Photo Credit: Mike Mozart

Pier 1 Imports, Inc. (PIR) Consumer Discretionary - Specialty Retail | Reports April 13, After Market Close

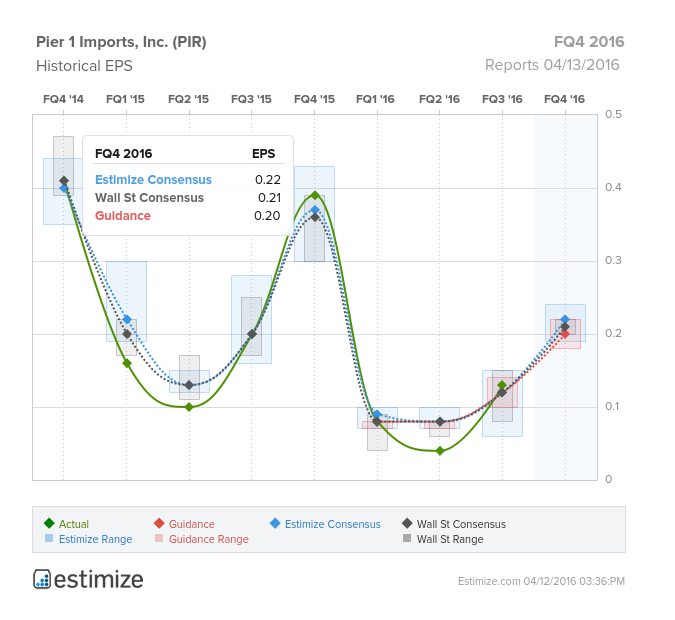

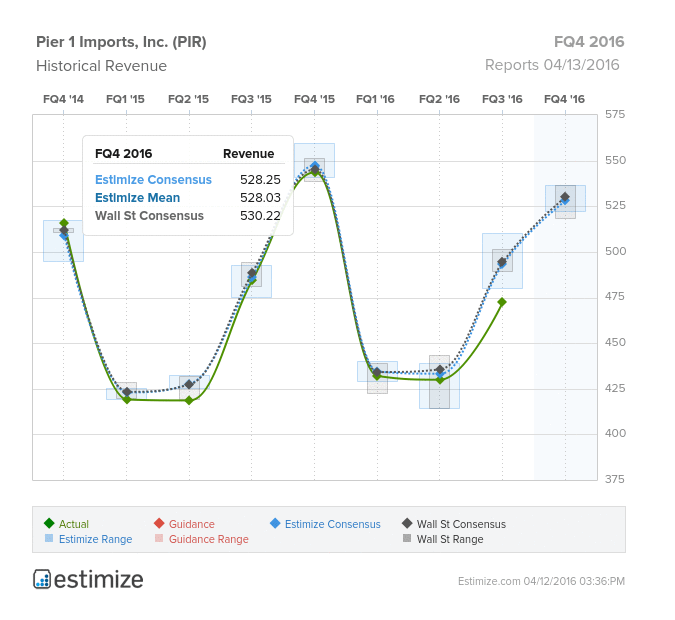

High-end home furnishing companies have had a rocky start to 2016 after poor earnings from Restoration Hardware and William Sonoma. This week, Pier 1 Imports hopes to reverse the trend when it reports fourth quarter earnings. The company is coming off a mixed third quarter in which it beat on the bottom line but missed its sales number by $20 million. Expectations have been generally low for speciality retailers this quarter and Pier 1 has been no different. The Estimize community is calling for EPS of $0.22, 1 cent higher than Wall Street, and revenue expectations of $527.66, $2 million below the Street. Compared to the same period last year, earnings are projected to decline 45% while sales are expected to fall 3%. The market has reacted negatively to this information, cutting the stock in half in the past 12 months.

Pier 1 has fallen victim to volatile markets and weak economic conditions. The company’s merchandise largely consists of high quality, imported furnishing products which have lost favor with the common person. Pier 1 competes in a heavily concentrated space with retail giants like Costco, Wal-Mart, and Home Depot to name a few. Meanwhile, currency headwinds continue to hurt earnings and margins. Margins are expected to decline yet again, marking the second consecutive year of sharp declines. On the bright side, the company has done an admirable job of improving its product mix, offering low priced impulse products to drive traffic to stores. Should the pricing environment improve or real wages increase, Pier 1 has an opportunity to spark growth in key metrics.

Comments

Log in or sign up to join the conversation.