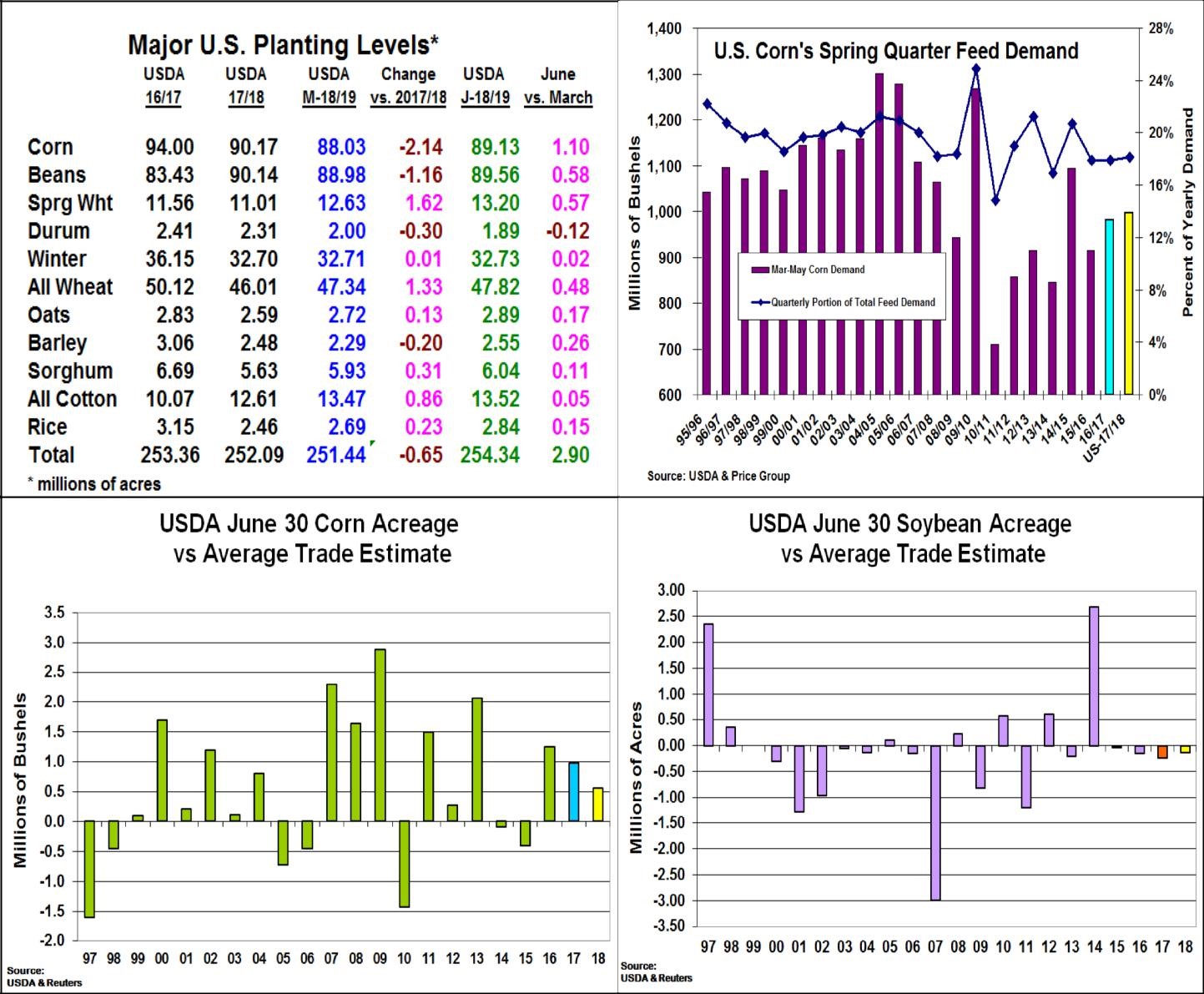

Overall, 2018’s planting levels for the 8 major US crops increased a surprising 2.9 million acres from the March intentions. This was led by corn’s 1.1 million acre jump, spring wheat’s 570,000 & soybean’s 575,00 increases and modest rises across the other US crops, except durum wheat that dipped 117,000 acres from March. Corn’s 566,000 larger seedings was the biggest surprise. Interestingly, no change in IA, IL or IN corn seedings were noted while the weather & credit challenged W & N Corn Belt rebounded with NE (400 K), MN (300 K), ND (300 K) and KS (300 K) leading the recovery after dropping their March levels. Soybeans larger acres came across the US with IL’s 300,000 increase and ND’s 500,000 drops the only dramatic state changes. Spring wheat’s 575,000 and 2.19 million acre increases from March and 2017 were substantially lead by more ND and MT seed-ings. However, ongoing concerns about smaller world competitor's crops (Russia, Europe and Australia) was Friday’s focus along with the US WW harvest moving past halfway.

The USDA’s quarterly stocks for soybean & wheat were very close to expectations. 2017/18’s wheat feeding will decline slightly while soybeans seasonal residual, exports and crush are confirming 2017’s crop size. Corn’s 38 million higher stocks at 5.31 billion bu. remains slightly disappointing when its used to calculate the US 3rd quarter feed demand. This pace remains only slightly higher than 2017 de-spite 2.5%-4% higher US livestock & poultry numbers.

(Click on image to enlarge)

What’s Ahead;

Prices retreated on weekend evening up and traders concerns about any tariff announcements ahead of July 6 US deadline. The USDA’s updated acreage levels have opened more 2018/19 crop potential, but corn’s last half July pollination weather & shrinking world wheat output remain highly important to both crops price. Use 15-20 & 27-40 cent rallies to sell 20-25% of old-corn and new-crop wheat.

Comments

Log in or sign up to join the conversation.