There’s BOTH a lot of hype, AND substantial long-term demand, for select critical materials. I think the hype falls under the categories of certain Rare Earth Elements (“REEs”) and a few military & high-tech metals, but there’s clear strategic & fundamental demand for indispensable commodities like silver, uranium & copper.

Like “superfoods” or “essential” health supplements, some are more important than others… A key differentiating metric is how replaceable a scarce material truly is. Some juniors contend their featured metals are irreplaceable when in fact they really aren’t.

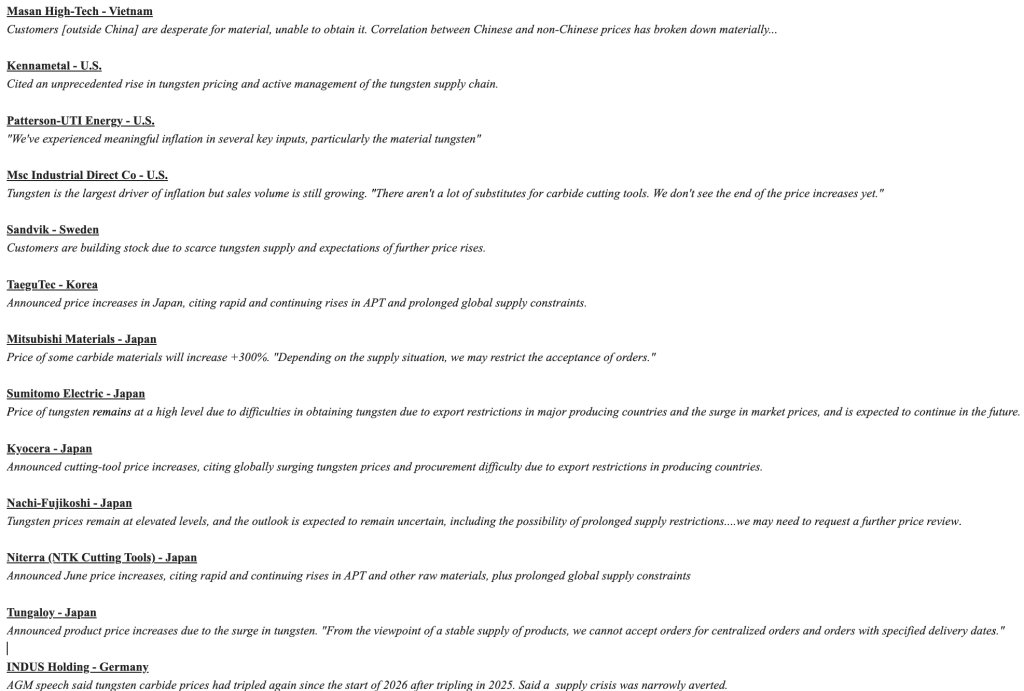

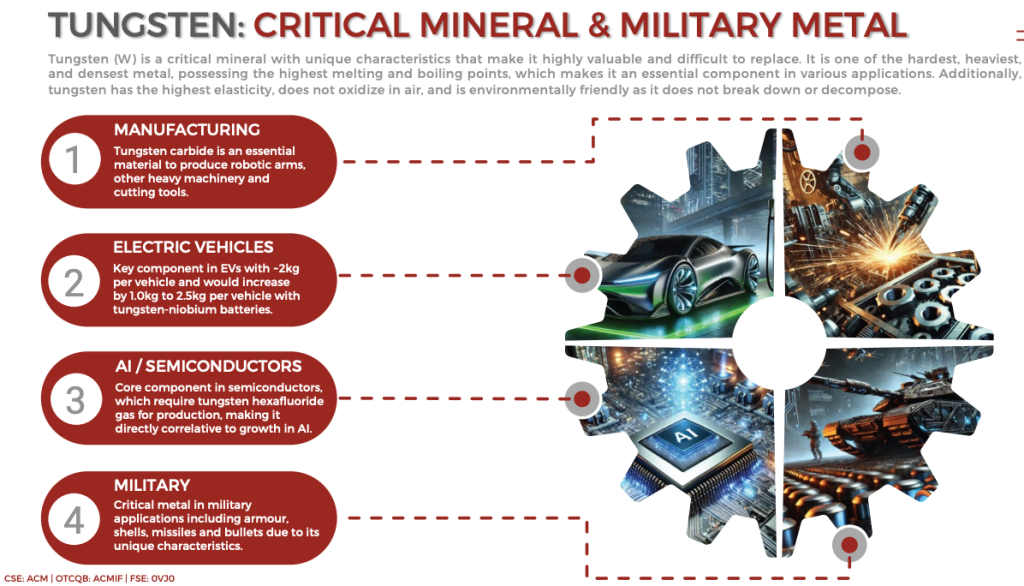

A metal I have high conviction in is tungsten. Tungsten’s extreme hardness & highest melting point of any metal make substitution nearly impossible for key industrial uses. And, in my view, recycling can’t scale fast enough to close the gap. The following image depicts recent commentary on tungsten fundamentals.

