Depending on your time horizon, you can have some really different perspectives on Facebook (FB) stock and its performance. The social network is down by nearly 20% from its historical highs on February 5, so returns look quite dismal in the short term.

However, in spite of this sharp pullback over the past several weeks, Facebook is still up by 9% in the past year. Even more impressive, from a long-term perspective Facebook has gained over 490% in the past five years.

The main question for investors would be: Is the current pullback in Facebook an opportunity to buy a fundamentally solid business for discounted price or is the Cambridge Analytical scandal the beginning of the end for the company and its stock?

The Most Important Thing

First and foremost, we need to consider how the Cambridge Analytica scandal is affecting the user base and Facebook’s relationship with advertisers. This is clearly the most important variable in terms of evaluating Facebook’s ability to continue generating solid revenues and cash flows for investors over the long term.

It looks like the “Delete Facebook” campaign made a lot of noise among a small group of high profile people with very vocal positions on the matter. Traditional media outlets also gave a lot of coverage to the campaign, which needs to be interpreted in its due context. Facebook is taking away a lot of user attention and advertising money from traditional media companies, so it’s no surprise at all to see many traditional media companies hitting Facebook as hard as they can and even promoting the Delete Facebook campaign.

However, the data is indicating that most users are not deleting their Facebook account or reducing their engagement levels with the company’s different platforms. Even if many users are angry at Facebook because of the Cambridge Analytica scandal, deleting your Facebook account is actually more problematic than it seems to be.

For example, many dating apps require users to have a Facebook account. Besides, many users log into multiple apps through their Facebook account, so deleting Facebook would mean that they have to create new accounts to log into apps such as Spotify (NYSE:SPOT) and Airbnb (Private:AIRB), among many others. It’s not just about the time and annoyance required to create new accounts, but you could lose access to important content and information saved in your original accounts.

For many people, even those who don't use their Facebook account much, the platform allows them to remain in touch with family members, friends, and colleagues across different areas and social circles in their life. If you delete your Facebook account maybe you won't find out that your friend just had a new baby, or you won't receive an invitation to a birthday party because those invitations were sent via Facebook.

Regardless of the reasons, the fact remains that Facebook is not losing many accounts after the Cambridge Analytica scandal. Facebook, Messenger, Instagram, and WhatsApp remain among the most downloaded apps in both Android and iOS as of the time of this writing. Offering a similar perspective, here is the data from a Deutsche Bank Markets Research survey, as quoted by Barron's.

“The investment bank found only 1% of 500 users surveyed deleted the social network in the last week following news that data from tens of millions of its users were harvested by consultant firm Cambridge Analytica.”

Advertisers need to go where the users are. If users are not leaving Facebook, then advertisers will continue allocating their money to Facebook as long as the platform continues delivering a high return on investment.

According to data from Pathmatics, among the top 1,000 ad spenders on Facebook, only seven ceased buying ads on the platform after Cambridge Analytica. In the words of Pathmatics CEO Gabe Gottlieb, as quoted by AdAge:

"This speaks to how important Facebook is as an advertising channel, and that brands are surely making the decision that the benefits of the platform outweigh the smaller risks of brand damage due to association with it. Furthermore, Facebook's advertiser ecosystem is very diverse, so only the largest spenders like P&G or Amazon could potentially impact its bottom line."

This data is consistent with recent comments from Mark Zuckerberg on a conference call with the media. According to the Facebook CEO there is "no meaningful impact" on users or advertisers from the Delete Facebook movement.

Facebook’s reputation has been certainly affected by the Cambridge Analytical scandal, and the company will need to work hard in order to guarantee both users and advertisers that something like that will never happen again. However, the data indicates that the damage is quite small, almost negligible, in terms of its impact on users and advertisers.

Regulatory Risk

Regulatory risk is still an uncertainty factor weighting on Facebook stock, as the company is being closely scrutinized both in the U.S. and in Europe. Zuckerberg will reportedly testify before the House Energy and Commerce Committee on April 10, and it will be important to watch how things go for Zuckerberg in Congress.

Regulatory authorities could potentially require measures such as more ad transparency reporting or data privacy protections, among many other possibilities. These measures could cost Facebook considerable sums of money, and they could also hurt the company’s ability to launch new products and generate revenue from its user base. This is an important risk factor to consider.

On the other hand, regulation usually reduces competitive pressure in an industry, and it favors a market leader such as Facebook. The company has enough money and human resources to comply with all kinds of heavy regulations, but those regulations would be far more problematic for a small startup trying to gain some ground in social media. Too much regulation could be a heavy burden on potential Facebook competitors, and that would hurt those companies in their ability to get funding from venture capitalists.

Facebook already is making moves in terms reducing the information it shares with third parties, and the company will probably need to invest massive amounts of money on data security, since it really can't afford another misstep in this area.

But at the same time Facebook is implementing machine learning and artificial intelligence technologies which can make its data much more strategically valuable and profitable for advertisers. In addition, emerging technologies such as augmented reality and virtual reality should provide plenty of opportunities for Facebook to generate more value to both users and advertisers over the years ahead.

It’s still too early to tell how the regulatory landscape will evolve, and what kind of impact it could have on Facebook’s business. Zuckerberg’s Congressional testimony could obviously be very important in this regard.

That being acknowledged, the most likely scenario is that increasing regulation will not significantly impair Facebook’s ability to continue generating growing revenues and cash flows for investors in the years ahead.

Strong Fundamentals And Reasonable Valuation

Facebook is quite a strong growth business with exceptional profitability levels. The company produced $12.9 billion in revenue during the fourth quarter of 2017, a vigorous increase of 47% year over year.

Operating profit margin amounted to 57% of revenue during the quarter, a material increase vs. 55% of sales in the same quarter a year ago. Due to explosive revenue growth in combination with expanding profitability, operating income increased by 61% year-over-year during the quarter.

Image source: Facebook.

It's hard to argue against the fact that Facebook is a fundamentally sound business in terms of financial performance, and the stock is not excessively priced for such a high-quality company.

Wall Street analysts are on average expecting Facebook to make $8.78 in earnings per share during 2019. Under that assumption, the company is trading at an inexpensive forward price to earnings ratio around 18.2.

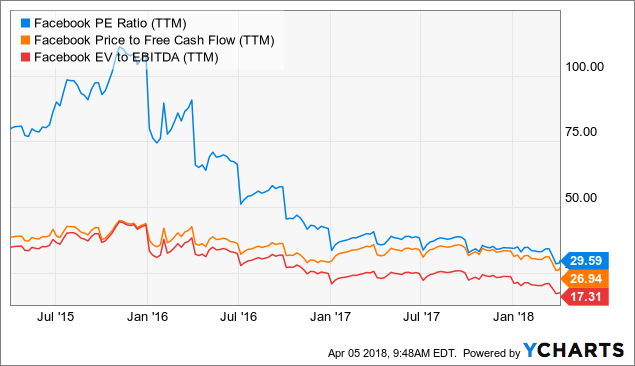

Offering a similar perspective, the chart below shows the evolution of multiple valuation ratios such as price to earnings, price to free cash flow, and enterprise value to EBITDA over the past three years. The three indicators look quite compelling in comparison to the company's valuation levels over the middle term.

FB PE Ratio (TTM) data by YCharts

The most likely scenario is that the Cambridge Analytical scandal will not inflict much permanent damage on Facebook's business. Looking at the main numbers, the business is exceptionally profitable, and valuation is opportunistically low.

For investors who can handle the short-term volatility, the pullback in Facebook stock looks like a buying opportunity over the long term.

Comments

Log in or sign up to join the conversation.