There are a lot of things we don’t know about Russia’s attempt to invade Ukraine, but there are also some things we do know.

Mr. Putin’s gamble, and the West’s response, has brought into view one of the few existential tail risks that isn’t a Black Swan, which is to say, it is a known unknown: The risk of an escalation into war between Russia and NATO, and the exchange of nuclear weaponry. The continued call on NATO from Ukraine President Volodymyr Zelensky to impose a no-fly zone his country is an alarming case in point.

I have no idea how to quantify such a risk, and it is fair to assume that markets don’t either, at least not with any accuracy. BCA’s suggestion that you might as well be long stocks on a 12-month basis, even if you think an ICBM is headed your way is probably a fair reflection of the level of analysis you can expect from your favorite sell-side researcher. Take everything you read with a heap of salt

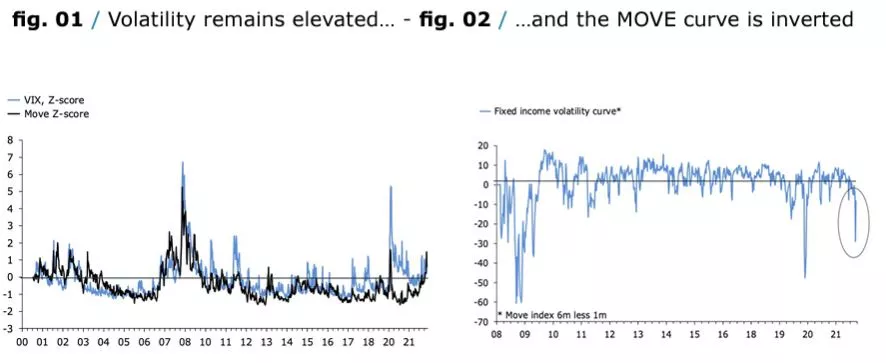

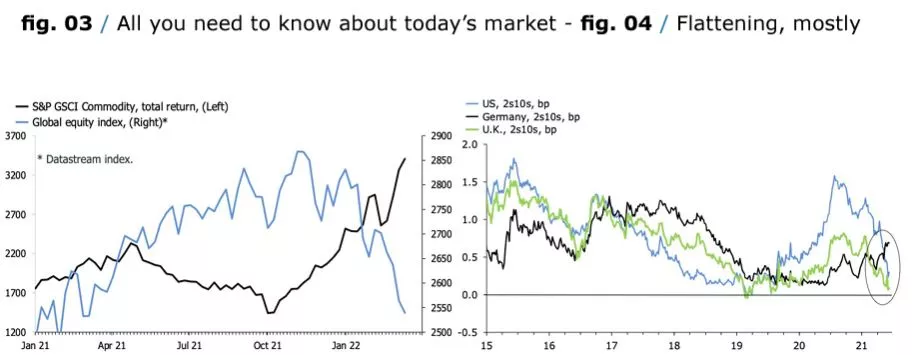

We also know that the war between Ukraine and Russia has cemented a trend that financial markets aren’t too happy about. Chris Wood, a strategist writing for Jeffries, calls it “goldilocks inverted”, or more colloquially; stagflation. The change in conditions on the ground are easily identified; rates and volatility are rising and equities and credit are suffering. Yield curves, by contrast, remain mixed. 2s10s in the US and the UK are flattening—the latter is within touching distance of inversion— while the curve in Germany is still steepening. Commodities and energy equities, not surprisingly, are rallying.

In a goldilocks world, central banks have the luxury of running loose monetary policy—chiefly via asset purchases and negative real interest rates— without having to worry about inflation, let alone reaching their targets. That reality now faces, well…a reality check. Markets have, until recently, been limit-long the idea that central banks would never reach their targets, and that if they did, they would conjure up a reason—average inflation targeting etc—to keep easing.

The stimulus-fueled mismatch between supply and demand after COVID has pushed this assumption to the edge, and the war in Ukraine could well be the camel that breaks the camel’s back. This is an asymmetric stagflationary shock; the near-term boost to inflation is certain and uncomfortable, but it remains unclear whether households will stop going to shops or restaurants, especially considering the likelihood of fiscal support, in the manner observed during COVID.

It’s possible that the war in Ukraine eventually knocks growth to such an extent, via inflation driven demand destruction, as to bring both monetary and fiscal stimulus back on the table. That wouldn’t be too bad, for markets. There is nothing like a negative shock to keep central banks focused on keeping the punchbowl full. For now, however, policymakers are forced to focus on inflation, even as the butcher’s bill in Ukraine rises to depressing heights. Are you not entertained?

