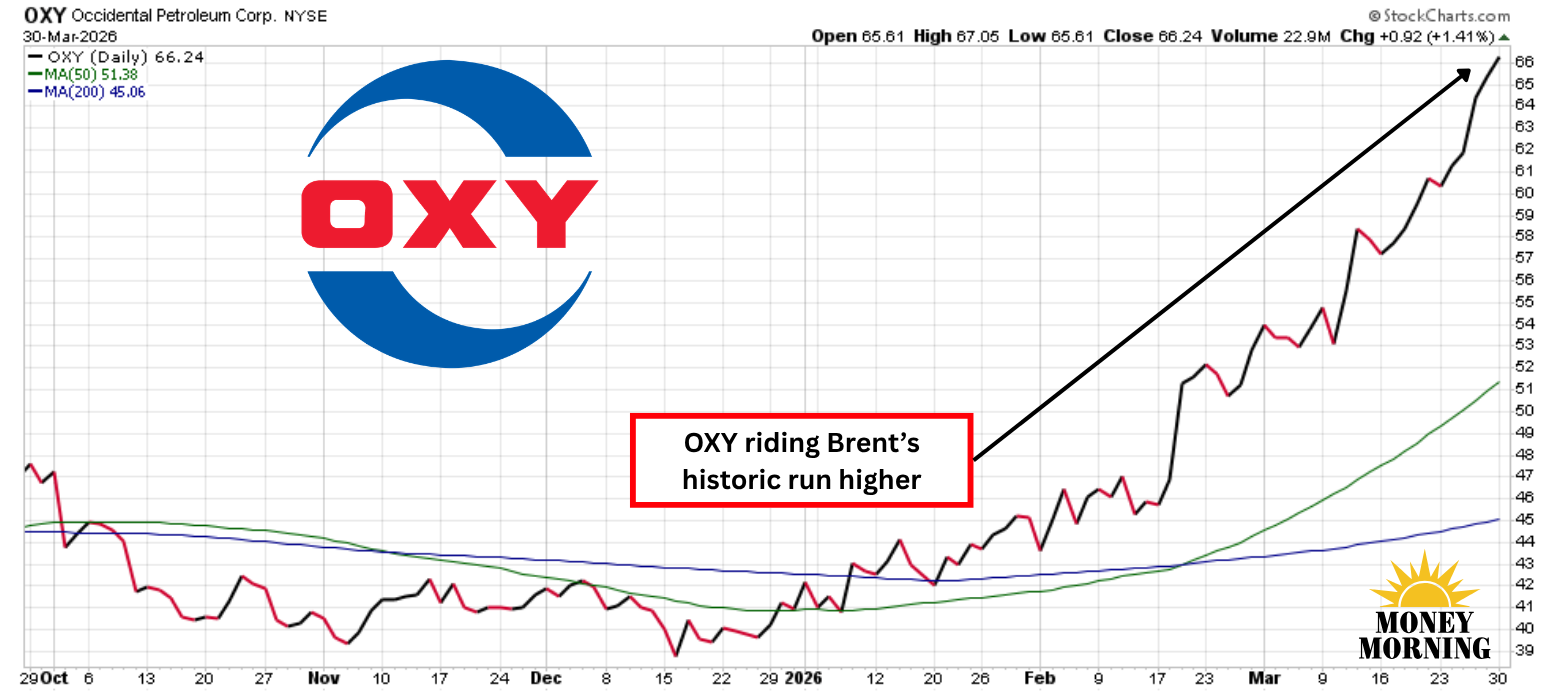

Brent crude delivered its largest monthly gain on record in March 2026. The benchmark climbed 58% from roughly $72.48 per barrel at the end of February to close near $113. Disruptions in the Strait of Hormuz tied to the Iran conflict drove the surge. Investors now ask, which energy name turns this price spike into the strongest cash-flow gains?

Why Buffett's Stake Signals Confidence in OXY's Setup

Warren Buffett's Berkshire Hathaway (BRK-A) (BRK-A, BRK-B) owns approximately 27% of Occidental Petroleum (OXY), with 265 million shares valued around $17.5 billion as of recent filings. Berkshire also completed the $9.7 billion purchase of OXY's OxyChem chemicals unit in January. That transaction let Occidental cut principal debt by $5.8 billion to $15 billion.

OXY runs as a focused upstream producer, heavy in the low-cost Permian Basin. It carried no active commodity hedges on production. This structure channels higher Brent and WTI prices straight to margins. Every $1 per barrel increase in realized prices adds roughly $240 million in pre-tax cash flow annually.

OXY's Numbers Deliver Clear Leverage at $110+ Oil

OXY reported record full-year 2025 production of 1.434 million barrels of oil equivalent per day (Mboed) and 1.481 Mboed in Q4 – above the high end of guidance. It generated $2.6 billion in operating cash flow and approximately $1 billion in free cash flow before working capital that quarter alone. For 2026, the company guides 1.45 Mboed output with capital spending trimmed to $5.5 billion to $5.9 billion, freeing resources for further debt reduction and returns.

The quarterly dividend rose more than 8% to $0.26 per share. That marks the fifth consecutive annual increase and doubles the payout over four years. OXY's wells maintain breakeven costs well below $50 per barrel in core areas, so current prices above $110 expand margins sharply.

OXY: Forward P/E around 20x, dividend yield 1.5-1.6% ($1.04 annualized), 84% U.S. onshore production with zero hedges.

Devon Energy (DVN): Permian exposure but hedges mute price upside; lower cash-flow sensitivity than OXY.

Chevron (CVX): Another Buffett favorite, integrated operations with higher 3.3% yield, yet refining costs offset some crude gains.

ExxonMobil (XOM): Scale and diversification provide stability, but lower percentage upside from pure upstream moves.

OXY shares have risen nearly 58% year-to-date, outpacing most integrated peers amid the oil rally.

Key Takeaway

In short, Occidental Petroleum gives passive income investors the purest exposure to elevated oil prices, backed by Buffett's long-term stake and a hedge-free, low-breakeven model. At a forward P/E near 20x and a growing 1.5%+ yield, it balances upside potential with returning capital.

Comments

Log in or sign up to join the conversation.