From Linked-in post by Mike Henshaw of PURE Asset Management

Project Blue estimates that defense demand, which accounts for ~12% of the tungsten market, is expected to grow to ~15% between 2027 and 2028… Global defense sector demand grows by ~8% per year. That’s twice the demand CAGR of copper.

Some pundits & analysts expect defense applications to overtake automotive as the top end-use by the mid-2030s. Tellingly, Western governments are already paying a premium for non-Chinese tungsten supply.

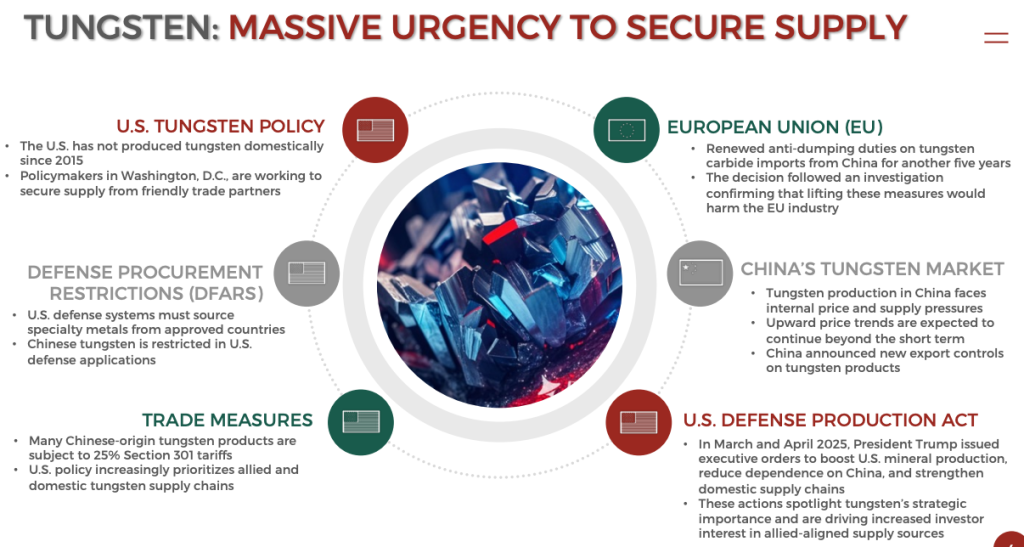

According to the U.S. Geological Survey, 83% of tungsten comes from China, and adding Russia, Vietnam & North Korea bumps the total to 90-91%%. Since Feb. 2025, Beijing capped authorized exporters at ~15 companies for 2026-2027.

The U.S. added tungsten to its critical minerals list, launched DPA stockpiling, and is barring Chinese, Russian, Iranian & North Korean tungsten from key defense applications starting Jan 1, 2027. And, the EU is building its own stockpile.

