Global Copper Cladded Aluminium Wire Market: The Lightweight Conductor Powering 5G and Electrification

The Global Copper Cladded Aluminium (CCA) Wire Market is evolving from a cost‑saving alternative into a strategic conductor platform at the heart of modern telecommunications, electrical infrastructure, and emerging vehicle wiring architectures. CCA wire, built as an aluminium core metallurgically bonded to an outer copper layer, combines copper’s conductivity and corrosion resistance with aluminium’s low weight and lower cost, making it highly attractive wherever long cable runs, dense network deployments, and lightweight design are critical.

As 5G base stations proliferate, electrification accelerates, and automation systems demand lighter, more efficient cabling, CCA wire has become an important bridge between performance, weight reduction, and material cost optimisation.

The Global Copper Cladded Aluminium Wire Market size stood at USD 2.83 Billion in 2025 and is projected to reach USD 4.14 Billion by 2031 at a CAGR of 6.55%. This growth is supported by volatile copper prices that drive substitution, rapid 5G rollouts and telecommunications densification, and lightweighting initiatives in automotive, aerospace, and Industry 4.0 cabling, even as technical limitations and installation complexity constrain penetration in some high‑power and safety‑critical applications.

➝ 𝐑𝐞𝐩𝐨𝐫𝐭 𝐃𝐞𝐬𝐜𝐫𝐢𝐩𝐭𝐢𝐨𝐧 Forecast Period: 2027–2031 Market Size (2025): USD 2.83 Billion CAGR (2026–2031): 6.55% Fastest Growing Segment: Telecommunications Largest Market: North America Market Size (2031): USD 4.14 Billion

➝ 𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐇𝐢𝐠𝐡𝐥𝐢𝐠𝐡𝐭𝐬: 𝐖𝐡𝐲 𝐂𝐂𝐀 𝐖𝐢𝐫𝐞 𝐌𝐚𝐭𝐭𝐞𝐫𝐬 𝐀𝐜𝐫𝐨𝐬𝐬 𝐒𝐞𝐜𝐭𝐨𝐫𝐬

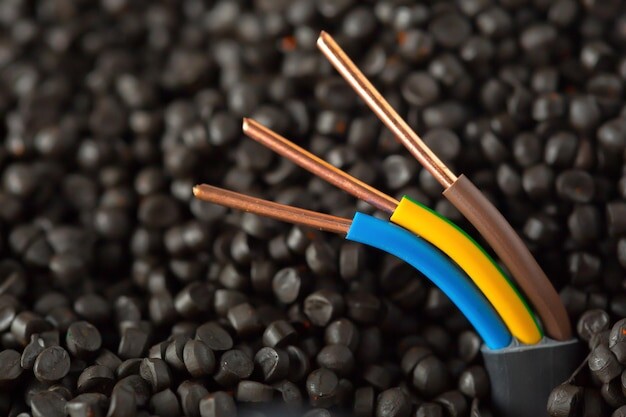

Copper Cladded Aluminium Defined: Structure and Benefits Copper-clad aluminium wire consists of an aluminium core metallurgically bonded to a continuous outer copper layer, forming a bimetallic conductor that behaves like copper at the surface and aluminium in the core.

This design delivers high‑frequency conductivity via the copper skin, thanks to the skin effect, while reducing overall mass and material cost through the aluminium centre. As a result, CCA wire offers an attractive conductivity‑to‑weight ratio and a compelling cost profile for long‑run cabling and densely packed installations

𝐆𝐋𝐎𝐁𝐀𝐋 𝐂𝐎𝐏𝐏𝐄𝐑 𝐂𝐋𝐀𝐃𝐃𝐄𝐃 𝐀𝐋𝐔𝐌𝐈𝐍𝐈𝐔𝐌 (𝐂𝐂𝐀) 𝐖𝐈𝐑𝐄 𝐌𝐀𝐑𝐊𝐄𝐓 𝐁𝐘 𝐒𝐈𝐙𝐄, 𝐒𝐇𝐀𝐑𝐄 & 𝐅𝐎𝐑𝐄𝐂𝐀𝐒𝐓 2031 | 𝐓𝐄𝐂𝐇𝐒𝐂𝐈 𝐑𝐄𝐒𝐄𝐀𝐑𝐂𝐇

Core Roles: Telecommunications, Electrical and Mobility In telecommunications, CCA wire is widely used in coaxial cables, drop wires, and feeder lines where RF signals travel primarily along the copper cladding, ensuring performance comparable to copper for many high‑frequency uses while significantly cutting weight on towers and structures.

In electrical and electronics, CCA serves in selected low‑voltage circuits, harnesses, and composite cables where mass reduction and cost savings are crucial. Automotive and emerging EV wiring harnesses increasingly specify CCA for low‑voltage or signal lines to support vehicle lightweighting and zonal architectures without compromising connectivity.

