The Federal Reserve has been keeping interest rates steady, waiting to see whether the recent inflation surge will be temporary. That decision carries more risk after yesterday’s update of the Personal Consumption Expenditures (PCE) index for May, which shows that pricing pressure is increasing for reasons beyond surging energy costs tied to the Iran conflict.

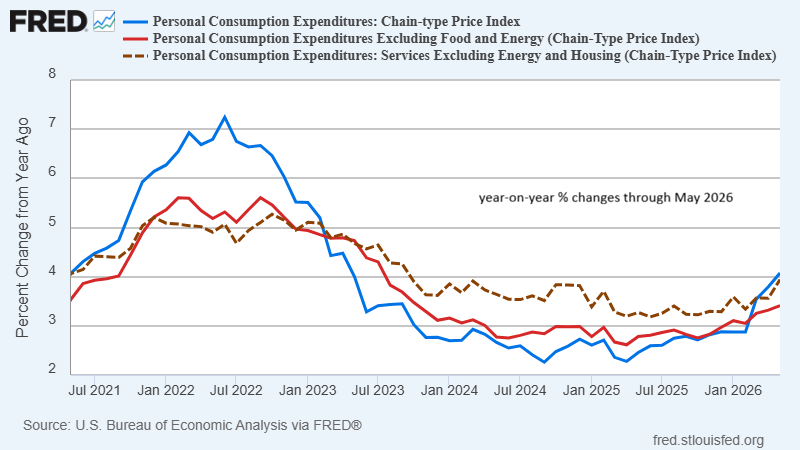

Headline PCE rose to a 4.1% year‑over‑year increase last month, the fastest pace in three years (blue line in the chart below). The view that energy costs have peaked—and will continue to fall—suggests that headline inflation will soon turn lower. But yesterday’s release highlights that inflation pressures are still building for reasons unrelated to energy, giving the Fed less room to argue that it can remain patient in deciding whether a hawkish pivot in monetary policy is necessary.

Core PCE inflation, which excludes food and energy, rose again to a 3.4% annual pace last month (red line in chart above). Another worrisome sign is the hotter trend in PCE services prices excluding energy and housing, which also extended its recent acceleration, rising 3.9%.

The implication: the Fed mahy be starting to lose control of the pricing trend, and for reasons that can’t be blamed on energy costs or the Iran war. A substantial reversal in inflation pressures in upcoming reports—particularly in the core readings—could buy the Fed more time to test the “inflation is transitory” narrative. But that is becoming a dangerous game.

At some point, if inflation pressure unrelated to energy continues to pick up, the central bank could face a repeat of 2021–2022, when it waited too long to respond to soaring prices. Although the current environment is less intense than the pandemic‑driven inflation surge several years ago, the threat to the Fed’s credibility is arguably higher in 2026 as Kevin Warsh, the new Fed chair, works to establish his policy bona fides.

If financial markets lose confidence early in Warsh’s tenure, his job of delivering “price stability,” as he vowed last week, will become more difficult.

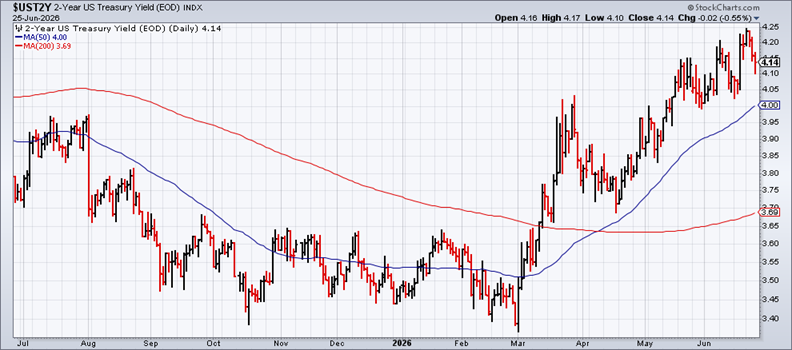

The bond market may ultimately determine whether the Fed is losing control of inflation. For now, investors are still willing to give Warsh the benefit of the doubt. The policy‑sensitive 2‑year yield edged lower yesterday for the third straight session. Yet the current 4.14% level keeps the recent uptrend intact and remains well above the Fed’s 3.50%–3.75% target range, reflecting the market’s expectation of further rate hikes.

Fed funds futures continue to lean toward no change at next month’s policy meeting, but the odds shift in favor of tightening in September.

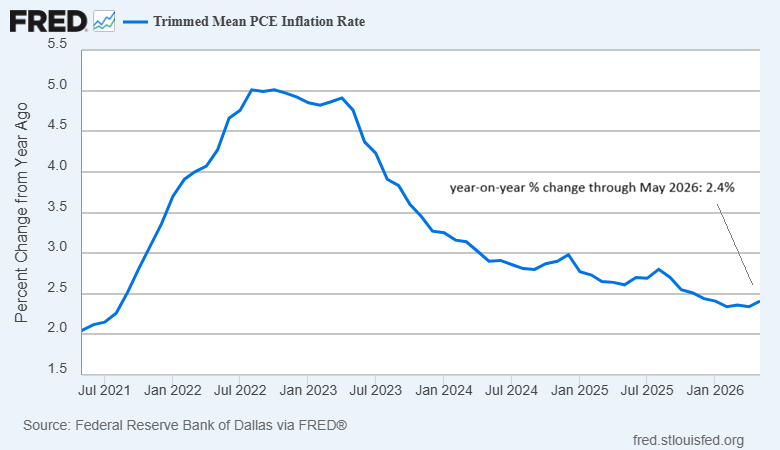

The counterargument is that the “trimmed mean” measure of inflation—which removes the most extreme price moves each month and which Warsh has cited as a preferred gauge—continues to show relatively subdued pricing pressure. This version of PCE inflation, calculated by the Dallas Fed, ticked up last month, but its 2.4% annual pace looks far less concerning than the trends noted above.

Although some economists argue that trimmed‑mean inflation indexes are superior to traditional core metrics, recent history is not encouraging. Notably, PCE trimmed‑mean inflation was slow to respond to the inflation surge in 2021–2022.

That raises the question: Will Warsh bet heavily on the trimmed‑mean’s softer inflation message?

Ultimately, the trajectory of inflation in the coming months will determine whether the Fed can preserve its institutional credibility. Should underlying price pressures continue to firm, the central bank may find itself compelled to tighten policy more aggressively than currently anticipated—an outcome that would underscore the costs of delayed action.

Comments

Log in or sign up to join the conversation.