"Worldly wisdom teaches that it is better for the reputation to fail conventionally than to succeed unconventionally" John Maynard Keynes

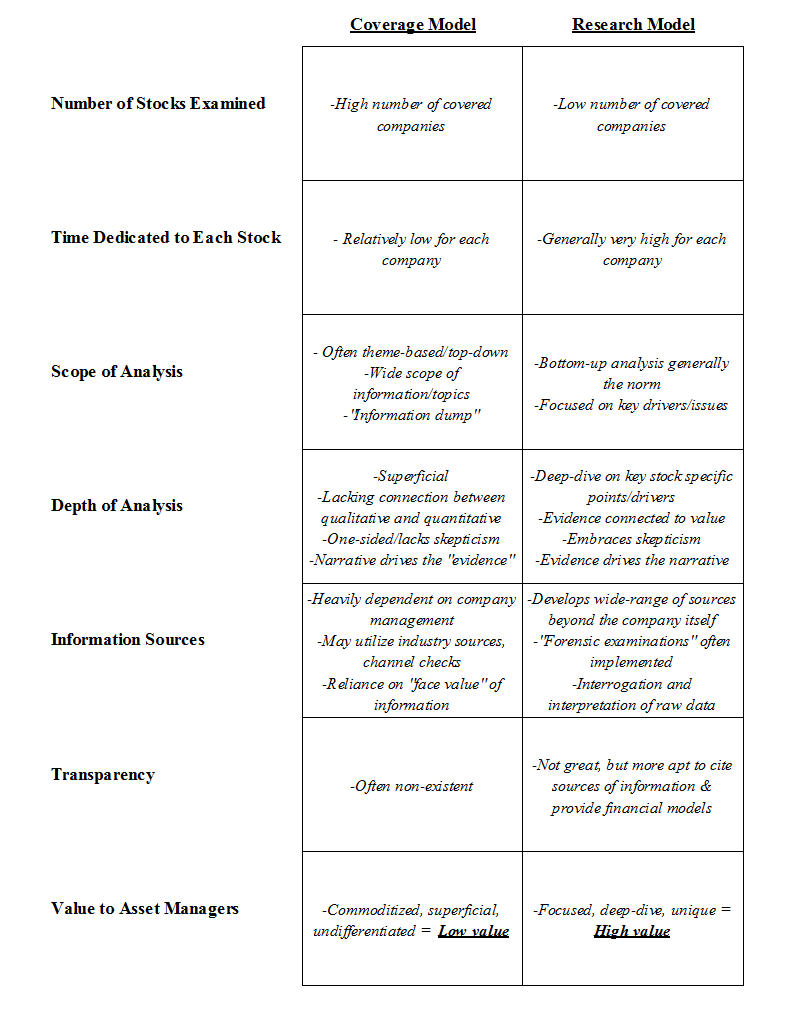

The chart below demonstrates a trend that is well-discussed in asset management circles. Active managers continue to struggle with outflows, a shift that began with the devastating withdrawals of 2008. Meanwhile passive indexing funds are roaring ahead, led by the likes of Vanguard and Blackrock’s iShares. 2014 was the best year ever for passive funds, with net inflows of nearly $100bn. In the same year active funds saw net outflows of $74bn.

Source: ICI Investment Company Factbook, StockViews Research

The future certainly looks bleak for active managers. However there is a silver lining for those that are prepared to change.

Failing Conventionally

The "bulge bracket" model of active management is rapidly loosing its appeal. Increased transparency and a robust debate around historical performance has taught the mass-market the same thing that professionals have always known: Active management offers a raw deal to consumers. Most active managers churn out a result which is more-or-less similar to the market. After fees of 2% or more, the vast majority of these strategies are consigned to chronic underperformance. Increasingly consumers are asking themselves, what am I paying for?

