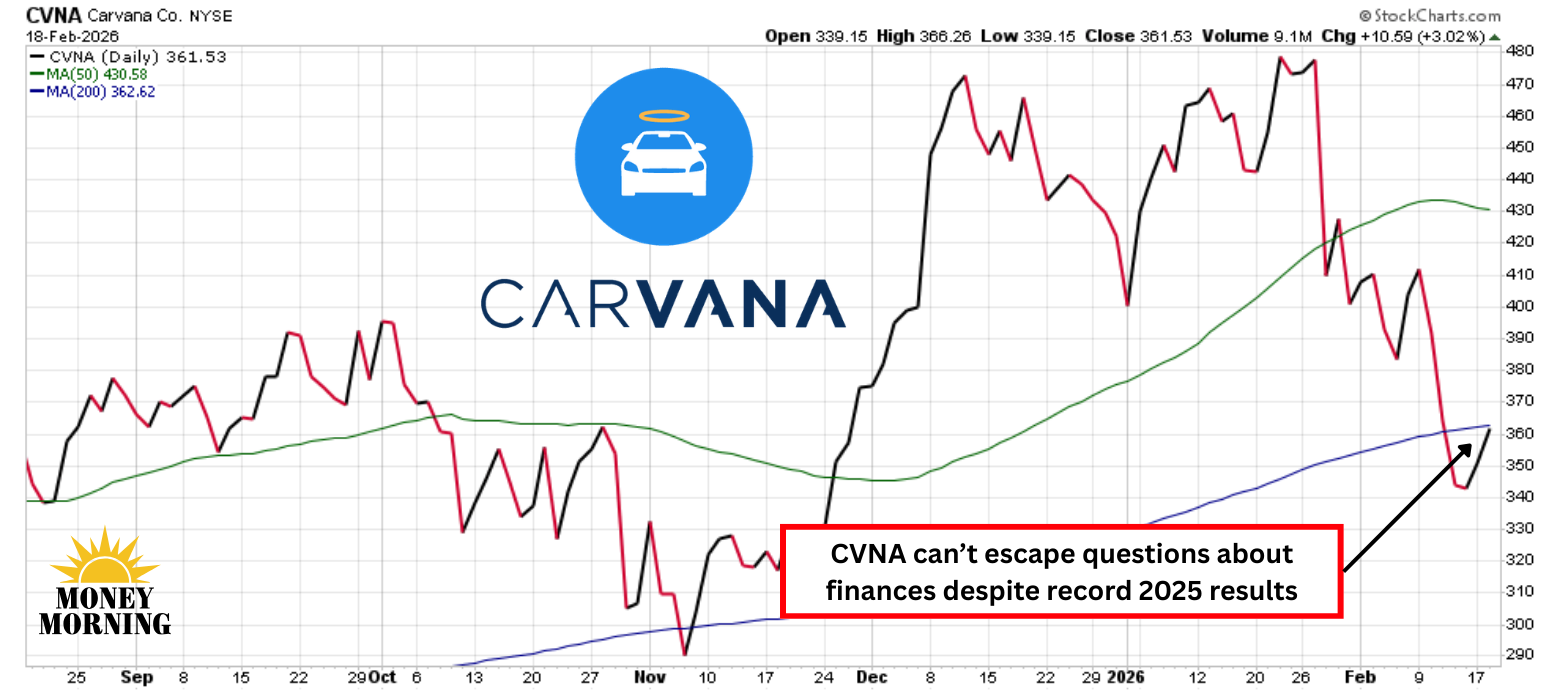

Carvana (CVNA) just delivered a blockbuster close to 2025, reporting record full-year revenue of $20.3 billion, up 49% year-over-year, alongside net income of $1.9 billion and a staggering 596,641 retail units sold, a 43% increase. The fourth quarter shone brightly too, with $5.6 billion in revenue (58% growth), 163,522 units sold (43% up), and net income of $951 million. Management's guidance points to even stronger performance in 2026, fueled by operational efficiencies and market share gains toward a long-term goal of 3 million annual units.

Yet, investors are dumping the stock, sending shares plunging, as a Q4 miss on adjusted EBITDA at $511 million versus expectations of around $536 million, and dragged down by rising reconditioning costs that eroded gross profit per unit by $244 to $6,427. If you're still tempted to buy into this dip, proceed at your own peril – there are deeper issues lurking beneath the surface.

Shadows from Short-Seller Scrutiny

A persistent cloud has overshadowed Carvana since Gotham City Research released a devastating report last month alleging undisclosed related-party transactions that masked a far worse financial condition than publicly reported. The accusations centered on Carvana's loan sales, suggesting heavy reliance on entities tied to CEO Ernie Garcia III's family, including DriveTime and its subsidiary Bridgecrest.

In the recent earnings call, Carvana's management dismissed these claims, particularly on related-party loan sales, saying it had refuted them as "100% inaccurate." But Gotham fired back with an update yesterday, asserting it has "on-the-record evidence" from public records showing Bridgecrest as the lienholder on dozens of Carvana-sold vehicles, contradicting official statements. They identified 34 specific VINs where Bridgecrest holds the liens, highlighting how Carvana finances sales initially before offloading loans that ultimately land with these affiliates. This setup, Gotham argues, inflates gains on loan sales while maintaining opacity.

Fragile Dependencies and Financial Opaqueness

Gotham's latest revelations paint Carvana's third-party dependencies as more precarious than acknowledged, with leverage ratios potentially reaching 20x in key financing arms, amplifying risks in a volatile market. The company's "originate-to-sell" model funnels loans to securitizations, but the lack of transparency around servicers like Bridgecrest raises red flags.

Investors are left questioning the true health of Carvana's balance sheet, especially as extensions on subprime loans in securitizations have doubled recently. This murkiness isn't just academic – it erodes trust, particularly when short-sellers provide verifiable data challenging management's narrative.

Bottom Line

Much of Carvana's sales engine relies on subprime borrowers, with over 44% of originated loans classified as non-prime and a significant portion deep subprime, contributing roughly 26% to gross profits through loan sales.

But subprime auto loan delinquencies have hit a 32-year high, with 60+ day past-due rates at unprecedented levels since 1994, driven by extended terms up to 120 months, high loan-to-value ratios, and loose lending standards. Borrowers are trapped in negative equity, facing repossessions that could flood the market.

With financially distressed buyers forming the core of Carvana's high-risk customer base, and unresolved questions about its finances persisting, this former market darling remains far too risky for investors to buy and they should steer clear until management provides greater clarity.

Comments

Log in or sign up to join the conversation.