Snap Inc. (Pending:SNAP), parent company of messaging app Snapchat, plans to make its much anticipated market debut this Thursday (3/2). Snap Inc. expects to raise $3.0 billion through its offer of 200 million shares at a price range of $14 to $16 per share. Of these shares, 28% will be offered by company insiders, and all will be non-voting shares with the founders maintaining majority voting power.

If Snap Inc. prices at the midpoint of its price range, it would command a market cap value of $17.8B and on a fully diluted basis, a market cap of between $21.5B.

Although this price range is lower than the original valuation projected, we strongly feel it is still too expensive given the fundamentals. There are also several red flags that make us nervous about investing including: steep competition, slowing user growth rate, non-voting share structure, and the recent sale of $16.2 million shares by the two co-founders, among others.

SNAP will list on the NYSE under the ticker, "SNAP." Joint bookrunners include: Morgan Stanley, Goldman Sachs, JPMorgan, Deutsche Bank, Barclays, Credit Suisse and Allen & Company. Snap also has over twenty other underwriters working on the deal.

The deal is currently reported to be multiple times oversubscribed, meaning more fund managers want to buy shares in the IPO than are being issued by Snap. This typically signals that the company will open above, or at the high end of its expected price range.

Advertising Market - High Growth, Yet Increasing Competition

The International Data Corporation (IDC) projects worldwide advertising will grow from $652B in 2016 to $767B in 2020, with mobile advertising being the fastest growing segment in advertising. In 2016, $66B was spent on mobile advertising, a number that is expected to grow 3x by 2020. This transition from ad spending on TV and desktop to mobile stands to benefit Snapchat's mobile strategy.

However, at the same time, Snap faces tough competition from Facebook (Nasdaq :FB) (whose subsidiaries include Instagram and WhatsApp), Google (Nasdaq :GOOG) (Nasdaq :GOOGL), and Line (Nasdaq :LN). Facebook in particular has shown itself capable to stealing DAUs from Snap by launching similar features.

Comparing Snap to Earlier US Tech IPOs

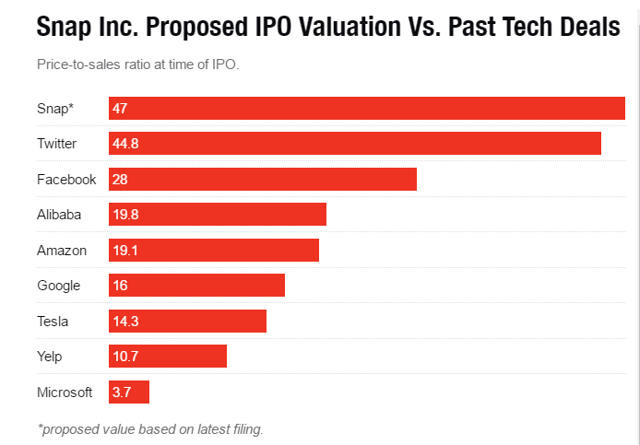

To put Snap's performance in context with some of the big tech IPOs, Fortune compared Snap's projected price to sales ratio to Twitter (NYSE:TWTR), Facebook, Alibaba (NYSE:BABA), and found Snap was more expensive than all of them on a price to sales basis (see chart below).

(Fortune)

Additionally, Snap is growing at a slower rate than both Facebook and Twitter when the two made their market debut. Quarter over quarter growth for Facebook, Twitter, and Snap was 5.7%, 6.9%, and 3.2%, respectively. In terms of DAUs at time of IPO, Facebook had 483M versus Twitter at 100 DAUs, and Snap at 153M DAUs (see below).

Comparison at Time of IPO

| DAUs (in million) | Q/Q Grwth | Date of Data | |

| 483 | 5.7 | December 2011 | |

| 100 | 6.9 | June 2011 | |

| Snap | 153 | 3.2 | December 2016 |

(SEC Filings)

To put Snap's valuation in the context of recent M&A activity, Facebook acquired WhatsApp, a messaging app, in April 2014 for $19B. At the time of the acquisition, WhatsApp had 350M DAUs, almost double compared to the 153M DAUs for Snap.

Use of Proceeds and High Spending

IPO proceeds are necessary for Snap to fund both its near-term cash burn as well as to deliver on its commitments to Google Cloud, Amazon (Nasdaq :AMZN) Web Services, and others. As of December 2016, Snap had 987.3M in cash and cash equivalents, and in just the year 2016, the company reported a net cash outflow of $677.6M. We expect heavy spending to continue in the near term and for the company to continue to report net losses.

Snap has committed to spend $1B with Amazon Web Services and $2B with Google Cloud over the next five years.

Legal Matters

Snap noted in its filing it switched accounting firms from PricewaterhouseCoopers LLP (PwC) to Ernst & Young (E&Y) in April 7, 2016. The decision was made after PwC identified material weaknesses in Snap's internal control over financial reporting. E&Y audited Snap's financial statements for the year 2015 and 2016. The decision to switch accounting firms was approved by the board, but may raise questions to investors on why Snap felt it was necessary to make the switch.

Accelerating Lock-up Period

On Feb 13, Snap announced changes to its lock-up expiration rule to allow employees to sell shares after 150 days (versus 180 days, which was initially listed in its IPO Prospectus). Employees holding standard stock awards are now able to sell shares after 150 days, the same holding period as co-founders and investors.

It is rare that most investors be able to sell shares before employees. Therefore the acceleration of the lock-up expiration for employees now puts them and investors on an equal playing field in terms of their opportunity to offload shares. Employees and investors stand to benefit tremendously from the IPO, and may be motivated to being unloading shares as soon as the lock-up period expires.

Performance of Past IPOs Suggests Holding Off

Reuters looked at the largest 25 technology IPOs both globally and in the US and found that during their first year as public companies, these start-ups tend not to perform very well. Globally, shares of the majority of the 25 largest technology IPOs were below their first day closing price one year later, with the median one-year performance being a decline of 22.3%. And looking at US technology IPOs, 14 of the 25 biggest fell in their first year compared to their IPO price.

Alibaba, Twitter, Groupon (Nasdaq :GRPN), Zynga (Nasdaq :ZNGA), Facebook, and Fitbit (NYSE:FIT), all dropped during their first year as public companies. This research suggests investors may be better off by waiting several months before investing in Snap as opposed to attempting to get in at IPO price.

Conclusion: Watch For Fun, Stay On The Sidelines

We look forward to watching this deal, given the hype, but recommend investors steer clear.

Competition from Facebook, slowing user growth rate, non-voting share structure, and large net losses all make us wary about investing, particularly at the proposed valuation. For us, the risks far outweigh the benefits. For us, Snap is a no-go at its current valuation.

**A Signal For Further IPOs**

Regardless of whether investors view the Snap IPO as a good investment or not, it will be closely watched as a signal to whether the mainly stagnant IPO market will make a rebound in 2017. Depending on how Snap performs, its IPO could encourage other successful startups, like Uber (Private:UBER) and Airbnb (Private:AIRB), to enter the IPO market. Snap's IPO is slated to be the largest US tech IPO since Facebook went public in 2012.

Comments

Log in or sign up to join the conversation.