Active funds have responded by reducing fees, but they are coming from such a high starting point that it’s having little impact on behavior. Smart consumers are looking at what they’re getting for their money and making a choice – either they want to achieve meaningful outperformance or they will simply invest in the index. This is one of the key trends identified by PwC in their recent report "Asset Management 2020":

"Many investors have now come to realize that a large proportion of alpha strategies are arguably closet beta – that is, an expensive and disguised beta product. It is not surprising that many long-only active funds have seen quarter after quarter of net outflows. The growth of AUM and profitability of many strategies based purely on absolute return, particularly in the equity space, will likely be under severe pressure in the indefinite future"

This is putting pressure on asset managers to move away from "closet beta" and demonstrate outperformance. Most of them, however, are struggling to re-engineer their operations for this new world. Having been a fund manager for over 10 years, I know that these institutions are not environments that are conducive to alpha generation. The philosophy of most professionals is that it’s better to fail conventionally than succeed unconventionally. Institutional bureaucracy, excessive diversification, and a fixation with career risk work together to encourage benchmark hugging. On top of this funds find it hard to invest in smaller-cap stocks, where many of the best opportunities are to be found. Most asset managers are happy to sit back and "go with the flow". In 1995 this was fine and fund managers could enjoy a nice long career without any downside. In 2015, it’s not OK. (I have written more about the constraints of an institutional environment here)

Fragmentation of an Industry

Despite all these issues, we shouldn’t write off active management just yet. You might be surprised to learn that the number of actively managed funds has actually been rising over the past 2 years. Last year saw the net creation of 96 new active funds in the US, the most since 2006. (Meanwhile the number of passive funds hasn’t changed much at all in the past 10 years.)

Source: ICI Investment Company Factbook , StockViews Research

These figures confirm a trend that many professionals already understand – active fund mangement is fragmenting. While mega-managers like Fidelity experience huge outflows, smaller and more nimble firms are taking share. These smaller firms lack the constraints of a large institution and are driven by a strong performance-oriented culture. The continued growth of the hedge fund industry and the proliferation of small family offices also speaks to this trend. (In contrast a large institution is actually quite well adapted to manage index money, where processes can be automated and costs kept to a minimum. In this context the lack of growth in passive funds makes a lot of sense.)

Succeeding Unconventionally

Smaller firms are more likely to live or die by the value they provide to customers. They are usually guided by a strong investment philosophy, they have the flexibility to act fast and they can get involved in situations that larger firms wouldn’t (or couldn’t). They are often led by people who are fully invested alongside their clients. This kind of alpha generation is often worth paying for.

"In wealth management in particular, firms will win or lose based on their ability to clearly define in the client’s mind a "unique value proposition" that differentiates their brand identity from that of other players in a very crowded market" Asset Management 2020

Many asset managers try to differentiate themselves by launching expensive ad campaigns, drawing attention to their "unique offering". But most consumers are adept at smelling the BS. Underlying the marketing message we know we’re backing the same old dinosaurs; dinosaurs who are more comfortable keeping their job than generating value.

"By 2020, the industry is likely to see the emergence of a new breed of global managers, one with highly streamlined platforms, targeted solutions for the customer, and a stronger and more trusted brand. These managers will not only emerge from the traditional fund complexes, but from among the ranks of large alternative firms as well" Asset Management 2020

Change before you have to

I believe there is a future for active fund management but it requires managers to make a break from the old world. The same level of disruption occurs in all industries that are subject to a high level of competition and transparency. Industries like retail and tech have to constantly reinvent themselves every few years to remain competitive. There’s no reason why the investment industry should be any different.

Jack Welch said "Change before you have to". Firms that want to charge for alpha-generation must have a process and culture that can genuinely deliver it. Those who don’t will be consigned to the shrinking ranks of the benchmark dinosaurs.

"For active investment strategies, managers must educate, explain and prove alpha more than ever to increasingly skeptical clients" Asset Management 2020

Comments

Log in or sign up to join the conversation.