Juniors that can deliver new supply this decade are very well positioned. Almonty Industries’ Sangdong restart in South Korea is getting significant attention, but it’s only expected to reach ~2,300 tonnes of concentrate per year, a small fraction of the world’s growing needs.

Tungsten is essential in carbide tooling for machining, mining, and manufacturing. Supply is highly concentrated and, outside of China, is slow to expand. New mines can take a decade or more, keeping deficits tight. Inside China increasing production will be difficult.

The country faces declining ore grades, stricter environmental rules, production quotas, and reserve depletion concerns. New long-term sustainable supply from the U.S.. Canada, Europe & Australia is incredibly important.

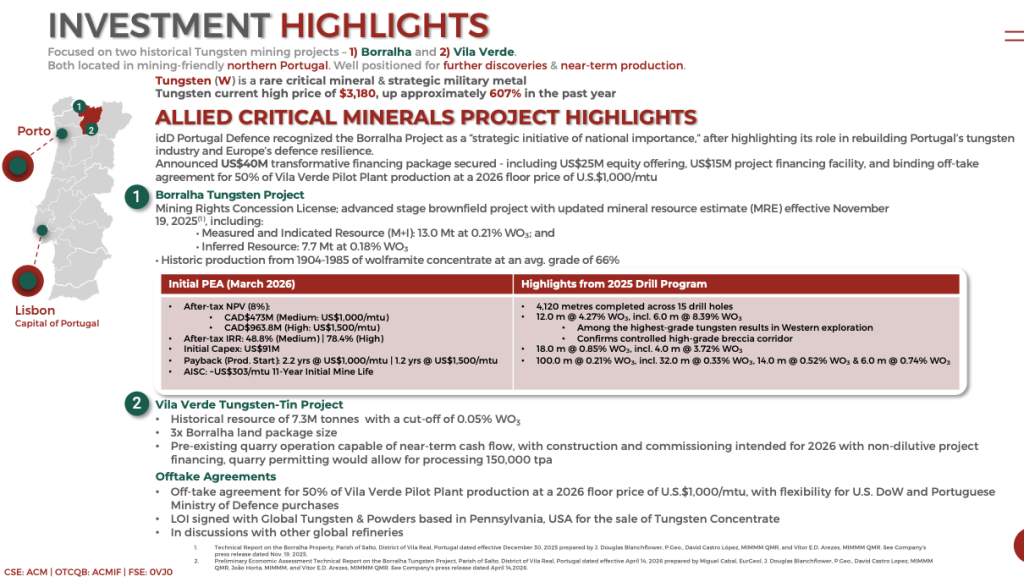

A company that has caught my attention is Allied Critical Metals (CSE: ACM) / (OTCQB: ACMIF) a junior advancing two 100%-owned, past-producing tungsten projects in northern Portugal — Borralha (one of the EU’s largest undeveloped resources with excellent metallurgy) and Vila Verde (tungsten-tin with significant exploration upside).

This is a company that’s cashed up and reporting continuous de-risking news flow, such as this morning’s drill result press release.

Positioned as a near-term, potentially low-cost, Western producer, it benefits from Portugal’s mining-friendly jurisdiction and EU critical minerals push. I have been speaking with CEO Roy Bonnell, and conducted the following interview in the week ended July 10th.

Roy, when did the tungsten price start moving meaningfully higher? What was the reason?

Near the time we went public in 1H/25, tungsten prices, especially outside of China, started to soar. The main driver was U.S. / China tariffs. We believe that military uses of tungsten is different then almost all other end uses. If a government needs tungsten, it often needs it ASAP and nations are typically NOT price sensitive.

Trump has made critical metals a key policy issue and has stuck with it. That’s why the non-Chinese tungsten price is up as much as +900% since early last year. I get asked why the tungsten price won’t fall back like the lithium (“Li”) price did (Li fell 80% from its 4Q/22 high). That’s a good question.

