There is a noticeable difference in market and economic outlooks between those on the front lines of the fixed income markets and those sitting back at HQ in wealth management. I have observed this even within the same firm.

Readers know that I am a fan of Morgan Stanley economist, Ellen Zentner. Ms. Zentner’s outlook on the economy and the timing of Fed policy has been very accurate. While a guest on CNBC’s “Closing Bell” show, Ms. Zentner pointed out that the economy should be able to absorb mild Fed Funds Rate increases fairly well. She pointed out that much of the job and wage growth has been on the lower end of the income spectrum and that tightening into, what looks to be a low inflation environment probably results in a flatter UST yield curve.

The very next morning, Morgan Stanley Wealth Management head, Greg Fleming was on CNBC’s Squawk Box telling viewers how well the economy is doing and that it could drive the market higher. He continues to hang is hat on low fuel prices.

This dichotomy of opinion is not endemic to Morgan Stanley, by any means. I have seen it around the industry. Most of the wealth management commentary I read points to a resumption, if not an acceleration of economic growth. Most commentary I read from the trading and institutional areas of the business expresses a much more cautious view.

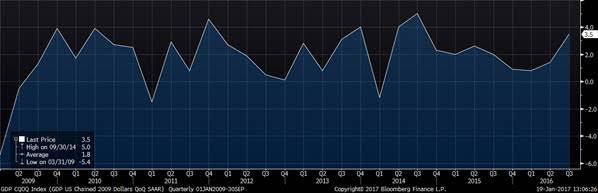

I understand that in the wealth management business, one needs to be positive so as not so frighten clients. However, Bond Squad’s mission is to provide subscribers with a front line view of the fixed income markets. From the front lines, it appears that the U.S. economy has probably done most of the recovering it is going to do in the current economic cycle. The underlying trend appears to be settling into a 2.0% (+/-) economy. However, there is a monster which threatens to spoil our happy economy.

You’re a mean one Mr. Grinch

For more than two years, I have been writing about frothy conditions in the high yield bond market. My concerns were featured in the Wall Street Journal in 2013. In 2014, Bloomberg News quoted me several times. In June 2014, I suggested that the junk debt market was overvalued and, where investor suitable, investors and advisors may want to take on a bit more duration risk to generate yield over credit risk. This was a decidedly unpopular view on the retail side of the business. However, for anyone on the front lines, warning signs were flashing.

I also warned on an overdone energy sector. In my 2015 Outlook, published on 12/23/14 I wrote:

“When we view high yield from a fundamental perspective, the space appears to be overdone. If there isn’t a bubble in the oil shale industry, there is almost certainly a blister. As such, we would be underweight small high yield oil producers and service companies. That sector of HY should be reserved for total return speculators who can tolerate the occasional default, rather than moderate investors looking for increased income.”

I didn’t know how bad things would get in high yield, generally or how bad things would get in energy, specifically. Because I did not know how bad it would get is why I became cautious. Warnings have been flashing like Christmas lights in the high yield space. Yet many investors chose to ignore the warnings.

Extreme monetary accommodation usually causes capital misallocations and asset bubbles somewhere in the economy. Most pundits debated whether the bubble was in equities or auto loans. I have consistently pointed to overvalued conditions in junk debt and to the illiquid conditions which could make exiting difficult. Recent developments support my outlook.

My view of the high yield bond market is; this is probably not a dip, but a fundamental repricing of risk. Although there could be a modest junk debt rebound, there is probably another leg down in the first quarter of 2016, when corporate defaults are expected to increase. My concern is that some investors are not going to get out of the burning room alive. Even institutional portfolio managers are having difficulty exiting junk debt positions. Some managers have been forced to sell better bonds to meet client cash needs. This threatens to cause a spillover into the broader high yield market. I should note that more than half of all high yield oil and gas producer bonds are trading at less than 50 cents on the dollar.

Bank of America Merrill Lynch high yield strategist, Michael Contopoulos, told a CNBC audience that “leverage in non-commodity high yield is the highest it has ever been.”

Over/Under

The spillover of which I am most concerned is the spillover of pain form the commodities sector into the broader economy. The oil and gas boom (and to a lesser extent, a metals boom) not only resulted in the hiring of oil and gas workers, but of manufacturing and service workers as well. The expansion of energy production resulted in the construction of roads, rail lines, homes, stores, etc. These created jobs. The commodities boom also brought about an increase in small service businesses (plumbers, electricians, medical professionals, etc.)

Monetary and fiscal policy makers often look to infrastructure spending to boost economic growth following a recession because of the multiplier effect caused by infrastructure spending. The so-called commodities super cycle was, in a sense, a private-sector-funded infrastructure program. My concern is that, without the commodity sector multiplier effect, the U.S. economy could see a few tenths (or more) shaved off of 2016 GDP, even with low oil prices, versus 2015 data. Thus, we could be looking at 2016 annual GDP right around the 1.75% to 2.00% area.

I do expect oil prices to remain low. Maybe not as low as they are now (WTI was $35.56 per barrel at the time of this writing), but now even $50 oil looks difficult. Since oil prices began falling in earnest in Q3 2014, U.S. oil producers have become much more efficient. Most U.S. oil production is now viable as low as the $50 per barrel level and some production is viable well into the $30s. What could happen is that stronger producers become even more efficient. This would probably be accomplished by a combination of layoffs, equipment modernization and buying the assets of failed companies on the cheap. Where oil trades in 2016 I cannot say. However, if someone gave me an over/under of $50 at the present time. I would take the under for 2016. Oil prices will probably come back above $50 someday, but this probably does not happen prior to a clearing-out of the weaker energy companies.

I should also note that the International Energy Agency is forecasting that global demand growth should slow to 1.2 million barrels per day from a current expansion pace of 1.8 million barrels per day. At the same time, global supply is expected to increase. I just can’t see how oil can make much of a rebound.

Comments

Log in or sign up to join the conversation.