Block (SQ) - formerly known as Square - delivered a remarkably strong quarter in Q4. Management is making lots of smart moves and permanently innovating to build a stronger and more powerful ecosystem.

Block is a very dynamic company and management is not afraid to take risks. This strategy can sometimes backfire, but it is also a blueprint of many of the most successful businesses in history.

The current market environment is extremely hostile for high-octane growth stocks. Nevertheless, Block is well-positioned for attractive returns over the years ahead.

The Numbers

Block accounts for the Bitcoin trading business as revenue, but this creates some noise and volatility in the data, and it has minuscule profit margins for the business. For these reasons, gross profit is a more relevant metric to follow than accounting revenue in the particular case of Block.

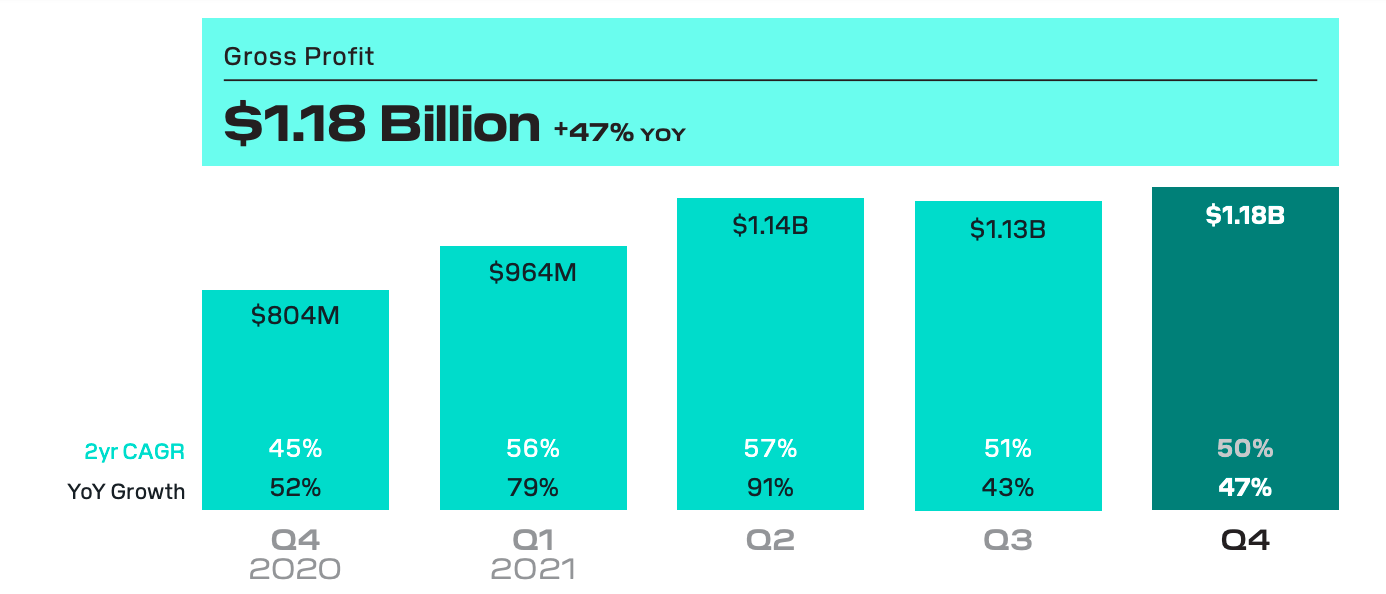

The company reported $1.18 billion in gross profit during Q4: up 47% year over year. Cash App generated $518 million, up 37%. The Square ecosystem produced $657 million in gross profit, up 54% year over year. These are more than healthy growth rates for a company that is facing challenging year-over-year comparisons.

(Click on image to enlarge)

