NOV SOYBEANS

With the USDA Oct 12 Demand & Supply coming out Wed & harvest weather very benign, the size of the Bean Crop continues to be ratcheted up fromthe 4.2 BB crop estimate from the govt in Sept to the recent Informa # – 4.300 BB to the FC Stone # 4.357 BB.Remarkably, since Aug 1 – despite all the “record crop talk”, the (940-1020) rang has held Nov Futures – as robust exports have continued to offset better-than-expected yields.

FACTORS IMPACTING THE MARKET

EXPORTS – Tues Inspections were 1.801 MMT (LW -1.109)

Thur sales were 2.18 MMT (1.3 – 1.7)

Thur – 258,000 MT to Unk

Fri – 195,000 MT to Unk

CROP CONDITIONS – harvest 44% (LW – 26, AVG – 47)

Ill – 39 % (46) Ind – 33 % (36) Ia –43 %(54)

USDA 10/12 SUPPLY & DEMANDEST

Bean Production –4.286 BB

Yield –51.5

US Stocks 0.413 MB

Global 73.28 MMT

BETTER-THAN-EXP-YIELDS – continue to support ideas that the Bean crop will continue to grow in the USDA Oct & Nov Crop Reports.

CRUDE OIL – has rallied $8.00 since Mid-Sept on ideas OPEC Will at long last – cut production – and this is certainly beneficial To ethanol demand & therefore to the corn market

US DOLLAR – despite a tepid Oct unemployment report, the Dec $ Contract is stubbornly holding onto a 200 point rally that started In Mid-Sept. A rate increase by years end would support this market.

The bottom end of its two month range holding – despite continued reports of better-than-expected yields – bodes well for the market. Exports will certainly outlast harvest pressure.

DEC CORN

Much like Nov Beans, Dec Corn has been range bound since early August – confined to a tight range (315-340).But unlike Nov Beans, Dec corn was able to momentarily break out of that range early last week – on the heels of a neutral Sept 30 Qtly Stocks Report. The report spawned a 20 cent rally (330-350).Unfortunately, heavy harvest pressure brought the market back to the top end of its range.

FACTORS IMPACTING THE MARKET

EXPORTS – Tues Inspections were 1.131 MMT (LW-1.485)

Thur sales were a whopping 2.50 MMT (900-1.9)

Tues – 100,000 MT to Unk

CROP RATINGS – Harv – 35% (38)

Ill – 62% (51) Ind – 38% (33) Ia – 19% (32)

SEPT 30 QTLY STOCKS – reflected 738 BB (exp – 1.754) – The market had a strong reaction up – as it was looking for a Much bigger #

Oct 12 USDA REPORT –

Production– 15.060 BB

Yield 173.5 B/A

US Stocks 2.359 MB

Global – 218 MMT

UNEVEN YIELDS – unlike bean yields which are being universally reported as better than expected, corn yields are much more Variable & the market action reflects that.

HISTORIC SUPPORT – as Dec Corn continues to hold its (315-340) range, it is also holds lows established in 2007 & 2008.

The markets inability to break thru the bottom end of its range (315-340) off a widely reported record crop at 15 BB plus – in the middle of harvest speaks volumes. The harvest lows appear to be in & exports will determine the extent of the rally from these lows.

DEC WHEAT

Since Sept 1, Dec Wheat has been locked in a very tight range (390-410) as its own massive stocks & record Corn & Bean Crops now in harvest have continued to weigh on the market.The only thing keeping it honest – is its price level at a 10 year low & a big short open-interest in the market– that promises to exit– should anything ignite a rally.

FACTORS IMPACTING THE MARKET

The USDA pegged the Sept 1st stocks report at 2.527 BB – Up 21% from last yeat & the largest since 1987-88

The US Dollar, emboldened by the likelihood the Fed will raise rates byear’s end, has rallied – weakening export prospects for Wheat

Egypt recently bought 24,000 MT of Russian Wheat at 187.20 – it didn’t Go to the US but still was a positive – as Wheat was moving on the world stage

Morocco bought 260,000 MT of US Wheat – which drove the Dec Wheat to the top end of its range

The rally was short-lived as the market needed but didn’t receive Further export news after Morocco

Trend-following funds hold a record net short – 164,690 contracts

The market is eagerly awaiting the Wed USDA Supply & Demand Report

At 11am – negative #’s are expected but are they dialed in?

DEC CATTLE

The first 6 trading days of October have witnessed some extreme volatility – as Dec Cat has both rallied $5.00 (99-104) & broken $5.00 (104—99) – asit trys to come to grips with record supplies of meat & a price level low enough to absorb them.

