Alibaba (NYSE: BABA) stock has produced lackluster returns over the past year, shares of the Chinese online giant are down by 12% in the past 12 months due to the trade war concerns and economic uncertainty in China. On the other hand, the company's fundamentals look stronger than ever, and the stock is very attractively priced at current prices.

As Warren Buffett said, the time to be greedy is when others are fearful, and geopolitical fears are creating a buying opportunity in Alibaba stock.

The Fundamentals Remain Intact

In spite of the economic volatility in recent months, Alibaba keeps firing on all cylinders as of the most recent earnings report. Even a mediocre company can do well when the wind is on its back, but it takes a particularly resilient business to continue growing at full speed in spite of economic and geopolitical headwinds.

Some key metrics to consider:

- Revenue reached RMB93,498 million (US$13,932 million), an increase of 51% year over year.

- Annual active consumers on the company's China retail marketplaces reached 654 million, an increase of 18 million.

- Mobile MAUs reached 721 million, an increase of 22 million.

- Adjusted EBITDA increased 29% year over year to RMB25,166 million (US$3,750 million).

- Non-GAAP diluted EPS was RMB8.57 (US$1.28) during the quarter, an increase of 50% year over year.

Very few companies in the world can sustain those levels of growth from such a massive size, especially in times of economic uncertainty. This speaks well about Alibaba's fundamental strengths and the company's ability to continue executing in all kinds of environments.

Interestingly, management highlighted during the conference call that Alibaba could actually benefit from the trade war going forward. If China is going to import more products from the US and other countries, Alibaba is in a position of strength to become the platform of choice for global producers and brands selling into China due to the company's massive reach of over 650 million active Chinese consumers on its platform.

Looking at the long-term opportunity, the middle class in China has reached a critical mass of over 300 million, almost as large as the entire U.S. population. The size of the middle class is expected to double in the next 10 years, especially from the lesser developed Chinese cities.

Chinese domestic consumption is $5.5 trillion today, and consumption from these cities, with a combined population of 500 million people, will triple from $2.3 trillion to nearly $7 trillion in the next 10 years. This gargantuan opportunity should allow Alibaba to continue delivering attractive returns in the years ahead.

Attractively Valued

Wall Street analysts are on average expecting Alibaba to make $6.73 in earnings per share during the current year and $8.76 next year. Under those assumptions, the stock is trading at forward PE ratios of 25 and 19, respectively. The valuation looks more than reasonable for a company that is currently growing at more than 50%.

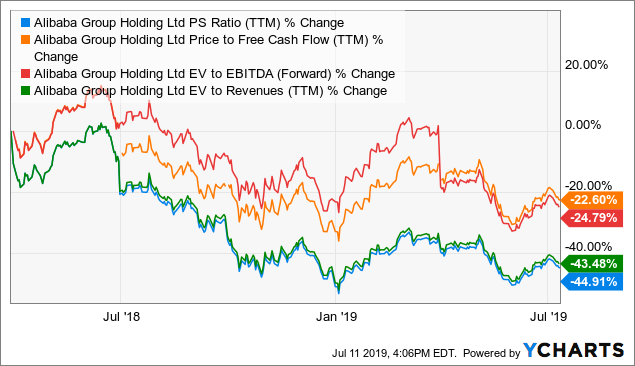

The chart shows how different valuation ratios such as price to sales, price to free cash flow, EV to EBITDA and EV to Revenues have evolved over the past 3 years. Alibaba stock is currently trading at a valuation discount of between 22% and 45% versus its recent history.

(Click on image to enlarge)

Data by YCharts

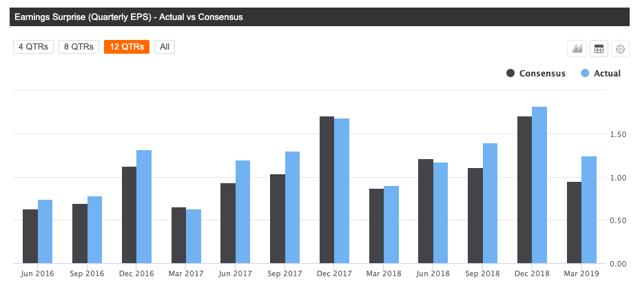

It is important to keep in mind that Alibaba tends to deliver earnings figures above Wall Street expectations more often than not. The chart below compares the expected earnings number with the actual reported figures, and Alibaba has delivered above expectations in 9 of the past 12 quarters.

(Click on image to enlarge)

Source: Seeking Alpha Essential

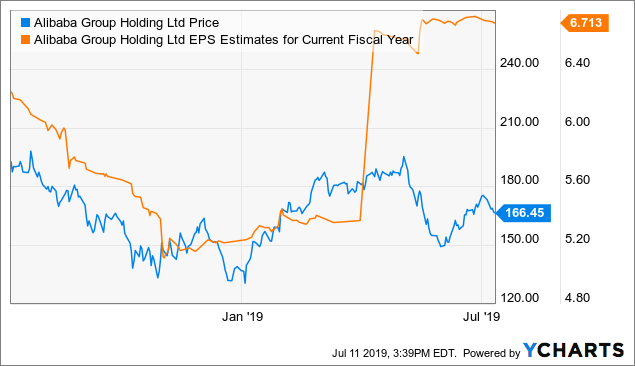

Since the company delivered solid numbers last quarter, Wall Street analysts have increased their earnings expectations for Alibaba in the current year.

The stock price and earnings estimates generally move in the same direction over time, but there is a gap in terms of earnings estimates and the stock price in the case of Alibaba recently. The stock price is lagging earnings expectations, and this is arguably reflecting an opportunity in Alibaba stock.

(Click on image to enlarge)

Data by YCharts

It's hard to tell how the trade war negotiations will evolve in the short term, however, Alibaba is not only producing strong growth but also delivering solid fundamental momentum, meaning that the business is doing better than expected. Over the long term, this should drive the stock price higher, with or without geopolitical risk.

Valuation needs to be analyzed in its due context. A company with strong financial performance and accelerating momentum obviously deserves a higher valuation than a business producing mediocre financial performance and languishing momentum.

Alibaba is in the top 10% of companies in the US stock market based on financial quality, valuation, fundamental momentum, and relative strength combined. In other words, Alibaba looks particularly cheap when the valuation ratios are analyzed in the context of other quantitative drivers.

Moving Forward

The trade war should not have much of a direct impact on Alibaba's business model, but the indirect impact from economic uncertainty in China could be more relevant. The company also makes most of its money in RMB, so a depreciating Chinese currency would reduce the value of those earnings when translated to US dollars.

Regulatory risk is always an important consideration when investing in China since accounting rules in the country are not as strict as in the US and the government can have a big impact on different industries through all kinds of interventions. Alibaba has made lots of acquisitions in recent years, which makes the company's financial statements more complicated and financial performance harder to predict.

Nevertheless, those risk factors are more than accounted for in the current valuation. Alibaba continues growing at full speed, and chances are that investors who buy the stock at current prices will be rewarded with attractive returns over the long term.

Comments

Log in or sign up to join the conversation.