Image: Shutterstock

Key Takeaways

Bristol Myers shares rose 10.1% in the year so far, beating both the industry and the S&P 500 on strong Q4 results.

The company's Growth Portfolio drove ~55% of 2025 revenues, led by Opdivo and newer drugs like Camzyos.

Bristol Myers faces 12%-16% legacy portfolio decline in 2026 due to generics despite Eliquis growth.

Bristol Myers Squibb (Free Report) has delivered a strong performance year-to-date, with its shares gaining 10.2% compared with the industry’s growth of 1.6%. This biotech giant has outperformed both the sector and the S&P 500.

Its sustained rally has helped restore confidence among previously cautious investors, who now appear more assured of the company’s ability to navigate generic erosion of its legacy products.

Bristol Myers Outperforms Industry, Sector & S&P 500 Index

Image Source: Zacks Investment Research

Against this backdrop, let's examine Bristol Myers' fundamentals to assess whether the stock makes for a prudent investment opportunity.

Bristol Myers' Growth Portfolio Drives Sustainable Top-Line Expansion

Bristol Myers’ Growth Portfolio continues to anchor its top-line trajectory, comprising key drugs like Opdivo, Opdivo Qvantig, Orencia, Yervoy, Reblozyl, Camzyos, Breyanzi, Opdualag, Zeposia, Abecma, Sotyktu, Krazati and Cobenfy. This portfolio accounted for approximately 55% of total revenues in 2025, underscoring its central role in the company’s growth strategy.

Growth is primarily driven by the immuno-oncology (IO) franchise, complemented by strong momentum from newer assets, such as Camzyos, Breyanzi, and Reblozyl. Opdivo remains the leading revenue contributor, supported by continued label expansions and sustained share gains in first-line non-small cell lung cancer.

The launch of Opdivo Qvantig, a subcutaneous formulation, further strengthens the IO platform, with early uptake in the U.S. tracking well across approved tumor types. Opdualag continues to deliver robust growth, particularly in the United States, where it has become a standard-of-care option in first-line melanoma.

Reblozyl, developed in partnership with Merck & Co (Free Report), has surpassed $2 billion in annualized sales, benefiting from strong adoption across both first- and second-line MDS-associated anemia. Breyanzi has also crossed a $1 billion run rate, reflecting solid uptake in large B-cell lymphoma and incremental contributions from label expansions, with further growth anticipated in 2026.

Camzyos continues to perform well, driven by robust demand in its cardiovascular indication. Cobenfy has delivered an encouraging launch, generating $155 million in 2025 sales as access expands and adoption deepens across both community and hospital settings.

As the first novel pharmacological approach to schizophrenia in decades, Cobenfy represents a potentially meaningful long-term growth driver, with further upside expected from future label expansion opportunities.

Overall, the scale and momentum of these therapies reinforce the durability of Bristol Myers’ top-line growth trajectory.

Bristol Myers' Legacy Portfolio Grapples With Generic Headwinds

Bristol Myers' legacy portfolio continues to face structural headwinds from generic competition, particularly affecting key products such as Revlimid, Pomalyst, Sprycel, and Abraxane, resulting in a 15% revenue decline in 2025.

The segment — which includes Eliquis, co-developed with Pfizer (Free Report) — generated 45% of total 2025 revenues ($48.2 billion). While Eliquis continues to demonstrate solid demand growth, this has been partially offset by broader generic pressures and higher U.S. government rebates.

Looking ahead, management guides for a 12%-16% decline in the legacy portfolio in 2026, reflecting ongoing patent expiries and pricing headwinds. In contrast, Eliquis is expected to deliver 10%-15% growth, supported by strong global demand, helping partially mitigate the overall segment decline.

Policy-driven changes introduce incremental pressure on net pricing and margins. Under a new U.S. agreement effective Jan. 1, 2026, Eliquis will be supplied at no cost to Medicaid, alongside API donations to support supply-chain resilience. Several other products, including Sotyktu, Zeposia, and Orencia SC, will be offered at significant discounts to eligible cash-paying patients.

Bristol Myers' Pipeline Underscores Growth Potential

Bristol Myers boasts a deep and promising pipeline. Key pipeline candidates with multi-billion-dollar potential are milvexian (Oral factor XIa inhibitor), admilparant (LPA1 antagonist) pumitamig (PD-L1 x VEGF-A bispecific antibody) and iberdomide & mezigdomide (oral CELMoD protein degraders).