Block

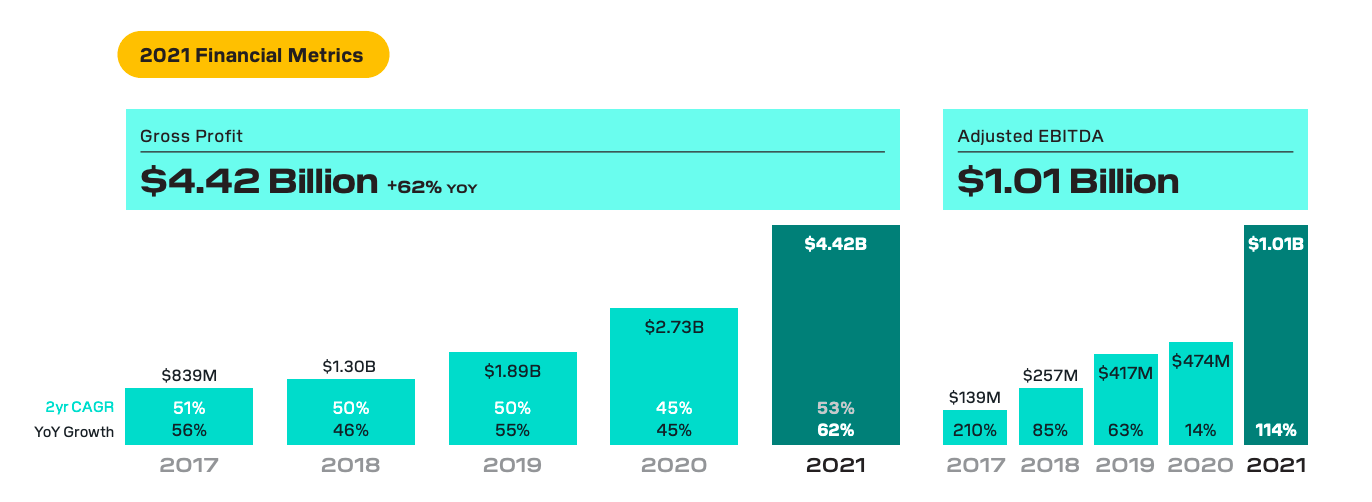

Looking at profitability on an annual basis, Block is above breakeven, but the company is not focused on margins at this stage.

(Click on image to enlarge)

Block

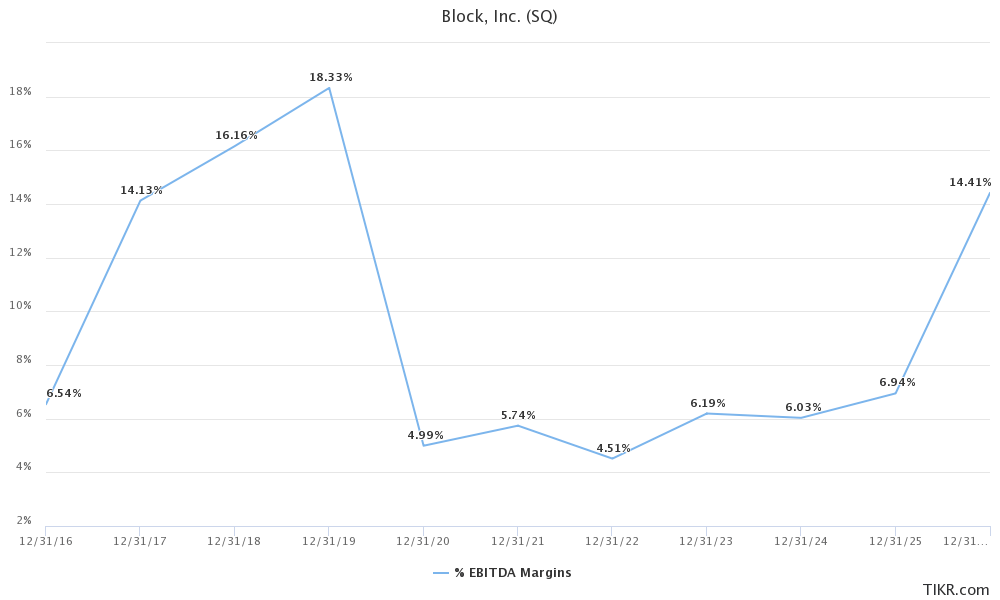

Due to all the active innovations and growth investments, I am expecting Block to continue delivering positive earnings and cash flows, but with small margins on revenues over the next several years.

The chart shows the average EBITDA margin forecasts for SQ among the analysts following the stock. Wall Street is expecting margins to remain positive but thin in the next 3 years, followed by a significant expansion in profitability as the business matures in 2025 and beyond.

(Click on image to enlarge)

TIKR

In the Cash App business, network effects play a crucial role for the company. Users attract other users to the platform when they need to transfer money or split bills. In Q4 Cash App also started offering the functionality of allowing users to send fractional shares of stock and Bitcoin via Cash App to friends and family. This move further strengthens the network effect.

In January, Block introduced Cash App Taxes, where customers can file for free from a phone or computer and can receive their tax refund up to two days early if deposited through Cash App.

Square is now the name of what the company used to call Sellers, and it is basically the platform for small merchants to process payments plus additional software and services related to small businesses management.

The company is working on international expansion in this area, which is still in the very early phase. Block has recently introduced the Square Photo Studio mobile app, which makes it easier for sellers to take high-quality photos and directly sync them to the catalog or online store.