Russia's Terrible Gamble

Finally, for all the things that we don’t know about the impact of Russia’s invasion in Ukraine, permit me some thoughts. I agree with the initial analysis by Jeremy Cliff that Russia’s invasion “changes everything”, as well as former German foreign minister Joschka Fisher’s point that that Russia’s invasion ”is showing a brazen disregard for international treaties and the law of nations.” An argument often made is that this is a crisis of the West’s own making for too aggressively expanding western institutions, the EU and NATO, without regard for Russia’s security interests. This sounds reasonable over a few pints at the pub. But the counterfactual is difficult to justify in my view. It is effectively the argument that Russia would have been more friendly to the West if we had just allowed it to impose its will, and territorial ambitions, on former Soviet economies in the first place. That’s possible, but far from certain in my view.

It is also the argument that the West should not stand up to the likes of Ukraine out of fear of Russian aggression. But this is in effect ensures that Russia can, in the first place, unilaterally decide what it wants to do with former Soviet countries, if anything. That, in particular, seems wrong to me. The difference between allegiance to the Western part of Europe and the East is the difference between Slovenia, with a GDP per capita of $25K, and Belarus, with a GDP per capita of just over $6K. It is not surprise that the long arc of history has bent in such a way as to push former Soviet Eastern European countries into the arms of the West. It seems reasonable that Mr. Putin should think about why this is, though judging by his reasons for the assault on Ukraine, he is way past such considerations at this point.

By contrast, the west does have some responsibility of what happens next, or at least, it has agency. It warms my blue and gold-starred heart to see Europe finally rising to the challenge in moments of crisis. COVID strengthened the fiscal integration in the EU, and Mr. Putin’s war in Ukraine has similarly galvanized Europe’s joint sense of urgency on defense/ security and energy, two areas where EU countries’ objectives invariably overlap, even if outright interests sometimes vary.

Yet, I can’t be the only one struck by the grim irony of European leaders meeting in Versailles to agree on an extended sanctions list, and the swift accession of Ukraine, and perhaps even Moldova and Georgia, into the EU. Is there any version of this misery that does not end with war with between the West and Russia 5-to-10 years down the line?

I ask this question knowing full well that the west doesn’t have a choice. The barrage of economic sanctions—which could well end up driving Russia to default on its USD debt—was the only thing we could do, absent a conventional military intervention.

At some point, however, we have to ask when the screw will stop turning, and the risk if it continues to do so. This decision, of course, is linked to the military contest itself. We have to assume that the balance of power eventually will force one of the fighting parties to seek a deal. It will be interesting to see whether the West at some point applies pressure on Ukraine to accept a ceasefire, even if such a deal means a carve-up of the country, and no NATO membership.

The situation leaves me with two emotions. First, anger that a European country is now being destroyed. Even in the best possible outcome, Ukraine’s infrastructure and major cities will be ruined. This, incidentally, is the second time in recent memory that Mr. Putin’s war machine is laying waste to an otherwise reasonably well functioning civil society. The first, of course, was Syria, at the behest of Assad. Shame on him.

Secondly, however, I can’t help but feel that the West, Europe in particular, is running from one extreme to the other in its triumphant “cancellation” of Russia. Former German Chancellor Angela Merkel’s adherence to “Putinversteher” is now being cast as a hopelessly naïve strategy, epitomized by the recent announcement by new Chancellor Olaf Scholz that Germany will now spend 2% of GDP on defense, adding a €100B in an immediate injection, for good measure. Other countries, primarily in Scandinavia, have followed with similar announcements. In short, if Mr. Putin want’s a tussle with Europe, Europeans are now getting ready for it.

An increase in European defense spending was long overdue, if only for the political signal this sends to the rest of the world about the region’s desire for autonomy. I can’t help but feel, though, that you need both Putinversteher and more defense spending to enjoy a stable relationship with Russia. After all, Russia is, geographically speaking, a European country, and if you buy gas from Mr. Putin, or whoever else is in charge, there is a smaller risk that you end up in a conventional military, let alone nuclear, exchange.

The problem is that such a position does not help the likes of Ukraine to whom the West has a responsibility. If they want to be part of our sphere, they should be welcomed, perhaps even if it means war.

Comments

Log in or sign up to join the conversation.