Alibaba (BABA) has been on a wild ride over the last year, but the more this stock drops, the more I buy.

Here's why:

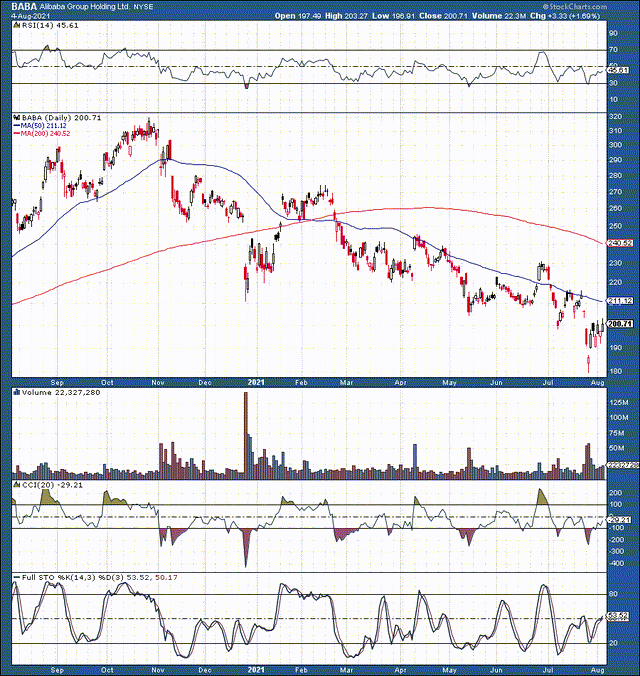

Source: StockCharts.com

Alibaba's stock peaked at about $320 around the end of October last year. It's been all downhill from there. From peak to trough, Alibaba's stock slipped by nearly 44%, wiping out more than $300 billion of the company's market cap in the process. However, Alibaba continues to grow and is becoming more profitable. The company is rewarding its shareholders by increasing its buyback program, and the stock is remarkably cheap compared to similar firms. Moreover, Alibaba's technical image suggests that the stock made a long-term bottom recently. Due to the improving technical setup, low valuation, and a constructive fundamental backdrop, there is a strong probability that Alibaba's stock will appreciate substantially over the next year.

Earnings Snapshot

- Alibaba recently put up a split quarter beating on EPS but slightly missing on revenues.

- EPS came in at $2.57 vs the estimate for $2.22 (16% beat).

- Revenues were light, $31.87 billion vs. the expected $32.4 billion figure (1.5% miss).

- However, revenue rose 34% on a YoY basis.

- The company reported an astounding 1.18 billion annual active customers, up 45 million QoQ.

- The company also announced that it is increasing its share buyback program by 50%, from $10 billion to $15 billion.

Revenue Breakdown

Source: alibabagroup.com

The company's core China commerce segment performed very well, accounting for 66% of total revenues and growing at 34% YoY. While international retail accounted for 5% of total revenues, this segment expanded by 54% YoY. The company's logistics service also illustrated substantial growth, increasing revenues by 50% YoY. Total commerce grew by 35% YoY, and the company's cloud unit increased revenues by 29%. While cloud revenue growth slowed down, we see that Alibaba's retail segments continued to fire on all cylinders, delivering robust revenue growth for the company in Q1.

Income Overview

Source: alibabagroup.com

We saw the cost of revenues increase significantly primarily due to sales and marketing expenses. This increase is not necessarily a bad thing as the rise may be transitory. If the company is spending more on advertising, Alibaba will likely grow its sales in the future. After all the variables are considered, Alibaba's net income decreased by roughly 8% YoY. Now, this may seem like a big deal, but I should point out that the company's revenues grew by 34% YoY. Additionally, some of the cost increases appear transitory. Furthermore, the company's stock price was about 30% higher a year ago, and Alibaba should become more profitable in future years.

Profitability Snapshot

Source: alibabagroup.com

Once we get down to the Non-GAAP figures, we see that Alibaba made about $7.1 billion for shareholders last quarter, a YoY increase of about 13%. So, we have income attributable to shareholders up by 13% while the share price is 30% lower, quite the disconnect here.

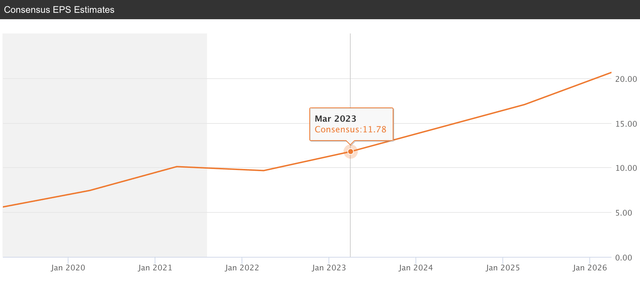

Valuation Perspective

Source: seekingalpha.com

Analysts expect Alibaba to earn close to $12 in its next fiscal year. This consensus estimate puts the company's forward valuation at around 16 times forward EPS projections. The company's trailing P/E ratio is approximately 19.8, and given the company's expected 27% EPS growth projection, Alibaba's PEG ratio is around 0.74 right now. These valuations are remarkably cheap for a company set to increase revenues and EPS substantially as the company advances.

Source: seekingalpha.com

Analysts anticipate that Alibaba will grow its revenues by 29% this year. Moreover, the company's growth runway is enormous, as revenues could essentially quadruple over the next decade.

Just how cheap is the stock?

So, I mentioned its 16x forward P/E ratio, 0.74 PEG ratio, expected 29% revenue growth rate, and 27% EPS growth projection. Now let's look at Alibaba's closest competitor, its counterpart in West Amazon (AMZN).

Amazon's business is quite similar to Alibaba's in many aspects. Both companies are massive e-commerce juggernauts, both have powerful cloud platforms, and both names have a diversified secondary business portfolio.

However, Amazon trades at 50x forward EPS, has an estimated EPS growth rate of about 26%, a projected revenue growth rate of 18%, and a PEG ratio of around 2. If these were identical companies, we can see that Alibaba should be awarded the higher multiple because of its superior revenue growth rate, but that is not the case. Instead, we see that Amazon trades at triple Alibaba's multiple both on the forward P/E and on the PEG side of the equation.

So, why does Amazon deserve such a rich multiple relative to its Eastern counterpart? Yes, I understand the China risk is there, but it seems overdone now. It doesn't seem very likely that the Chinese Communist Party "CCP" would reck one of its most prominent tech companies. Besides, Alibaba already paid its fine, and it may be time to move on.

The way I see it - one of these companies is very expensive, or the other one is very cheap. Since I own shares of Amazon, I'm inclined to say that Alibaba is exceptionally cheap right now. If its stock were trading at a comparable multiple to Amazon, Alibaba's shares would be worth around $600 right now.

The Bottom Line

Alibaba is trading at around $200, but its actual value seems highly suppressed right now. Yes, the China risk is present, but I don't think it's worth $400 or roughly $1 trillion in lost market cap (comparison Amazon's valuation). Due to the various adverse news events surrounding the company and China's market in general, Alibaba's stock started heading in reverse toward the end of last year and has been stuck in the wrong direction ever since. However, nothing fundamentally has changed at Alibaba. The company is the rapidly expanding dominant e-commerce giant in the east, is remarkably cheap, and should continue to increase EPS in the future. The stock looks like it has bottomed, the fundamental image is strong, and shares should start going in the right direction from here.

Comments

Log in or sign up to join the conversation.