Now, before you start calling me an Apple (AAPL) basher or a perma-bear, please know that this is far from the truth. Apple was one of my most significant portfolio holdings for over ten years (2006 - 2020). I realized early on that the iPhone would be a world-changing product and could transform Apple. Additionally, I continued to pound the table on Apple for years, as at 12 - 15 times forward earnings estimates, the company was substantially undervalued for a long time.

After about a 5,000% move (2006 - 2020), I exited Apple in Q4 2020 and found better investments since. To be clear, I am not arguing to short Apple. I think this is a poor investment idea right now. Nevertheless, due to minimal growth in coming years, Apple is likely a dead money investment for now.

Apple's Growth Story is Dead

I hate to say it, but Apple's "growth story" looks dead for now. My initial thesis for investing in the company centered around a revolutionary new product (iPhone) and its ability to continue to grow market share for many years into the future. Well, many years have passed, and the iPhone surpassed many of my expectations, but now what?

(Click on image to enlarge)

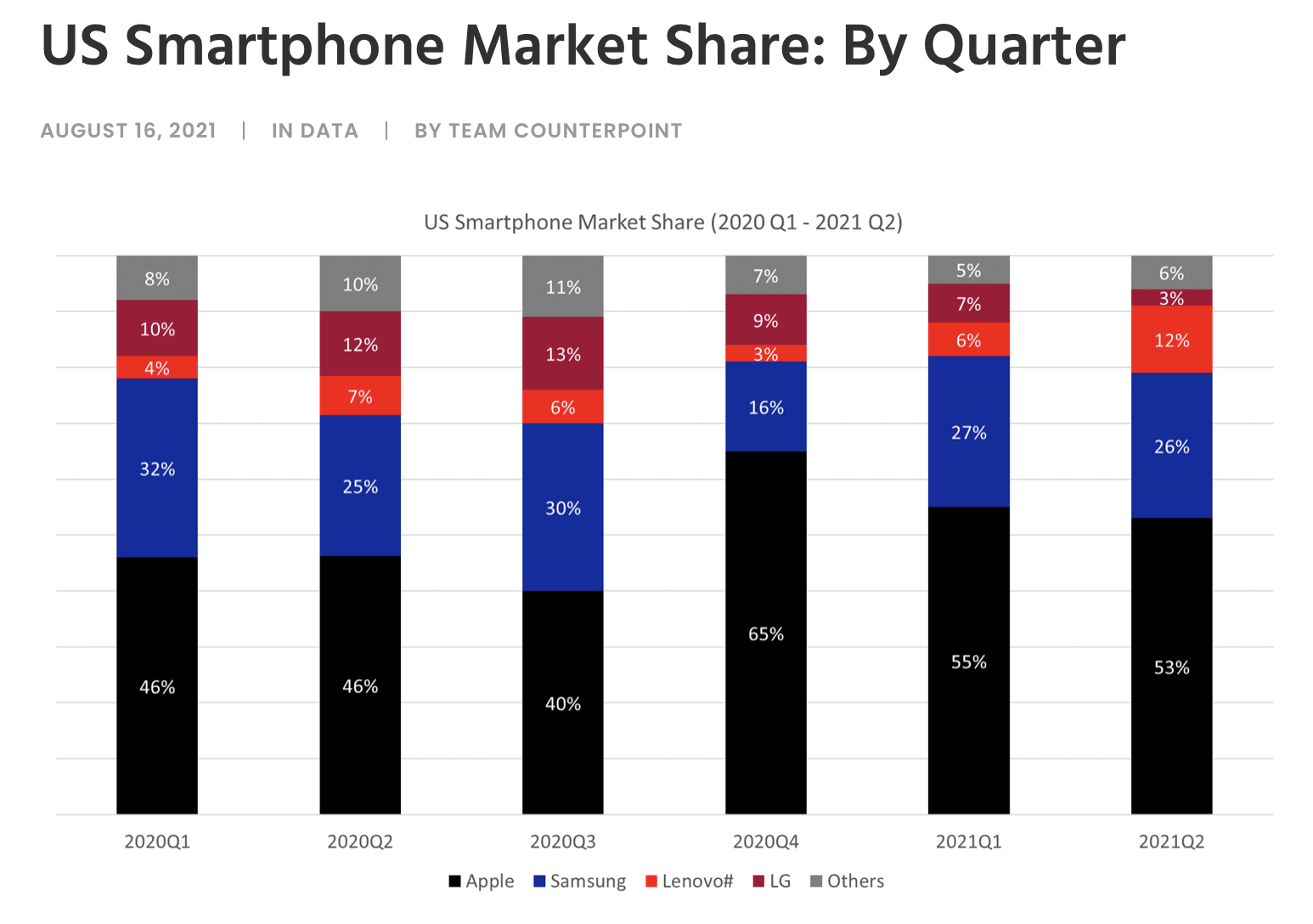

Source: counterpointresearch.com

The iPhone now accounts for more than 50% of the U.S.'s smartphone market. The iPhone already controls a massive share of the smartphone market in the U.S., illustrating Apple's high saturation rate, and I am not sure that Apple can continue to grow share from here. We see a notable gain in market share at the end of 2020, but the iPhone's market share has been falling since, with competitors Samsung (OTC: SSNLF) and Lenovo (OTCPK: LNVGY) making comebacks.

