Market Analysis

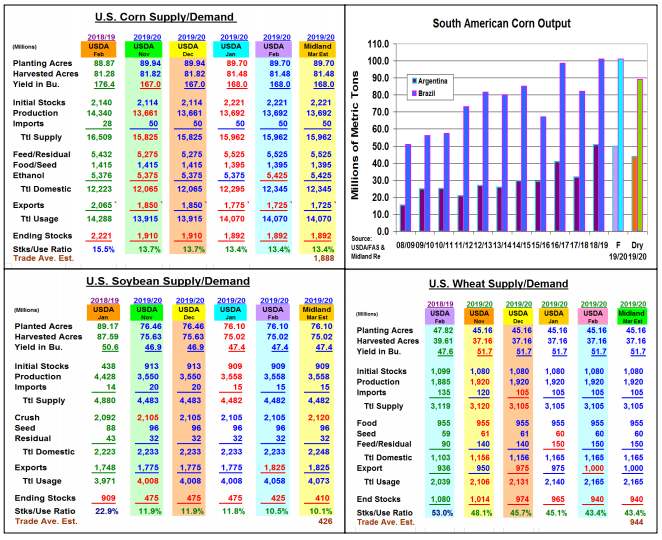

The upcoming World Output & Supply/Demand revisions will be released on March 10. The USDA hasn’t traditionally made many changes in this month’s US & World S&D update. The Ag Department usually likes to see its quarterly stocks and processing reports before making domestic demand changes. This year’s S. American growing season started late because of dryness that delayed Brazil’s bean seedlings and impacted Argentine first crop corn and soybeans potential in December and early January. Rains have returned in Brazil with heavy amounts in the past month delaying the northern bean harvest vs. last year. This could have an impact on Brazil’s large safrina (second crop) corn crop if this region’s dry season would begin in April vs. mid-May like last year. This makes S Am. output vulnerable to a 15-18 mmt setback if dryness occurs.

After last month’s ethanol and export adjustments, no changes in March’s US corn demand levels are expected. January’s 5.7% yearly jump in biofuel demand seems to confirm the USDA’s increase last month. Exports remain sluggish, but China issuing 1-year tariff exemptions starting this month likely keeps the USDA patience to see what might occur. No change in feed demand is expected ahead of the upcoming quarterly stocks report either so corn’s March ending stocks will probably remain unchanged.

In soybeans similar to corn, the USDA will likely hold their export forecast after last month’s increase given the Chinese new export tariff exemptions. The ongoing strong US processing demand (3 out of last 4 months at record levels) suggests this usage level could be upped 15 million bu. This could tighten US soybean ending stocks to 410 million bu. despite 1 mmt rise in Argentina’s crop to 54 mmt.

Currency values remain a trading issue for wheat and other US ag products. However, no change in US exports is expected this month as China begins its quest to meet the recent Phase 1 ag import commitments.

What’s Ahead:

The Coronavirus remains a dark cloud. Hopefully, warmer weather and improving Chinese logistical and economic activity will prompt more ag imports from the US. Saturated soils in the US and building dryness in Argentina & S. Brazil keeps March weather important. Utilize May strength to advance corn and soybean sales 20% at $3.88-92 & $9.15-20 and 15% of your new-crop at $3.97-$4.00 & $9.40.

Comments

Log in or sign up to join the conversation.