While we turn the calendar page on to 2016, corporations are bracing themselves for the upcoming earnings season. For many retailers, the holiday season represents a large portion of the company’s earnings throughout the year. The first retailer to report in 2016, Bed Bath & Beyond (BBBY), is expected to report earnings and same store sales less than previously forecasted.

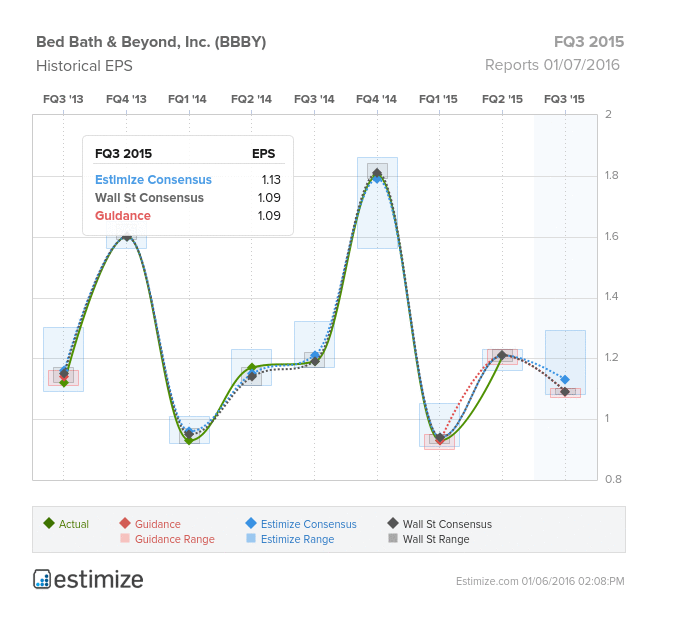

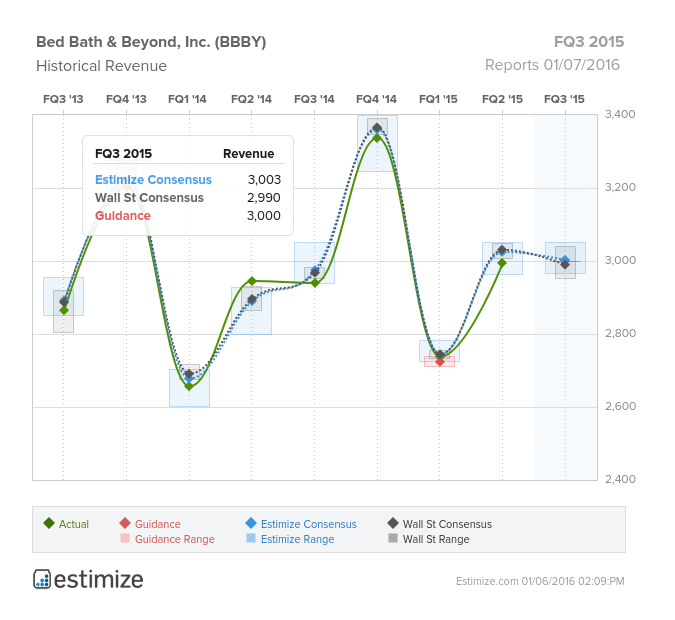

This past year has been particularly bleak for the company due to a shift in resources towards online shopping which has reshaped the retail industry. Despite online sales growing 25% in 2015, Bed Bath & Beyond’s digital channel only represents a fraction of the chain’s total sales. In fact, the company reported negative earnings surprises seven of the last eight quarters and consequently share prices declined 37% in 2015. Coming into their FQ3 2015 earnings, the Estimize consensus calls for revenue of $3.004 billion and EPS of $1.13, slightly higher than Wall Street’s estimates and corporate guidance. Compared to FQ3 2014, this represents a YoY decline in EPS of 4%. Unfortunately in the near future, Bed Bath & Beyond will be plagued with shrinking margins, pressure from online competitors and the rising cost of implementing an e-commerce platform.

A large portion of Bed Bath & Beyond’s anemic growth can be attributed to the increasing pressure online companies like Amazon (AMZN) have placed on the retail industry. In an effort to catch up, the household retailer devoted a significant amount of resources to build out their online platform. At the same time, same store sales are expected to decline on the back of weaker in-store transactions and a soft retail sector. Currency headwinds have also dragged down Canadian sales and negatively impacted margins. Looking ahead, Bed Bath & Beyond should continue to exhibit weaker sales led by restructuring investments, currency headwinds and decreasing margins.

Do you think BBBY can beat estimates? There is still time to get your estimate in.

Comments

Log in or sign up to join the conversation.