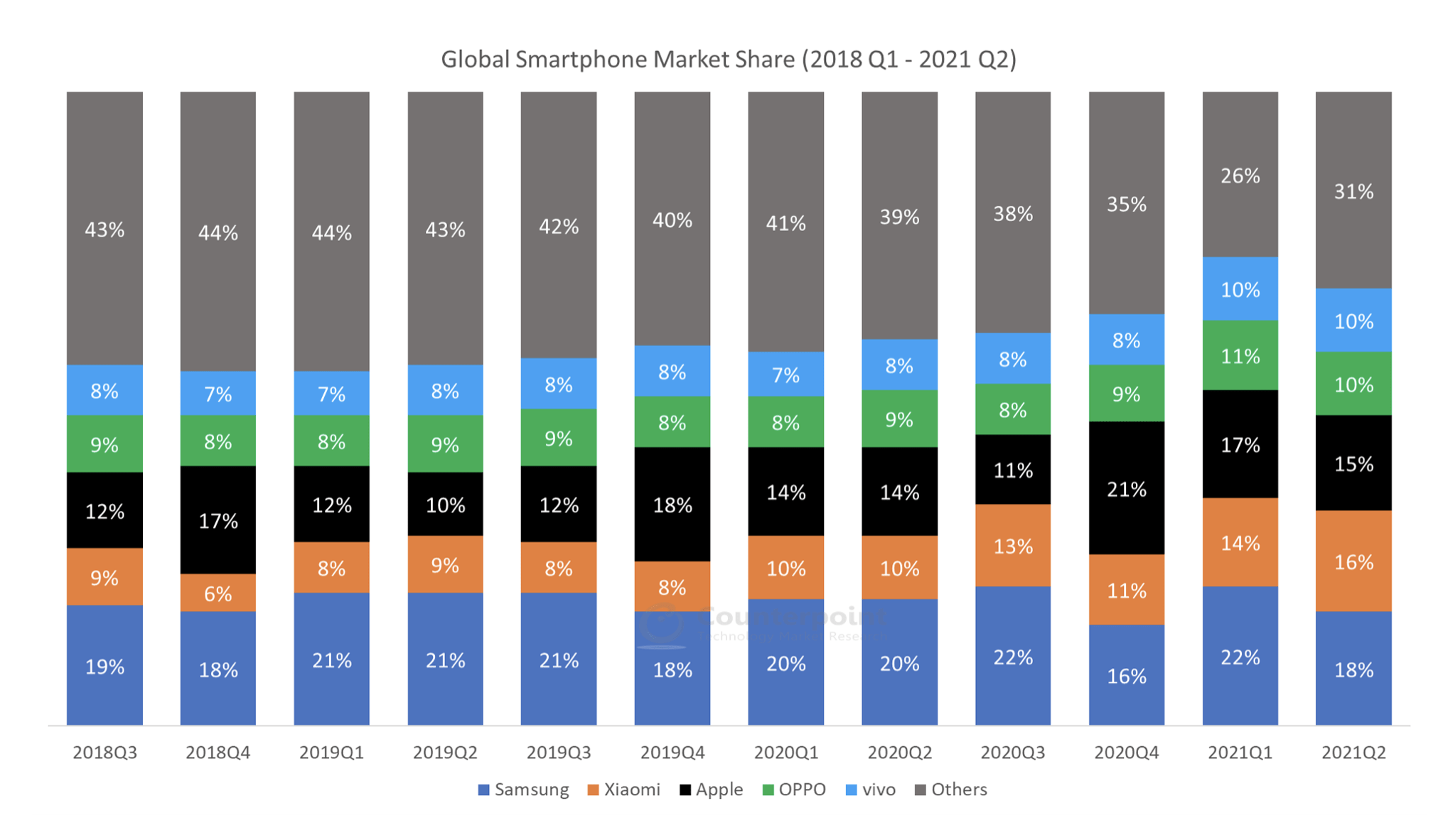

Global Smartphone Market Share

(Click on image to enlarge)

Source: counterpointresearch.com

If we look at the global market, again, we see Apple's share surge in Q4 2020, but its share has fallen since. Additionally, we see international competitors Xiaomi (OTCPK: XIACF) (OTCPK: XIACY) and others continuously gaining share. Apple is not likely to grow its market share substantially beyond its current global market share, as iPhones are considerably more expensive than its highly capable and much cheaper Chinese competitors. Thus we see Xiaomi and other prominent Chinese smartphone makers gaining share in the global market. While the iPhone's share has increased from 14 to 15 percent YoY, Xiaomi's has surged from 10 to 16 percent.

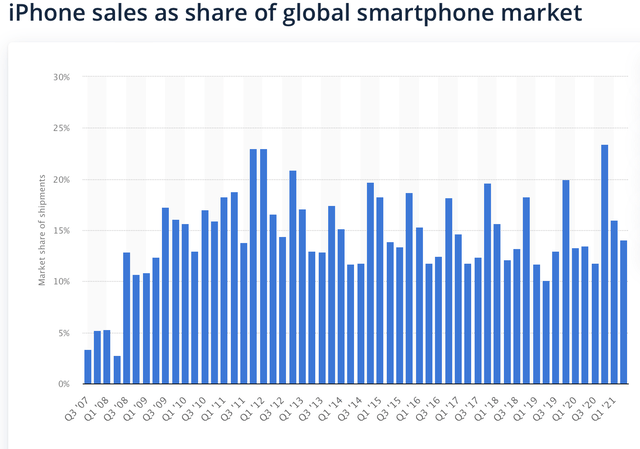

Source: statista.com

A long-term view of the iPhone's market share illustrates that we have seen a similar market percentage in recent years. Also, while growth surged late last year, it was likely due to pent-up demand due to the coronavirus along with the highly anticipated iPhone 12 release.

Furthermore, much of Apple's recent success has been due to the transition from the old iPhone 7/8 lineup to the new X/11/12 design. The substantial price increases also enabled the new iPhone lineup to produce substantially higher revenues and more profits for Apple. However, now that the "new" iPhone series is mature, it is not clear how Apple will continue to grow sales in its iPhone segment.

Missing Estimates: Red Flag for Apple

Firstly, Apple doesn't often miss revenue or EPS estimates, but it should be viewed as a red flag when the company does. Apple stopped reporting unit sales several years ago, but the company would likely show declining or slower than anticipated unit sales in some areas despite sales growth.

In Apple's most recent quarter, the company reported iPhone revenues of $38.87 billion, well shy of the $41.51 billion estimate figure. Mac and "other" segment revenues also missed estimates. The only segments to show slight beats in the quarter were iPad and services. Furthermore, while the company illustrated a substantial surge in YoY iPhone revenues, this phenomenon could have been due to the coronavirus-induced hangover effect coupled with new iPhone models coming to market. Overall revenues also came in lite, $83.36 billion vs. the $84.85 billion estimates.

Now, the company expects to set records next quarter, with an estimate of around $117.5 billion in revenues. However, even if the company delivers on its estimates, it will only be a 5.5% YoY increase. We are likely entering a period of shallow growth for Apple, and the stock's valuation is probably too high at this point.