➝ 𝐊𝐞𝐲 𝐌𝐚𝐫𝐤𝐞𝐭 𝐃𝐫𝐢𝐯𝐞𝐫𝐬 & 𝐄𝐦𝐞𝐫𝐠𝐢𝐧𝐠 𝐓𝐫𝐞𝐧𝐝𝐬

Driver 1: Copper Price Volatility and Cost Optimisation Strong fluctuations and structural tightness in global copper supply are a primary catalyst pushing users toward CCA wire. As pure copper prices rise and become more volatile under electrification and infrastructure demand, the aluminium‑based core in CCA wire offers substantial material cost savings.

Utilities, electronics firms, and telecom operators can soften raw‑material cost shocks while maintaining acceptable high‑frequency performance, making CCA an attractive choice for cost‑sensitive, large‑scale cabling projects.

Driver 2: 5G Network Expansion and Telecommunications Densification The rapid rollout of 5G networks and densification of telecom infrastructure are aggressively driving demand for CCA conductors. Next‑generation networks require millions of base stations, massive coaxial cabling, and lightweight feeds, where reducing tower load and installation complexity is critical.

CCA’s favourable conductivity‑to‑weight ratio enables long‑distance signal transmission with less mass than solid copper, supporting faster deployment and lower overall system costs as global 5G subscriptions and base station counts continue to climb.

Trend 1: Zonal Wiring Architectures in Electric Vehicles The transition to zonal wiring architectures in EVs is reshaping demand for lightweight conductors. Instead of bulky central harnesses, zonal designs use local controllers connected by multiple low‑voltage and data lines, creating a premium on high‑density, low‑mass wiring. CCA wire is increasingly specified for these signal and low‑power links, as it reduces harness weight and simplifies routing while still providing sufficient conductivity where the skin effect dominates current flow.

Trend 2: Hybrid Fiber‑Coaxial Cables for Automation and Robotics Industry 4.0 and advanced automation systems are driving development of hybrid fiber‑coaxial cables that combine optical fibers for data with CCA conductors for power. In robotic arms and dynamic drag chains, lightweight CCA reduces inertial mass and improves flex life compared to heavier copper conductors, allowing faster motion and longer cable service life. This composite cabling trend opens specialised application niches for CCA in high‑performance manufacturing cells and industrial networks.

➝ 𝐊𝐞𝐲 𝐌𝐚𝐫𝐤𝐞𝐭 𝐂𝐡𝐚𝐥𝐥𝐞𝐧𝐠𝐞𝐬

Challenge 1: Lower Conductivity and Galvanic Corrosion Risk The main technical challenge is CCA’s lower bulk conductivity versus pure copper and the risk of galvanic corrosion at termination points. To carry the same current as copper, CCA often needs a larger conductor size, which can be problematic in space‑constrained installations. If the copper cladding is damaged during stripping or connection, exposing aluminium, contact with dissimilar metals can lead to corrosion, connection failures and safety concerns. These factors impose strict installation and connector requirements.

Challenge 2: Limited Adoption in High‑Power, Safety‑Critical Systems Because of these technical limitations and handling demands, many high‑power and safety‑critical applications remain hesitant to adopt CCA. Installers must use specialised connectors and follow careful procedures, which increases complexity and labour cost. As a result, CCA is often restricted to specific low‑voltage or RF niches even though the broader cable market is expanding rapidly, meaning performance constraints directly cap the material’s market share relative to conventional copper solutions.

➝ 𝐒𝐞𝐠𝐦𝐞𝐧𝐭𝐚𝐥 𝐈𝐧𝐬𝐢𝐠𝐡𝐭𝐬

Fastest‑Growing Segment: Telecommunications Telecommunications is the fastest‑growing end‑use segment in the Global CCA Wire Market. In RF and high‑frequency cabling, the skin effect ensures current flows primarily along the outer copper layer, allowing CCA to deliver copper‑like performance while reducing weight and cost. As operators expand 5G, fiber‑deep networks and dense antenna arrays, adoption of CCA in coaxial and feeder cables accelerates, supporting a steep growth curve in this segment.

Other Key End‑Uses: Electrical & Electronics and Automotive Electrical and electronics applications use CCA in selected low‑voltage circuits, composite cables and harnesses where cost and weight must be controlled without sacrificing too much conductivity. Automotive and EV wiring systems increasingly apply CCA to low‑power and signal lines in harnesses and zonal architectures, reducing vehicle mass and improving packaging while leaving high‑power paths to more traditional copper options. Other uses span various industrial and consumer wiring niches where careful design mitigates CCA’s limitations.

➝ 𝐑𝐞𝐠𝐢𝐨𝐧𝐚𝐥 𝐈𝐧𝐬𝐢𝐠𝐡𝐭𝐬

North America: Largest Market with Strong Regulatory Framework North America is the largest regional market for CCA wire, supported by robust telecommunications and automotive industries and growing use in building and branch circuits. The region benefits from clear safety standards and codes that govern permissible CCA applications, helping improve market confidence where the material meets performance and safety criteria. This alignment of cost‑efficient, lightweight wiring needs with regulated acceptance positions North America as a leading demand centre for CCA conductors.

