Earlier last week I did an instablog post walking through why M&A activity was likely to remain robust in the pharma and biotech sectors. I also invited readers to submit their picks of firms within the industry that they thought would make attractive takeout candidates. The column generated a lot of good conversation and numerous ideas were offered up such as Geron (NASDAQ: GERN) in the small cap space as well as mid-cap Isis Pharmaceuticals (NASDAQ: ISIS).

However, it was a follower’s suggestion of a tiny pain and addiction management drug maker

BioDelivery Sciences (NASDAQ: BDSI) that caught my eye. Its unique drug delivery technology that produces a thin film strip that melts in your month to deliver the proper dosage is intriguing. It reminds me of one of the reasons I bought Eagle Pharma (NASDAQ: EGRX) back in mid-December of 2014 before it quintupled this year in that way. Finally, given a standing collaboration and distribution deal it already has in place with a larger player in the industry that is a serial acquirer, it made the most logical near-term buyout target.

Company Overview:

BioDelivery Sciences International is a specialty pharmaceutical company based in Raleigh, North Carolina. The company engages in the development and commercialization of pharmaceutical products principally in the areas of pain management and addiction. The company provides its products based on its patented BioErodible MucoAdhesive (BEMA) drug delivery technology.

The stock has a market capitalization of just over $300 million, enough cash on hand to fund itself through at least mid-2017 and has one approved product on the market and one more on the way. It also has a couple of other products in its pipeline as well as some small but frequent insider buying in 2015. The stock trades at right around $6.00 a share. The equity traded at $18.00 a share earlier in the year.

Product Pipeline:

In the first half of 2014 the FDA approved BUNAVAIL, the company’s first commercialized product. BUNAVAIL is the first mucoadhesive buccal film formulation of buprenorphine to compete directly with Suboxone sublingual film. In 2014, sales of Suboxone sublingual film totalled approximately $1.3 billion in the U.S. while the total market grew to more than $1.7 billion, driven by an 11 percent increase in prescriptions according to data from Symphony Health Solutions. BUNAVAIL has gotten off to a slow rollout but I am optimistic growth will pick up in the near future.

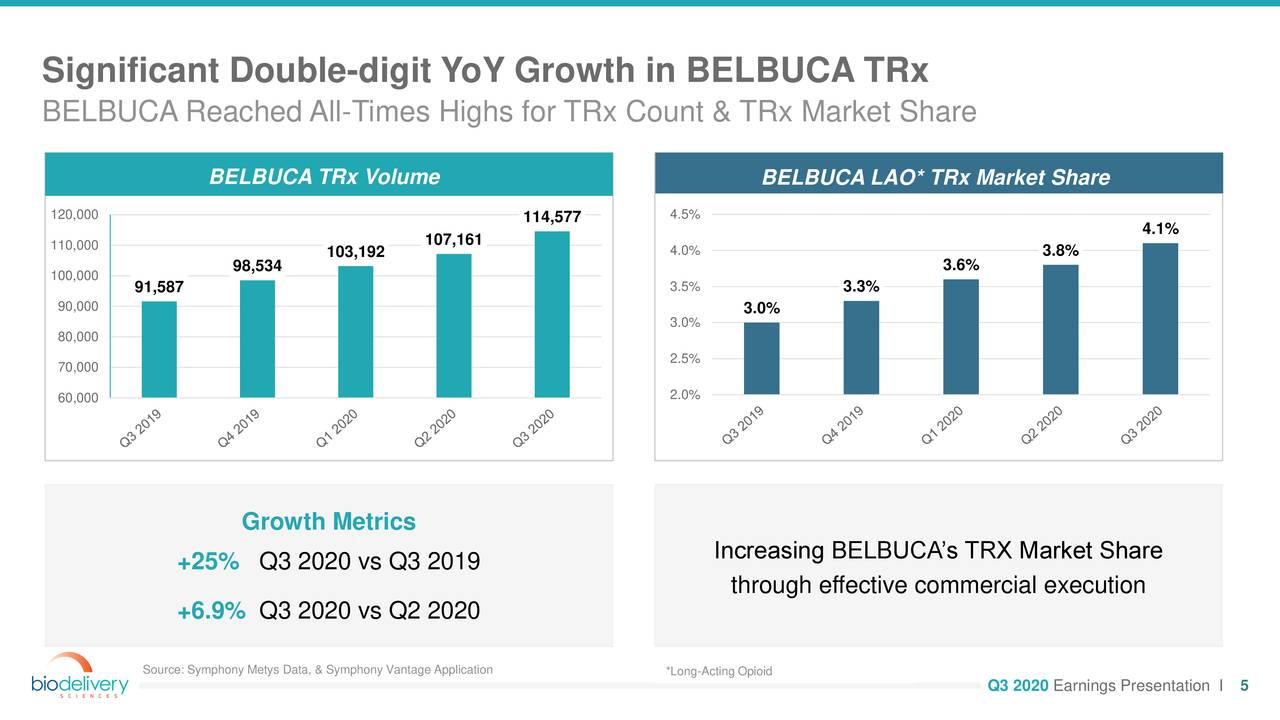

A more important product for BioDelivery is BELBUCA which was approved by the FDA late in October. This pain management drug is a mu-opioid receptor partial agonist and a potent analgesic with a long duration of action that utilizes BDSI’s patented drug delivery technology. Through this delivery technology, buprenorphine is efficiently and conveniently delivered across the buccal mucosa (inside lining of the cheek).Buprenorphine is a semisynthetic opioid derivative of thebaine. It is s mixed partial agonist opioid receptor modulator that is used to treat opioid addiction in higher dosages, to control moderate to acute pain in non-opioid-tolerant individuals in lower dosages and to control moderate chronic pain in even smaller dosages.

BioDelivery’s developmental and marketing partner on this drug is Endo International (NASDAQ: ENDP), an Ireland-based pharmaceutical that has grown using myriad strategic acquisitions and whose market capitalization of over $10 billion dwarfs the size of BioDelivery. It will be responsible for marketing and distribution of BELBUCA.

Here is where it gets interesting. FDA approval triggered a $50 million payout from Endo to BioDelivery. The company is also eligible for four more sales milestone awards potentially totaling $55 million. In addition, BioDelivery Sciences will also receive royalties on the sales of BELBUCA in the mid to high teens.

The analyst estimates I have seen has BELBUCA seeing sales levels of almost $250 million yearly in a few years with peak annual sales of around $500 million. That is quite the little high margin revenue stream to BioDelivery on top of the milestone payments for a company with a market capitalization of just $300 million. It just seems too logical for Endo to just buy BioDelivery as even with a substantial premium, it would end being an accretive acquisition. The company would claw back its milestone payments, keep the royalty payouts to itself and gain access to BioDelivery’s proprietary drug delivery system and pipeline. Just one man’s opinion.

Comments

Log in or sign up to join the conversation.