The acquisition of Afterpay was closed in January, and it provides a strong entry into buy now pay later. This can provide value and flexibility for both sellers and customers, and Afterpay can also work as a bridge, a connection between the Square seller ecosystem and Cash App going forward.

Block Stock Looks Undervalued

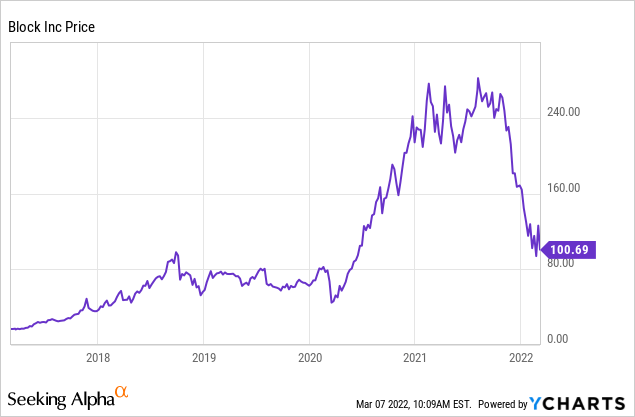

In spite of the sharp post-earnings rally, Block is still trading at levels that are not too far away from values first reached in 2019. I am talking about the stock price, not the valuation ratios.

Data by YCharts

Block has more than doubled the scale of the business since 2019 and it further diversified its product offering into multiple growth drivers. It is very reasonable to say that Block is a much sounder and more valuable business in 2022 than it was in 2019.