In 2026, the company expects to report top-line registrational data for six candidates – milvexian in both atrial fibrillation and secondary stroke prevention, admilparant in idiopathic pulmonary fibrosis, iberdomide in relapsed or refractory multiple myeloma, mezigdomide and arlo-cel in relapsed or refractory multiple myeloma and RYZ101 in second-line plus GEPNETs.

The company recently announced positive interim results from the late-stage SUCCESSOR-2 study, evaluating the efficacy and safety of mezigdomide in combination with carfilzomib and dexamethasone (MeziKd) versus carfilzomib and dexamethasone (Kd) in patients with relapsed or refractory multiple myeloma (RRMM).

The results mark an important milestone for the company’s next-generation CELMoD program. SUCCESSOR-2 represents the first positive phase III study for mezigdomide and the second successful phase III study for Bristol Myers’ CELMoD program, reinforcing confidence in the company’s targeted protein degradation platform.

Bristol Myers also continues to pursue strategic acquisitions and collaborations to expand its pipeline. The recent acquisition of Orbital Therapeutics adds OTX-201, a preclinical RNA CAR-T therapy designed to reprogram cells in vivo for autoimmune diseases, along with Orbital’s RNA platform.

In 2025, Bristol Myers partnered with BioNTech to co-develop the bispecific antibody pumitamig (BNT327) for solid tumors. Early phase II data in triple-negative breast cancer showed encouraging antitumor activity and manageable safety with chemotherapy. Pumitamig targets PD-L1 and VEGF-A, a dual pathway seen as a promising oncology approach.

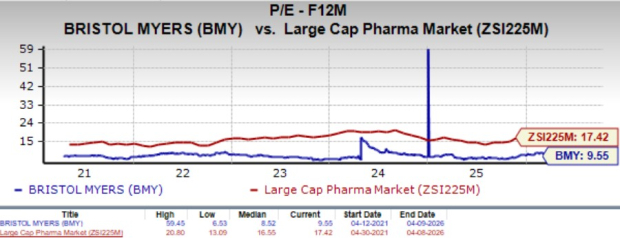

Bristol Myers' Valuation & Estimate Revision

Going by the price/earnings ratio, Bristol Myers appears inexpensive at the moment. Shares have been trading at 9.55x forward earnings, higher than its mean of 8.52x but lower than the large-cap pharma industry’s 17.42x.

Image Source: Zacks Investment Research

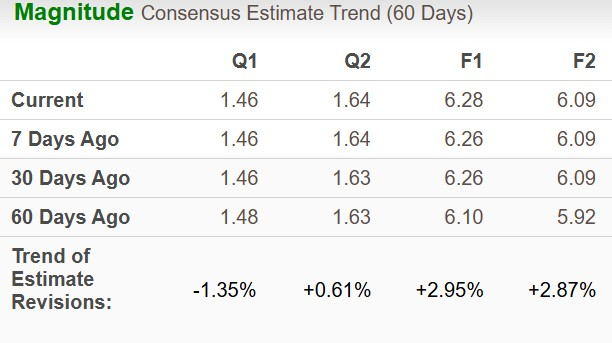

The Zacks Consensus Estimate for 2026 EPS has moved north to $6.28 from $6.10 in the past 60 days, while that for 2027 has gone up to $6.09 from $5.92.

Image Source: Zacks Investment Research

Stay Invested in Bristol Myers Stock

Bristol Myers' growth brands, including Opdivo, Opdualag, Reblozyl, Breyanzi and Camzyos, are increasingly offsetting generic-driven erosion in the legacy portfolio. Potential new drug approvals and label expansions for existing assets are expected to further diversify revenue streams, while upcoming pipeline readouts could serve as meaningful near-term catalysts, enhancing the portfolio’s long-term growth trajectory.

The company is also making steady progress on its cost optimization program, targeting $2 billion in annualized savings by 2027, with approximately $1 billion already realized in 2025. This positions operating expenses to trend lower, supporting margin expansion beginning in 2026.

That said, near-term performance remains constrained by ongoing generic headwinds, with 2026 revenue guidance of $46.0-$47.5 billion, down from $48.2 billion in 2025.

Given this backdrop, a cautious stance appears warranted. New investors may consider a wait-and-watch approach for more attractive entry points, while existing shareholders could continue to hold positions, supported by a dividend yield of approximately 4.3%.

Bristol Myers currently carries a Zacks Rank #3 (Hold) rating.

Comments

Log in or sign up to join the conversation.