The difference between tungsten an Li is there was no real shortage of Li, but of Li processing capacity… And, there are substitutes for Li in batteries, like sodium-ion. Not to mention, new battery chemistries keep coming… That’s simply not the case tungsten.

NOTE, mtu stands for metric tonne unit in tungsten pricing (mainly for APT or concentrates). It’s an industry convention for quoting prices per 10 kg of WO₃ content (WO3 = tungsten trioxide). Tungsten is traded based on contained WO3, so MTU makes pricing concentrates easier. Conversion: 1 metric tonne = 100 MTU (since 1 MTU = 10 kg).

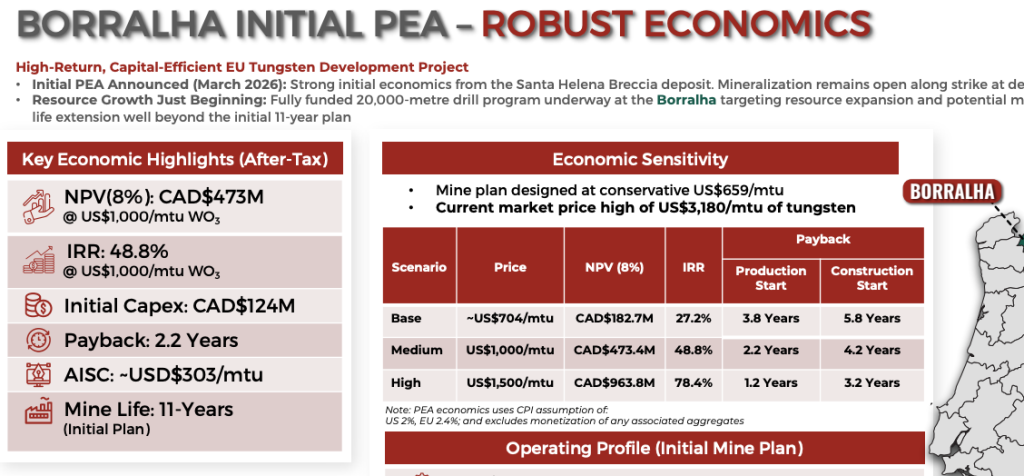

Importantly, even if the tungsten price were to fall 50%, we still have a very robust post-tax NPV, IRR & payback period. At $1,500/mtu, post-tax NPV would be C$963M, IRR +78% and payback period just 1.2 years. Perhaps more important, upfront cap-ex is only C$124M.

Some readers don’t know Portugal and will default to worrying about social license to operate and slow permitting. What are mitigating factors to those concerns?

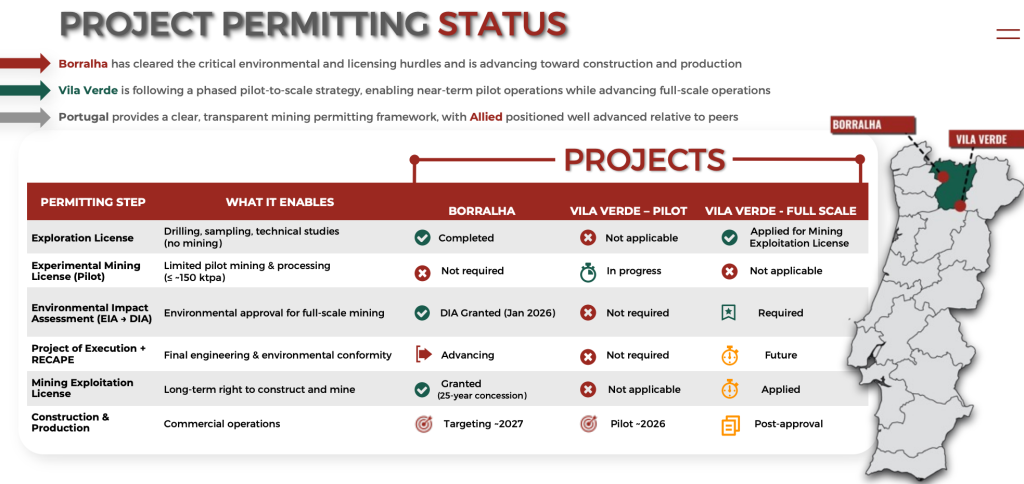

Yes a key concern of investors in the past was slow permitting. However, so far permitting in our region of Portugal has been easier than places like B.C. Canada, or many U.S. states. In January, we received our Environmental Impact Declaration (DIA), clearing a major permitting hurdle and enabling progression into detailed engineering & development.