- The heavy supplies have created a $3.50 discount to cash when A $7.50 premium is the norm

- The market is burdened – not only with huge meat supplies but Hefty pork & poultry stocks as well

- A lesser 4th Qtr production of beef is expected to take some Pressure off the market

- A blending of technical & fundamental factors is needed to confirm A low

- A tapering off of weekly slaughter might allow beef prices to settle

- Yesterday’s limit down tells us the lows are still being probed

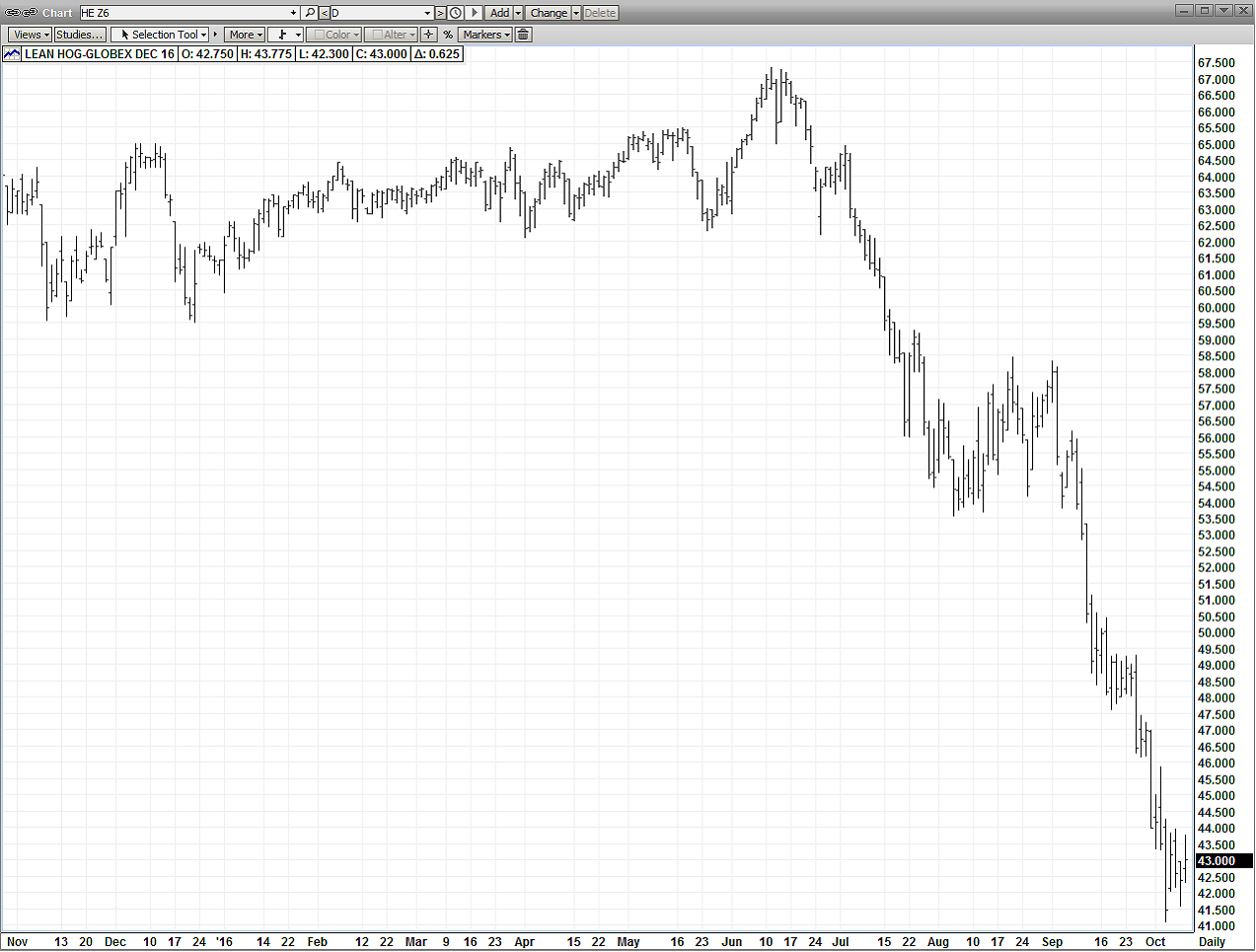

DEC HOGS

On Fri 9/30/16 at 2pm, the USDA issued their Quarterly Pig Crop Report- which reflected a record supply at 102.4% over last year. Prior to the report, Dec Hogs went limit down – in anticipation of a negative #. The entire sequence of market action suggests this report may have put in a low in.

- We need to see daily slaughters amounts level off

- We need to see weekly exports kick up

Comments

Log in or sign up to join the conversation.