Apple: Just Not Cheap Anymore

Apple used to be cheap. I used to write about this phenomenon all the time in 2017 and 2018. Apple seemed like an excellent investment with the stock trading around 12 - 15 EPS and a new iPhone lineup on deck. However, now that the company's valuation has ballooned to around 30 times EPS, Apple could be dead money.

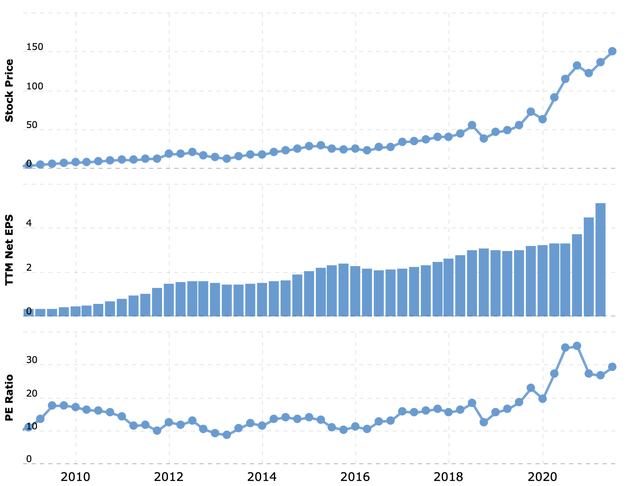

Apple's Valuation

Source: macrotrends.net

We see that Apple typically traded at a P/E ratio of around 12 - 15 before it surged into the 25 - 35 range in recent years. This increase is essentially the P/E ratio expansion I anticipated going into the new iPhone series product cycle. However, now that the current iPhone series has saturated the market, Apple's growth is minimal from here, and we could see multiple compression in future years.

We've seen times of stagnant or even declining growth at Apple before. Recently, Apple's revenues declined YoY in 2016, and 2017's revenues were lower than in 2015. Then we saw a relatively stagnant period between 2018 - 2020 revenue growth-wise. While Apple had a breakout growth year in fiscal 2021, this was partly due to the coronavirus's impact on sales in 2020, and there doesn't appear to be a catalyst for growth ahead.

Growth estimates are very modest for future years. Analysts expect revenues to rise to $378 billion in fiscal 2022, only a 3.6% YoY increase from this year. In addition, 2023 revenue growth is expected to be 5.5%, then 3.8% in 2024, followed by a 2% revenue decline in 2025. Therefore, we will likely see very little revenue growth from Apple over the next 3-5 years.

EPS growth trajectory looks very similar. We may see very slight YoY growth of only about 1% next year, followed by low single-digit EPS growth in coming years. Analysts anticipate EPS of just $6.56 in fiscal 2025, which is only a 17% increase from this year. Now, this is very muted growth, and a 17% EPS growth is something you would expect to see in one year from a company trading at a P/E ratio of around 27.

Instead, Apple is priced very richly here, almost the opposite of the valuation/growth dynamic we witnessed before the stock's runup in 2017 - 2018. Then, Apple was trading at a P/E multiple twice as cheap as today's and had much more growth potential ahead. Now Apple looks like an overvalued value company.

