Image: Bigstock

Applied Materials (AMAT - Free Report) has been one of the hottest stocks in the tech sector, climbing to fresh all-time highs of $739 a share in Tuesday’s trading session, and has now rallied nearly 200% year to date.

The rally reflects growing investor confidence that the artificial intelligence (AI) infrastructure boom is still in its early innings, positioning Applied Materials as one of the biggest beneficiaries of rising chip manufacturing spending.

But after such a powerful run, investors are asking the obvious question: Is there still room for AMAT stock to move higher, or has the good news already been priced in?

Image Source: Zacks Investment Research

Why Applied Materials Stock Is Surging

Several catalysts have fueled Applied Materials' recent surge.

Perhaps the biggest driver has been renewed optimism surrounding AI-related semiconductor spending. Strong earnings and bullish outlooks from memory chip giant Micron Technology (MU - Free Report) and chipmaker Qualcomm (QCOM - Free Report) have reinforced expectations that hyperscalers and semiconductor manufacturers will continue investing aggressively in AI infrastructure.

That spending ultimately flows to semiconductor equipment suppliers like Applied Materials, which provides the tools needed to manufacture advanced chips.

Analysts have become increasingly bullish on the company, with multiple Wall Street firms recently raising their price targets for AMAT after management highlighted accelerating demand for leading-edge logic, Dynamic Random Access Memory (DRAM), and advanced packaging equipment.

To that point, some analysts believe wafer fabrication equipment spending could remain elevated for years to come as AI adoption expands across various industries.

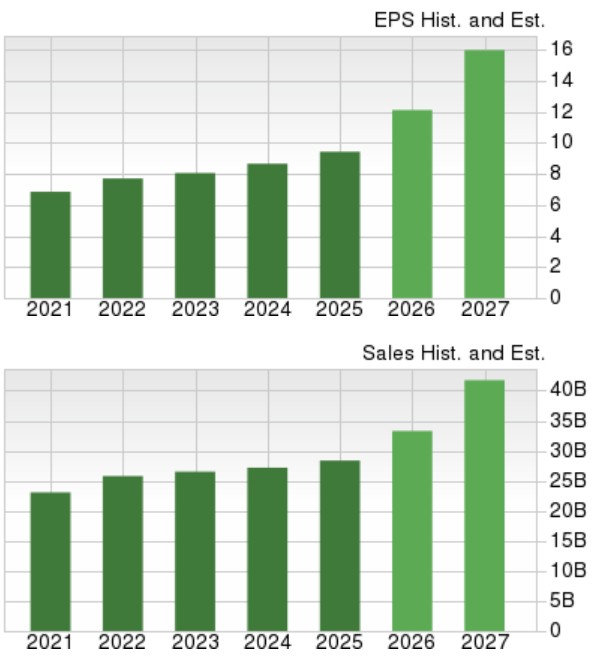

Tracking Applied Materials’ Outlook

Based on Zacks estimates, Applied Materials' annual sales are expected to increase 17% this year to a new peak of $33.29 billion, up from $28.37 billion in 2025. Furthermore, fiscal 2027 sales are projected to spike another 25% to $41.74 billion.

More impressively, Applied Materials' adjusted annual earnings are expected to jump 28% this year to a new peak of $12.11 per share, up from EPS of $9.42 on roughly $7 billion in adjusted net income last year. Better still, FY27 EPS is projected to climb another 32% to $15.98.

Image Source: Zacks Investment Research

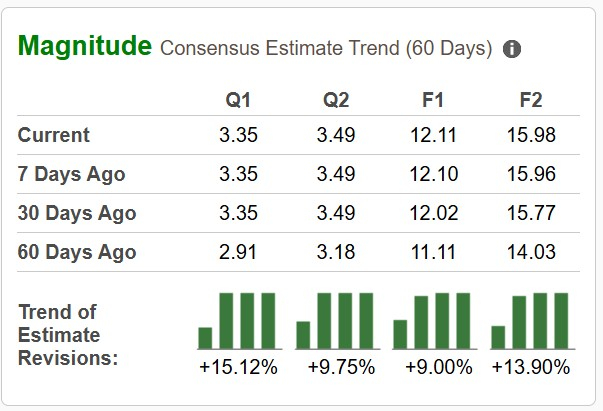

It’s also noteworthy that over the last 60 days, FY26 and FY27 EPS estimates have risen 9% (F1) and 14% (F2), respectively.

Image Source: Zacks Investment Research

Monitoring AMAT’s Valuation

Following its sharp rally, AMAT now trades at its highest P/E valuation in the last decade at 57X forward earnings. However, this is not an overly stretched premium to its Zacks Electronics-Semiconductors Industry average of 54X.

Like most AI-related semiconductor stocks, AMAT trades at a noticeable price-to-forward sales (P/S) premium as well, at 19X compared to its industry average of 8X.

Image Source: Zacks Investment Research

Is AMAT Still a Buy?

Applied Materials is benefiting from one of the strongest investment cycles the semiconductor industry has experienced in years. Rising AI infrastructure spending, improving industry fundamentals, analyst upgrades, and stronger semiconductor capital expenditure forecasts have all combined to push shares to record highs.

Although investors should expect some volatility after the recent rally, Applied Materials remains well-positioned to capitalize on the long-term AI semiconductor buildout. For investors seeking exposure to the semiconductor equipment space, the company continues to offer an attractive combination of market leadership, strong earnings momentum, and secular growth potential.

Keeping this in mind, Applied Materials stock currently sports a Zacks Rank #2 (Buy), based on the trend of positive earnings estimate revisions, which is helping to justify its elevated P/E valuation.

Comments

Log in or sign up to join the conversation.