Other Regions: Asia Pacific, Europe and Emerging Markets Asia Pacific contributes significant demand through large‑scale telecom deployments, electronics manufacturing and wire production, including specialised conductors and magnet wire. Europe focuses more selectively on high‑performance and regulated uses, balancing innovation with strict safety and reliability expectations. South America and the Middle East & Africa offer incremental growth prospects as their telecommunications and automotive sectors expand and seek lower‑cost materials for network and wiring projects.

➝ 𝐑𝐞𝐜𝐞𝐧𝐭 𝐃𝐞𝐯𝐞𝐥𝐨𝐩𝐦𝐞𝐧𝐭𝐬

Regulatory acceptance of CCA building wire in key electrical codes has opened new opportunities in residential and commercial branch circuits, particularly for low‑load lighting and control lines. Manufacturers have expanded magnet wire and special conductor capacity in North America and Southeast Asia to serve EV motors, transformers and electronics, including CCA‑based products. Design specification platforms have begun listing CCA building wire, giving architects and engineers clearer pathways to include bimetallic conductors in project plans, while new overseas facilities for special conductors increase global supply and improve service to electronics and automotive customers.

➝ 𝐂𝐨𝐦𝐩𝐞𝐭𝐢𝐭𝐢𝐯𝐞 𝐀𝐧𝐚𝐥𝐲𝐬𝐢𝐬

Key Market Players Hengtong Group Co., Ltd. | Sumitomo Electric Industries, Ltd. | Furukawa Electric Co., Ltd. | Prysmian Group | Nexans S.A. | LS Cable & System Ltd. | Belden Inc. | Southwire Company, LLC | Amphenol Corporation | Encore Wire Corporation

Leading companies focus on developing high‑reliability CCA products, improving bonding quality between copper and aluminium, and refining connector and installation guidelines to reduce failure risks. Many are expanding production footprints, enhancing regional service capabilities, and promoting CCA in telecom, EV and building‑wire applications where lightweight, cost‑efficient conductors provide clear value. Collaboration with standards bodies and code committees also plays a role in broadening accepted use cases.

➝ 𝐑𝐞𝐩𝐨𝐫𝐭 𝐒𝐜𝐨𝐩𝐞

Copper Cladded Aluminium Wire Market, By Sales Channel:

Direct

Indirect

Copper Cladded Aluminium Wire Market, By End Use:

Telecommunications

Electrical & Electronics

Automotive

Others

Copper Cladded Aluminium Wire Market, By Region:

North America

Europe

Asia Pacific

South America

Middle East & Africa

➝ 𝐅𝐮𝐭𝐮𝐫𝐞 𝐎𝐮𝐭𝐥𝐨𝐨𝐤

The Global Copper Cladded Aluminium Wire Market is expected to grow steadily through 2031, powered by copper price volatility, 5G rollout, EV lightweighting, and Industry 4.0 cabling needs. Technical limitations around conductivity and corrosion will continue to restrict use in some high‑power and safety‑critical domains, but targeted design guidelines, better connectors, and clearer codes should gradually expand the safe application space.

Producers that optimise bonding technology, educate installers, align with telecom and EV architecture trends, and position CCA as a proven, code‑accepted solution will capture the most value as demand for lightweight, cost‑efficient conductors deepens.

➝ 𝐅𝐀𝐐𝐬: 𝐆𝐥𝐨𝐛𝐚𝐥 𝐂𝐨𝐩𝐩𝐞𝐫 𝐂𝐥𝐚𝐝𝐝𝐞𝐝 𝐀𝐥𝐮𝐦𝐢𝐧𝐢𝐮𝐦 𝐖𝐢𝐫𝐞 𝐌𝐚𝐫𝐤𝐞𝐭

What is Copper Cladded Aluminium (CCA) wire? CCA wire is a bimetallic conductor with an aluminium core bonded to a continuous outer copper layer, designed to combine copper‑like high‑frequency conductivity and corrosion resistance with aluminium’s low weight and lower material cost.

Why is the Telecommunications segment the fastest‑growing end‑use? Telecom cabling for 5G and RF systems exploits the skin effect, where current flows mainly on the copper surface, allowing CCA to offer copper‑equivalent high‑frequency performance while significantly cutting weight and cost in dense network deployments.

What are the main technical limitations of CCA wire? CCA has lower bulk conductivity than pure copper, often requiring larger gauge sizes, and is vulnerable to galvanic corrosion if the copper cladding is damaged at terminations, demanding specialised connectors and careful installation practices.

Why is North America the largest regional market for CCA? North America’s strong telecommunications and automotive sectors, combined with clear safety codes and standards that define where CCA is acceptable, support broad commercial use in lightweight, cost‑efficient wiring solutions for networks and vehicles.

In which applications is CCA wire expected to see the most future growth? Future growth is strongest in 5G and telecom cabling, EV zonal wiring and harnesses, hybrid fiber‑coaxial cables for automation, and selected building‑wire and low‑voltage circuits where weight reduction, cost optimisation, and code compliance align.

Comments

Log in or sign up to join the conversation.