Market Analysis

After last month’s initial US and World new-crop supply/demand updates for the major row crops, the upcoming June 12 monthly balance sheet changes have been modest in the past. Adding to DCs stay the course approach are the USDA June 30 US acreage and third-quarter grain stocks reports. These two reports are highly important to the size of 2018 crops and helps determine the past quarter’s domestic demand across the US major crops.

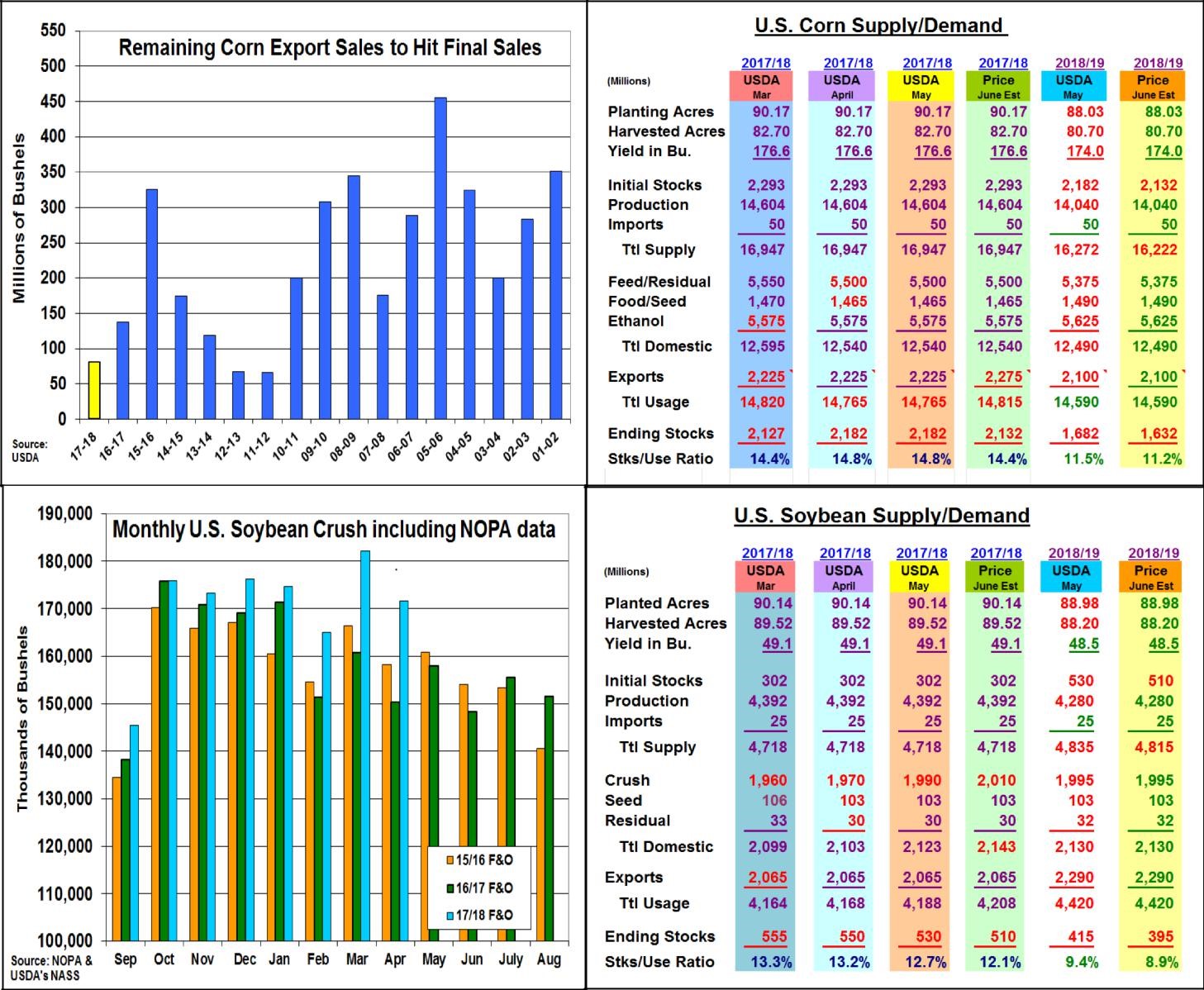

Using these tendencies, corn’s old-crop US balance sheet will likely have only a slight change. With US export sales only 81 million bu. below the USDA’s outlook, this demand level could rise by 50-75 million bu. this month. This year’s Argentine drought and S American analysts projecting a 5-7 mmt further drop in Brazil’s Safrinha corn output suggests the USDA will up this foreign demand. Domestically, ethanol output currently is on target to utilize the USDA’s 2017-18 forecast and corn’s feed demand can’t be calculated until the quarterly stocks report is available on June 30. With no changes in 2018/19’s acreage or demand levels until June 30, any old-crop stock changes will pass through to 2018/19’s ending stocks.

In soybeans, this year’s US crush has been very strong. Thru the first 8 months, this demand’s pace has already covered 77 million of the USDA’s 80 million bu. higher outlook. This suggests a 20-25 million higher forecast is forthcoming. Exports are only 27 million below the USDA outlook, but given the current US & China trade tensions, this demand level may remain unchanged.

In wheat, this week’s final inspection level suggests old-crop exports may have fallen 15 million bu. below the last forecast. With just 5% of the US winter wheat harvest done, limited crop changes are expected. Slightly higher early S. Plains yields suggest a 7 million rise in hard red output to 654 million while above-normal PNW conditions & a mixed Midwest May keeps our total WW crop at 1.199 billion bu.

(Click on image to enlarge)

What’s Ahead

The upcoming June crop report and supply/demand adjustments hold some modest trade interest. However, the beginning weather trend for 2018 crop year in the central US and news from the ongoing US/China trade talk will likely have more impact on the world’s grain and oilseed markets. Let’s hope the two sides get to the table soon for more talks. Hold sales.

Comments

Log in or sign up to join the conversation.