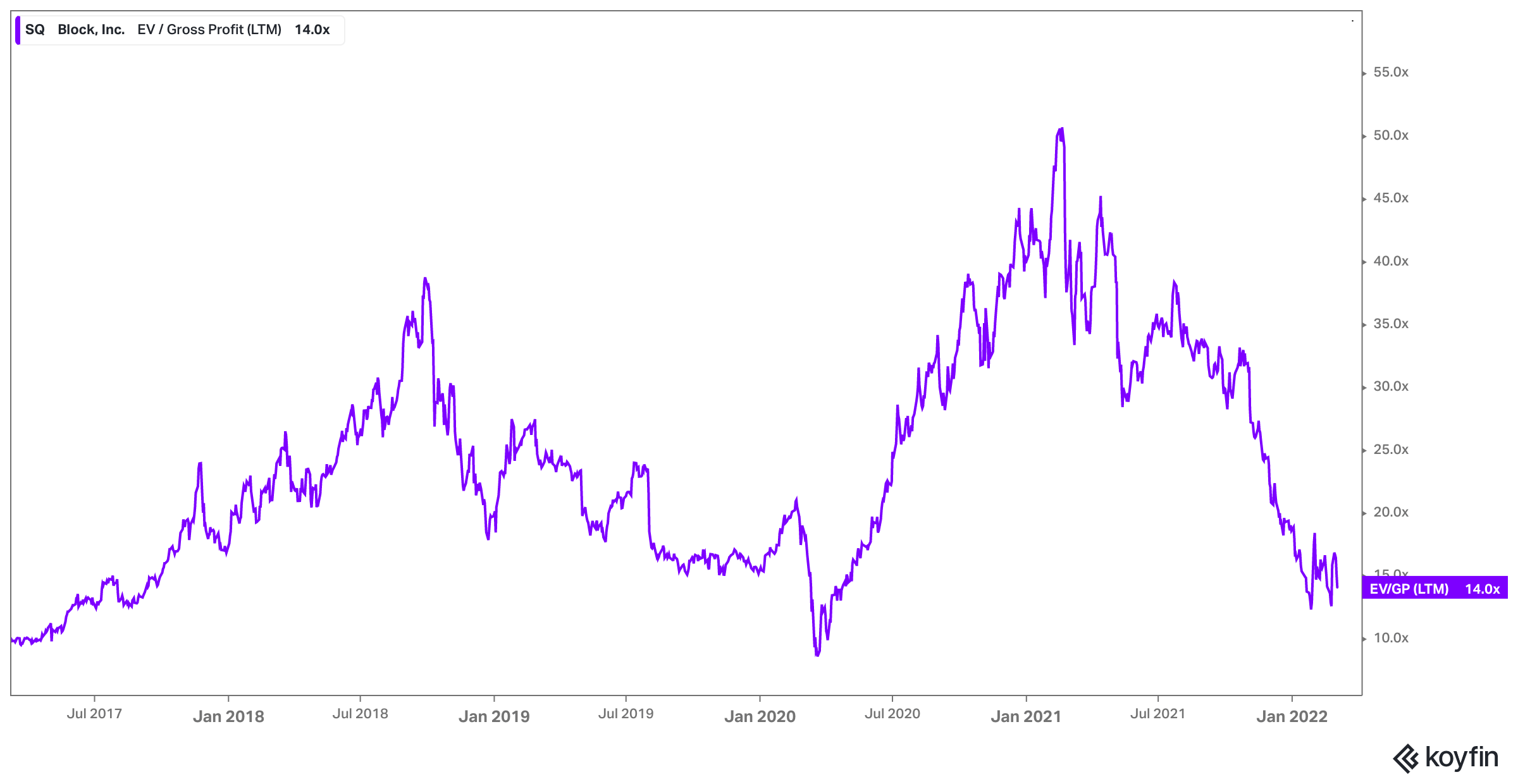

The valuation ratios as expressed by Enterprise Value to Gross Profits are near the lows of the past 5 years. Since 2017, Block has only been so cheap at the lows of the 2020 COVID crash.

The Cash App was a business much smaller at the time, so Block was making most of its money from small merchants that were particularly affected by the lockdowns.

I don't think the current environment is as bad as March 2020 was for the company, especially because Block is now a much stronger and more diversified business.

(Click on image to enlarge)

Koyfin

The Big Picture

Block has a remarkably singular CEO in Jack Dorsey. The man is brilliant, very creative, and has a big passion for design and art, which can be seen in the way that Block designs its elegant and user-friendly products.

In his own words:

Design is not just visual, design is efficiency. Design is making something simple. Design is epic. Design is making it easy for a user to get from point A to point B

It is impossible to read these words and don't think about how Steve Jobs was also deeply focused on design and building a comfortable and simple user experience. Great things can happen at the intersection of art and technology.

That being said, Dorsey can sometimes have too many interests on his mind, he can get into fights with hedge fund managers and he seems to be a Bitcoin maximalist, meaning that he wants Bitcoin to be the currency of the internet, and he may miss some opportunities for Block in other cryptocurrencies.

This happens very often with founders and builders in the tech industry. It is not a reason to stay away from Block on its own, the company is doing great and it has a deep management team. But it is also a factor that cannot be ignored, both for good and for bad.

Even Jamie Dimon - JPMorgan CEO - has praised Block for its innovations, saying that Block has done the things he wishes JPMorgan had done.

In another parallel between JPMorgan and Block, an analyst from Mizuho said in July of 2021 that buying Block now could be like buying JPMorgan in 1871.

Now could be a once in a lifetime opportunity to buy Square stock (SQ) as it transforms into a financial services powerhouse, argues Mizuho analyst Dan Dolev.

We believe Cash App may be en route to becoming the ultimate neo-bank and the money center bank of the future. This could make buying SQ analogous to buying J.P. Morgan in 1871

We obviously have to take these grandiloquent ideas with a huge grain of salt, as there are a lot of risks and things that could go wrong for Block on its way to becoming the ultimate neo-bank.

But it is also important to keep the long-term perspective in mind. Fintech companies as a group will create massive amounts of value for shareholders over the years ahead, and SQ is a leader in that space, just like JPMorgan was a leader in a young and growing industry in 1871.

Competition is very intense in fintech, and competitive pressure will only increase going forward. Square seems to be doing better than PayPal (PYPL) in digital wallets, but we are going to see traditional financial companies, big tech players such as Apple (AAPL), and new fintech entrants putting more pressure on the sector in the near term.

Block has proven that it has the ability to successfully compete over time. It even managed to beat Amazon (AMZN) in 2014 when the online retailer launched its own low-cost product to compete versus Square.

There are two differentiating factors to consider when thinking about competitive strength. First, Square is always innovating and it is hard for the competition to catch up. Second, the whole ecosystem is worth more than the individual parts. Once a company is using Square for payments, invoices, credit, and so forth, it is very inconvenient to replace SQ with another alternative, especially if such alternative is not materially better than SQ.

In Cash App, we have both permanent innovation and the network effect working in the company's favor. In December, there were more than 44 million monthly transacting activities on Cash App, an increase of 22% year over year. Once the network reaches such a scale, the competitive moat becomes quite strong.

Block has a risk-oriented management team, which can be a spectacular growth engine but also carries some risk. From a long-term perspective, competition is always the biggest risk factor to watch, although Block is doing great in that area and consolidating its competitive position.

Looking at the upside potential, the company has massive room for long-term growth, management is executing brilliantly, and the stock is very reasonably priced, if not materially undervalued.

In a risk-off market environment, the stock price can easily remain under pressure until market conditions improve. Over multiple years, on the other hand, Block is well-positioned for attractive returns.

Comments

Log in or sign up to join the conversation.