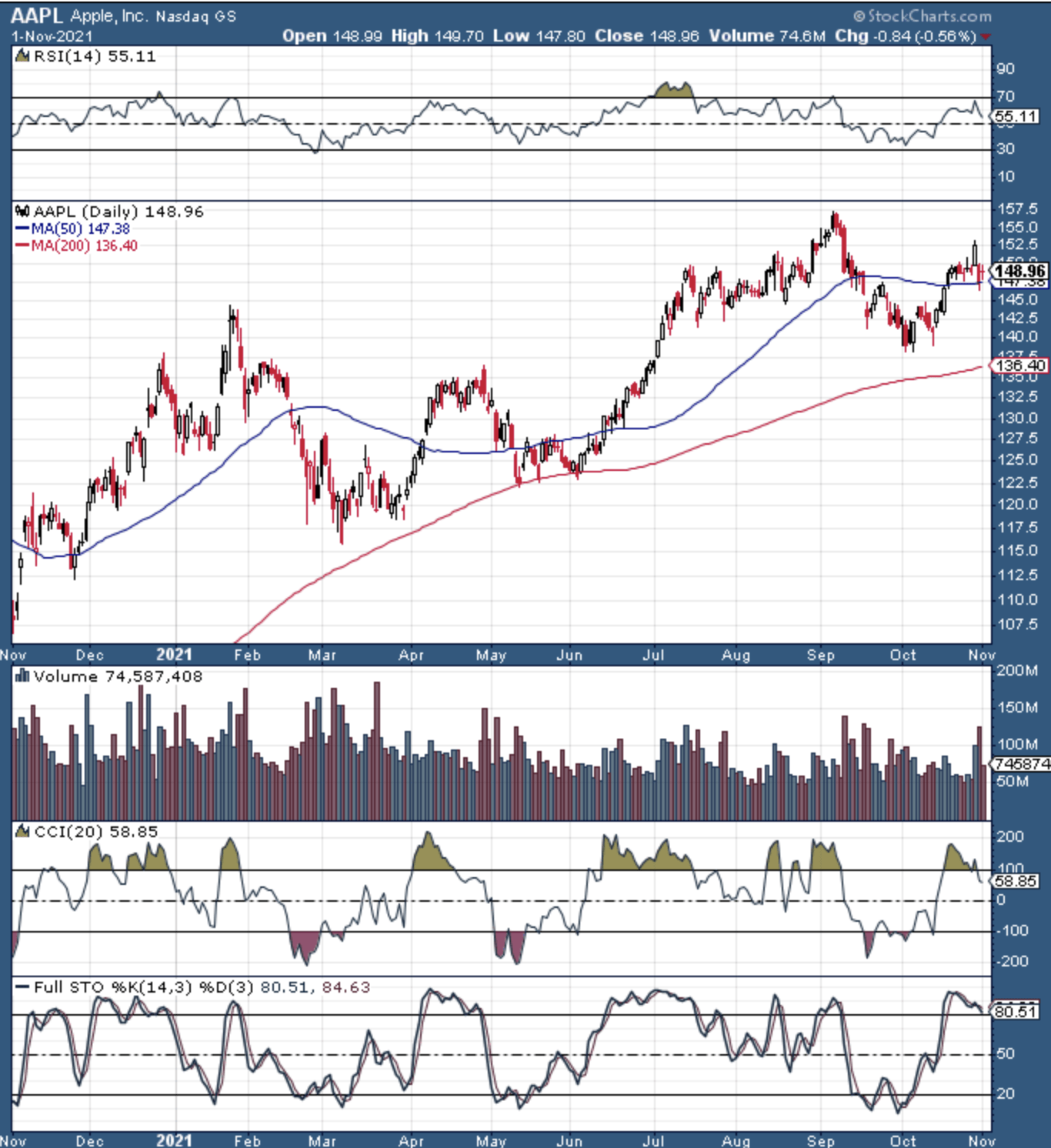

Blowoff Top Occurred

(Click on image to enlarge)

Source: stockcharts.com

Apple recently put in a blowoff top at around $158. The stock opened at a significant ATH, then closed notably lower on the session, and it's been mostly downhill ever since. When the stock hit this point, the company was trading at around 28 times forward EPS projections, extremely expensive for a company in Apple's low growth predicament.

We saw an attempt to move higher, but the stock made a lower high instead. The CCI and the full stochastic are turning down, and the stock is at risk of heading lower. Now, I don't think that Apple will experience a significant decline, but I also don't believe that the stock will be hitting new ATHs any time soon. Instead, the stock could trade sideways for a relatively long time and could be a dead money investment from here.

The Bottom Line: Upside for Apple is Limited From Here

Apple is transitioning to a slower growth environment. The company just went through a breakout growth surge year, during which revenues increased by 33%, and EPS climbed by 70%. Apple's stock also had an impressive run over the last year, appreciating by about 38%. Now, Apple's valuation sits at around 26.4 times forward earnings estimates. This P/E multiple is consistent for a company experiencing notable growth. However, the problem for Apple is that it's not about the past, but the future and Apple likely has very little growth in future years. Therefore, the coming low growth atmosphere should put pressure on Apple's P/E multiple. Thus, Apple's stock could be in trouble, may decline due to multiple compression, and is likely "dead money" for now.

Comments

Log in or sign up to join the conversation.