Our flagship Borralha project is methodically advancing through Portugal’s mine licensing pathway under the Directorate-General for Energy and Geology (DGEG) and the Portuguese Environment Agency (APA). While there’s always risk of delays, we’re in a known, past-producing mining district, not a major tourist area. As you mentioned, there’s an urgency to develop long-term non-Chinese sources of tungsten.

Europe urgently wants more military metals, (NATO countries are upping defense spending to 5% of GDP, a very large increase) especially tungsten, and the U.S clearly wants tungsten as well. If Portugal could contribute valuable tungsten, that would contribute towards its 5% of GDP pledge.

Regarding social license to operate, again we’re in a past-producing mining district. Mining is in the cultural heritage of the entire region, everyone knows family & friends employed in the past, or currently, by mining companies. We are proactively sharing economic benefits (jobs, training, taxes, infrastructure buildouts, etc.)

Without naming names, what challenges do peer tungsten juniors face compared to Allied Critical’s prospects?

Good question. Look, outside of China there are a handful (but not dozens) of strong projects. Simply put, the problem is many are in highly remote parts of good countries like Canada & Australia, or in places that Western countries cannot reasonably rely upon like Kazakhstan. Also, many peers are 6-10 years from production.

Some of the projects around the world are not nearly as large as ours, and some do not offer pure-play tungsten leverage. Finally, not every project has local community support. That’s why we believe Allied Critical Metals has world-class, near-term, tungsten potential.

Please tell readers about your projects, what makes them stand out?

Borralha was historically the largest tungsten mine in Portugal. It’s just about an hour drive on a three-lane paved highway from the deep water port of Porto, is near an international airport, ~30 minutes from Portugal’s third largest city, and ~2.5 km from the largest electrical dam system in Portugal, (no oil/gas/diesel price concerns once up and running).

Not only is Borralha a large and growing resource, it’s high grade, and has wide intercepts, some in the 100s of meters. In January we received environmental permits, a huge de-risking event, and in March we delivered a robust PEA. Drilling this year could double the size of our already large resource.

Several generations in surrounding communities grew up mining tungsten at Borralha. We get calls daily from heavy equipment operators, electricians, skilled trades people who want to work in the mine when reopens. We have social license to operate, which is not always the case around the world.

We’re moving forward rapidly, but prudently. We hope to have small-scale pilot mining underway next year at our second project, Vila Verde, host of the historic Vale das Gatas mine (3rd largest tungsten producer in Portugal). It has 4–5 million tonnes of high-grade surface tailings/waste.

With a small plant costing under $10 million, we could be in production within 6-9 months after financing is arranged, possibly generating ~$40 million/yr. in revenue at current prices.Vila Verde is just 30–40 minutes from Borralha, so it shares the same world-class infrastructure.

Thank you Roy for your insightful comments. It seems the tungsten price outside of China is likely to remain very strong, even if it pulls back moderately (it has pulled back quite modestly). I look forward to more news on small-scale production starting in the next 6-9 months and the prospects for a much larger resource at Borralha.

Disclaimers

Allied Critical Metals is not a current or former client of Epstein Research [ER], and the Company did not pay for this CEO interview. Mr. Epstein of [ER] owns shares in the Company, acquired in the open market. Allied Critical Metals is a highly speculative junior mining company. Readers should do careful due diligence, in conjunction with trusted financial advisors, above and beyond reading the above commentary.

Comments

Log in or sign up to join the conversation.